@TBPInvictus here:

I’m not an economist, but I count several very good ones among my friends. (Exciting, right? Note to self: get a life.)

On occasion, especially when my pal David Rosenberg is in town from Toronto, I’ll convene a dinner with eight or ten participants ranging from economists to academics to strategists to technicians to media types to hedgies to C-suiters to the occasional billionaire. And Barry. And Rich Yamarone.

At just such a dinner one year ago (see down below, as told by a participant), a question was posed to the table: Would the Fed raise rates in 2015? Count me among those who has thought all along (read: from 2009 on) that the Fed would be – and will continue to be – lower for longer. I have not thought until now that raising the Fed funds rate would be the appropriate course of action, and I don’t think so now. I’m with Summers and Krugman that the risks are asymmetric and that they should wait until they see the whites of inflation’s eyes. That said, I think it’s entirely possible that the FOMC will not have the courage of (what I think is) its conviction in the face of markets that clearly want and expect liftoff. However, I’m going to stick to my guns, fingers crossed, and forecast that Yellen & Co. are ready, willing, and able to stand up to petulant markets and hold steady.

As Paul Krugman wrote in his column on December 7, after the jobs number on the 4th:

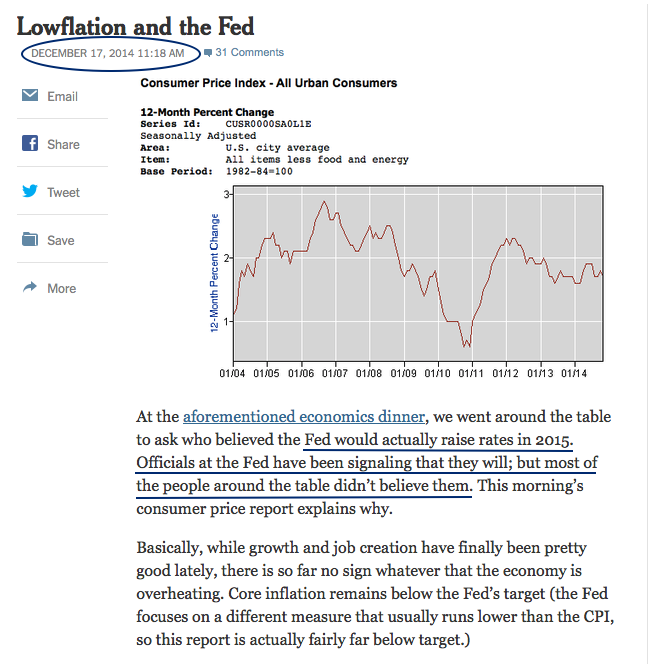

Fed officials believe that the solid job growth of the past couple of years — which happened, by the way, as Obamacare, which conservatives assured us would be a job killer, went into full effect — will continue even if rates go up. I’m among those who believe that America is facing growing drag from the weakness of other economies, especially because a rising dollar is making U.S. manufacturing less competitive. But those officials could be right, in which case waiting to raise rates could mean some acceleration of inflation.

On the other hand, they could be wrong, in which case a rate hike could end the run of good economic news. And this would be much more serious than a modest uptick in inflation, because it’s not at all clear what the Fed could do to fix its mistake.

I’m not sure why this argument, which a number of economists are making, isn’t getting much traction at the Fed. I suspect, however, that officials have been worn down by incessant criticism of their policies, and want to throw the critics a bone.

But those critics have been wrong every step of the way. Why start taking them seriously now?

With that, BR’s take:

~~~

@Ritholtz here: I’m not an economist (but I play one on TV). At the aforementioned dinner, I was the sole person expecting rates to go higher.

My reasons for the Fed to go in 2015 were simple:

• The Fed gave us targets, all of which had been hit (or in the case of CPI, was about to be hit);

• The emergency circumstances which precipitated ZIRP & QE was gone;

• It gave the Fed an opportunity to declare victory and go home.

Everyone else seemed to be either overthinking it. Occam’s Razor said keep it simple; the contrarian position was in my opinion, the best posture as well.

Sometimes, Fed officials say what they mean. That seems to be the case here.

The third possibility is that the Fed critics will get their bone but the Fed will not raise again.

That would be my guess too. Give them the expected 25bp (the economy has already taken the hit from that), then disappoint the market expectations on when they add the next 25bp. That would recover some of the damage already done.