How the ECB should respond to a German fiscal boost

Christian Odendahl

Insight, 26 September 2017

A German stimulus has the potential to help the eurozone economy. But how the ECB reacts is key.

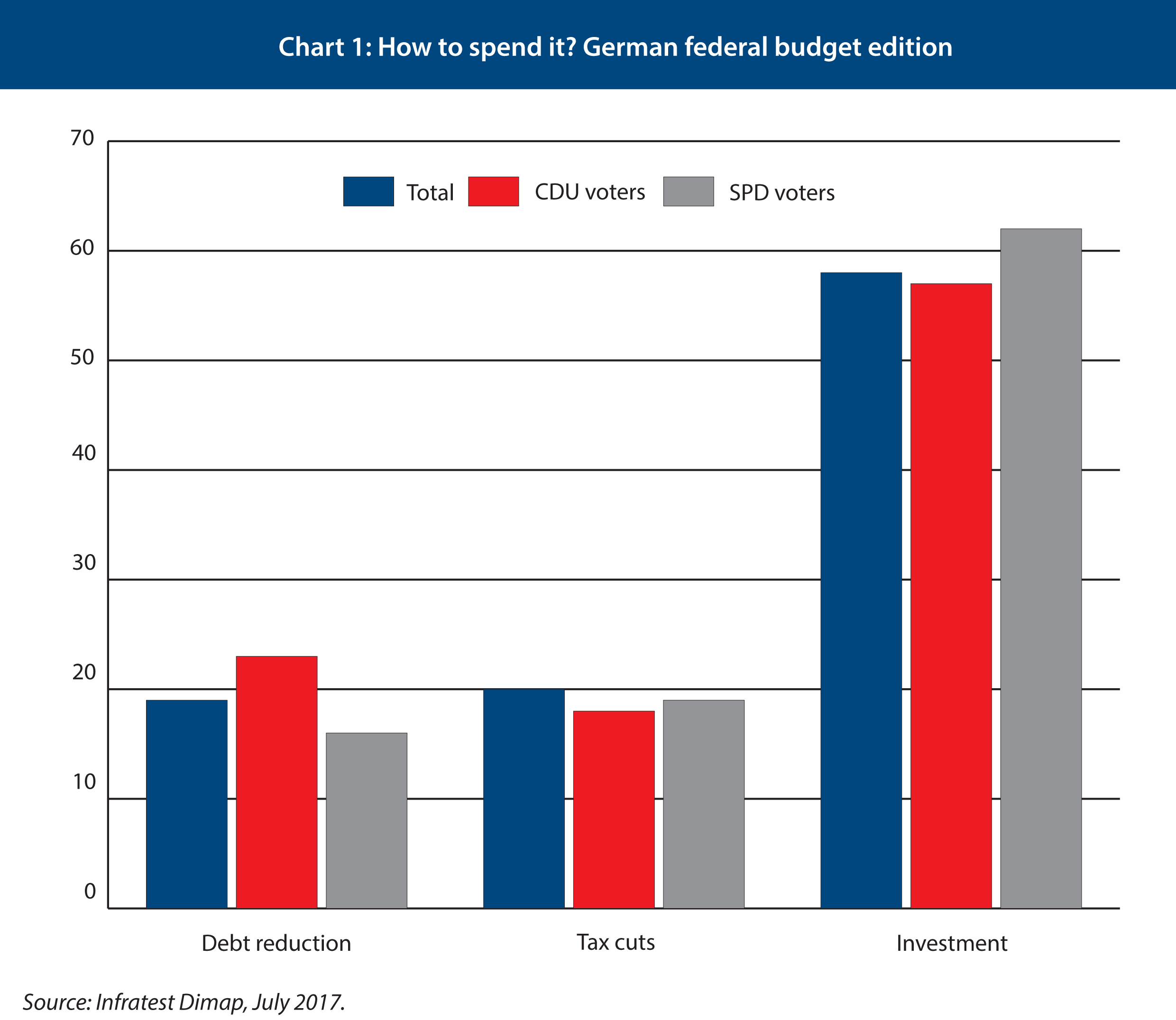

There will be difficult coalition talks ahead for Angela Merkel and her party, after Sunday’s election. A ‘Jamaica’ coalition of the conservative CDU/CSU, the Greens, and the pro-business Free Democrats (FDP), named after the parties’ colours, emerged quickly as the most likely. And that government will be under pressure to invest more. A large majority of German voters, even right-leaning voters, favour higher public investment over tax cuts and debt repayments (see Chart 1). Also outside Germany, many would like Germany to spend and invest more to boost Europe’s economy. But to what extent would a German fiscal expansion help the rest of the eurozone, now that it is recovering?

Start with how big a German fiscal expansion will be. Berlin’s fiscal policy is constrained by a constitutional ‘debt brake’, which restricts the federal public deficit to less than 0.35 per cent of GDP and those of the Länder (the German states) to zero. Both thresholds are applied after accounting for the ups and downs of the business cycle. As a result, the debt brake is supposed to mandate neutral fiscal policy throughout the cycle: deficits in recessions, surpluses when growth is strong. But even with the debt brake mechanism in place, German fiscal policy is gradually becoming more expansionary. Start with how big a German fiscal expansion will be. Berlin’s fiscal policy is constrained by a constitutional ‘debt brake’, which restricts the federal public deficit to less than 0.35 per cent.

First, in order to apply the debt brake, policymakers need to know at what stage the economy is in the business cycle, and how that affects government revenue and spending. This calculation is prone to error and later revisions.

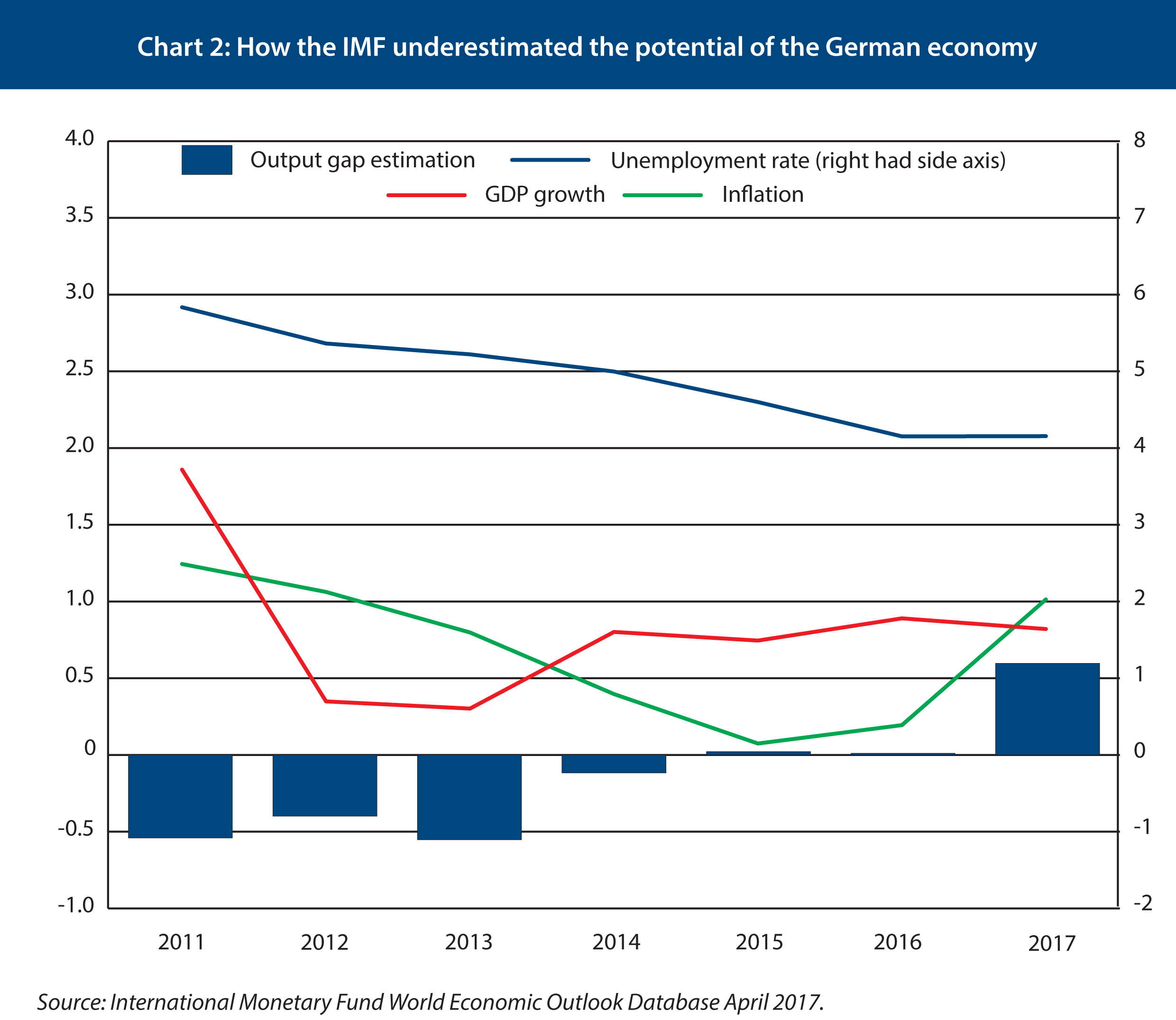

The International Monetary Fund (IMF) thought the German economy was running at close to full capacity as far back as 2014 (see Chart 2). But the German economy continued to grow (red line), unemployment fell further (green line), while inflation fell to close to zero (purple line). In short, Germany’s economic potential was larger than economists thought at the time, which gave the treasury additional leeway to spend in subsequent years.

The IMF reckons that the German economy will run above potential this year. Negotiated wage settlements have indeed picked up, signalling a growing shortage of workers (even though the recently reported 3.8 per cent increase was an outlier). But other indicators show the economy has yet to reach potential and may allow the next finance minister room to spend: there are more migrants coming to Germany (net immigration was 1.1 million in 2015, the latest available data), adding to the available pool of labour, and the so-called underemployment rate (U6), which adds unemployment and part-time workers who would like to work more, still stands at over 9 per cent.

Tax revenues may also provide more space for a fiscal stimulus. The Treasury’s current job is to calculate how much revenue to set aside for bad times to respect the debt brake mechanism. But German tax revenues have been higher than expected for several years, in part because the German economy is changing: exports are less of a driver of demand than domestic consumption and (by German standards) a property boom, and both are more heavily taxed than exports. Tax revenues are likely to continue to surprise on the upside.

Germany’s next government will spend and cut taxes. Impact on the eurozone depends on the #ECB #BTW2017

The second reason why Germany’s fiscal policy will become more expansionary is that the debt brake is not aggressive enough for a country that is part of a monetary union. In a monetary union, the most important tool for counteracting the ups and downs of the business cycle is outside individual countries’ control: monetary policy. The ECB has to set interest rates for the eurozone average, not for, say, Germany alone. As a result, countries have to use fiscal policy more aggressively to lean against the boom, and spend to contain a recession.

Germany’s debt brake is ill-suited for that purpose. In fact, it is designed to be passive: in a recession, it simply allows the additional amount of spending that a recession automatically generates, since government spending on unemployment benefits rises and tax revenues fall. Such ‘automatic stabilisation’ might be enough in a country like Sweden, where the Riksbank can adjust interest rates to Swedish needs and thus help stabilise the economy. In a eurozone country like Germany, such fiscal policy on autopilot is not enough to counteract a slump or a boom. In current circumstances, the debt brake will allow the German economy to run above potential, instead of prescribing the sort of fiscal policy that would prevent the economy from overheating.

The third reason why German fiscal policy is likely to become more expansionary is that so far, the government has not used up all the fiscal space that the debt brake allowed. In fact, Finance Minister Wolfgang Schäuble spent a cumulated €130 billion at the end of 2016 less than would have been allowed under the constitutional debt rules. Politically, it is unlikely that the next government will run up surpluses beyond the level mandated by the debt brake. The political differences between the likely coalition partners FDP, the Greens and the CDU are large, and one way to bridge them is by spending more on each party’s preferred project: tax cuts for FDP and CDU, investment for the Greens. Moreover, current projections of tax revenues show it is mostly state and municipal tax revenues that are coming in above target, not those of the federal government. Most states and municipalities will be keen to take advantage and spend and invest those funds as soon as possible.

What would be the effects of a fiscal expansion in Germany on the eurozone as a whole? At first, German companies and workers would be able to cover the demand generated by any increase in public investment and spending. The so-called ‘first-round’ or direct effect on the rest of the eurozone would thus be small. Given the close integration of the German economy with Central and Eastern European economies, these countries would probably benefit the most.

The ‘second-round’ effects on the eurozone are bound to be larger. If public spending leads to more revenues at German companies, higher German employment and wages, these firms and workers would spend more on domestic but also foreign goods and services, such as new machines or holidays in Italy. This effect is larger, the closer Germany is to its economic potential: any additional demand would have to be met through imports as the economy cannot produce much more.

The third and most important economic impact concerns monetary policy. The ECB’s job is to keep the economy close to potential and inflation at close to 2 per cent. A German fiscal stimulus would add to economic activity and inflation, which would in turn prompt the ECB to consider tightening monetary policy to prevent the economy from overheating. Increasing eurozone interest rates not only makes borrowing more expensive for all, it also increases the value of the euro, thus hurting exporters in the entire eurozone. This is why, in normal times, a German fiscal stimulus would have a limited effect on the rest of the eurozone economy.

Schäuble spent a cumulated €130bn less than would have been allowed under the constitutional debt rules

But these are not normal times. The eurozone economy has been running below potential for eight years straight and is likely to do so for two more years, according to estimates by the IMF. The ECB has, in part thanks to its own mistakes, struggled to get the economy back to potential and inflation back to target. Currently, inflation is accelerating – to 1.5 per cent in August – but the euro is also appreciating. A stronger currency usually pushes inflation down. Meanwhile, the underemployment rate U6 in the eurozone stands at 18 per cent, up from 14.5 per cent at the eve of the financial crisis in 2008. (It is 10.5 per cent in the US.) Under these circumstances, a German fiscal stimulus could boost the eurozone economy: if monetary policy is struggling to revive economic growth sufficiently to get inflation back to target, expansionary fiscal policy would add welcome additional spending.

How will the ECB react to a German fiscal stimulus? The ECB has pushed interest rates very low; short-term rates are even negative. It has also promised to keep rates low for a long time and bought public and private assets, to help bring down long-term interest rates. Given that inflation remains stubbornly below target, it is unlikely that the ECB is happy with the state of the economy. But many in Germany are calling for the central bank to start reducing its monetary stimulus sooner rather than later. With a more expansionary fiscal policy in Germany, such calls would only strengthen.

In order to make sure that a German fiscal expansion helps the eurozone economy, the ECB needs to reaffirm its intention to keep monetary policy accommodative until the single currency area’s economy has fully recovered. The ECB should communicate more strongly that it intends to let inflation overshoot its target for a while, to make up for missing its target several years in a row. Such a renewed commitment would allow the German economy to mildly overheat, help to reduce Germany’s current account surplus – but without hurting the rest of the eurozone with higher interest rates and a stronger euro.

~~~

Christian Odendahl is chief economist at the Centre for European Reform.