Of all the things that investors do, the selection, hiring and firing of managers is simultaneously the most important and yet perhaps the thing most investors are least equipped to do.

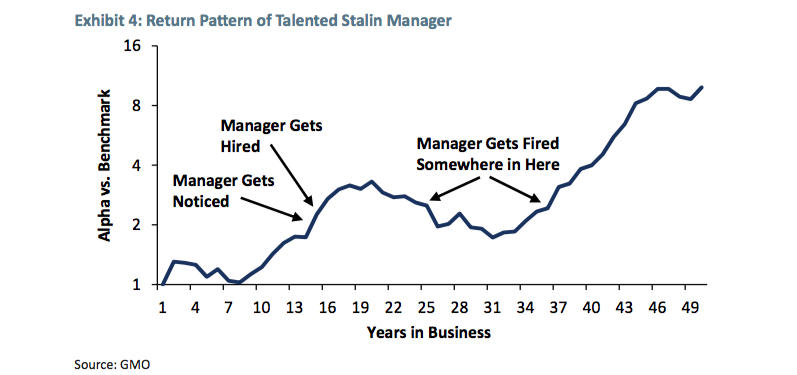

I was reminded of that when I saw the chart above, via Ben Inker of GMO. If you look at it from the right perspective, you might find a humorous side to the issue of manager selection. Inker’s perspective is interesting, and whether you agree or disagree with him, his quarterly commentary is always worth reading.

My selective perception — the lens with which I view everything, including his chart — sees this as a case study in investor psychology. The early rise is how any manager comes to the public’s attention; implied in this is how investors pile in into the fund on the mere strength of this publicity, often without doing the requisite research and due diligence. This big pop leads to a few years of undistinguished performance and investor impatience — where the manager may very well be doing exactly what their fund is supposed to and what their process requires — but to the casual buyer, none of that matters. The manager then gets fired. Of course, not long too long after this moment, the market cycle turns and the same environment/sector/cycle that led to the initial outperformance and good performance returns. The next few years are outstanding.

This is no surprise. It is also why so many investors (buy high, sell low) underperform their own holdings.

My own biases make me wonder:

-Did the original investor understand what they were buying?

-Were they looking at a fund that had an outstanding and replicable process, or did they merely buy a prior good outcome, hoping it would keep recurring?

-Was the manager under consideration truly skillful, or merely lucky?

-Was the original fund purchase made on the basis of rational decision making, or was it an undisciplined or emotional choice?

-Does the investor themselves have the requisite selection skillset (and time and money) to review, rank and evaluate managers, in order to determine which of them are appropriate for their portfolio?

That last issue raise the fascinating topic of meta-cognition — meaning: Is the allocator self-aware enough to evaluate their own ability to make that sort of manager selection? As we have learned via psychologists Dunning & Kruger, not only do most of us not have that skill set, very few of us have the tools to self-determine if we in fact do.

Note we are reviewing these concerns from a slightly different argument than the active versus passive debate. As we discussed last week, one should always be reviewing your own beliefs when confronted with contrary evidence. Per that, I am willing to admit that a handful of true alpha creators are at work today, and if you have dollars with them, well then that is terrific and you should stay with with. There are a handful of rare managers who have incredible skills — be it identifying mispriced assets, stock selection, market timing, or even selecting other managers.

Finding these folks is a huge undertaking and a stunningly difficult challenge to undertake. If you are one of the lucky few, then by all means don’t mess with what is working.

On the other hand, if you are unsure if you have the rare set of abilities to review, evaluate and monitor those managers, if you cannot confidently make a distinction between Process vs. Outcome, Luck vs. Skill, Rationality vs. Emotions, or if you are unsure that you possess the ability to honestly assess your own capabilities, then you might need some assistance.

If you’re looking for portfolio guidance and investment counseling, talk to us now.

Previously:

When Do You Fire a Manager? (TBP, April 5, 2011)

When should you fire your mutual fund manager? (Washington Post, May 8 2011)

Is Anyone Any Good at Picking Hedge Fund Managers? (TBP, January 23, 2012)

The mutual funds and managers to avoid (Washington Post, May 4 2012)

A Pension Fund Comes to Its Senses (Bloomberg, July 17, 2015)

Being a Stock-Picker Is Just So Hard (Bloomberg, August 11, 2017)