Share Buybacks Work Better in Theory Than in Practice

The main problem is that effects of bad decision-making don’t become clear until much later.

Bloomberg, March 12, 2018

The Corporate Finance Institute says stocks buybacks are a “win-win situation for both companies and shareholders.” Some members of the CFA Institute, which publishes the Financial Analysts Journal, take a different view: “favorable regulatory and tax treatment of buybacks is misguided and should be reformed.”

So, are buybacks a “win-win,” and if so, for whom?

There has been a robust debate on this subject. Patrick O’Shaughnessy (of O’Shaughnessy Asset Management) discussed the power of share repurchases. Cliff Asness (of AQR Capital Management) has termed the knee-jerk opposition to these operations “Buyback Derangement Syndrome.” AQR’s white paper of the same name raises the point that much of the criticism of share buybacks cannot be demonstrated mathematically. Looking at the impact of repurchases on the overall equity market, AQR finds that “in aggregate share repurchase activity is far less nefarious” than it has been depicted.

I am sympathetic to those arguments. However, looking at “the aggregate” may miss some specific issues. These are linked to the way buybacks are distributed among companies in the market: share repurchases are skewed by the very largest ones. As my colleague Ben Carlson has pointed out, the “top 20 companies in terms of buybacks accounted for almost 50 percent of total expenditures.” 1 While we never want to argue from anecdote or outlier, that lopsided distribution is so egregious that it must be taken into account.

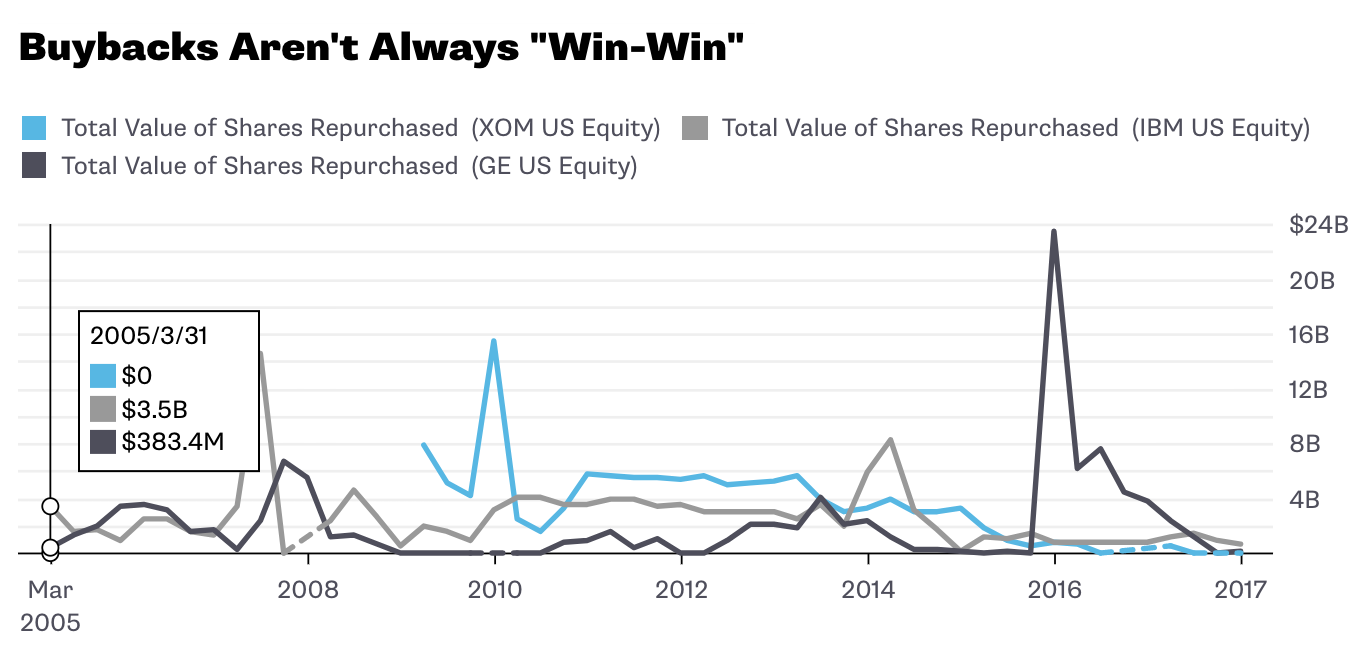

When we looked at buybacks in 2015, 2 the share repurchasers we considered were Caterpillar, Wal-Mart and Dell. 3 The companies we will look at today are IBM, GE and Exxon-Mobil.

When buybacks are announced, they are often greeted with glowing headlines, such as “General Electric Stock Buyback Returning Value to Shareholders.”

Yet there often is a lack of follow-up. Over the past three years, GE has made more than $50 billion in share buybacks. Since September 2016, when the article above was published, the stock price has been cut in half, from more than $30 to less than $15 recently. The value of the company is now $130 billion less than it was in the early days of that repurchase program. With the benefit of hindsight, we see that GE executives — like so many other corporate managers — are terrible repurchasers of their own company’s stock.

IBM has been another big user of this method. It has bought back more than $50 billion dollars in shares over the past five years. In March of 2013, its stock price peaked at about $215; it traded recently at a little more than $159, a drop of about 26 percent. The $50 billion market capitalization decrease over that period accounts for the buybacks.

Exxon Mobil is the biggest of the stock repurchasers. Over the past decade, according to Reuters, the oil giant has announced $210 billion in buybacks. Shareholders do not have a lot to show for it. Ten years ago, the stock price was $87; today it is under $75. (It peaked in 2014 at more than $100).

Reducing share count makes the earnings of each share higher. At the same time, however, it exchanges a corporate asset (cash) for the reduced share count. All things being equal, market capitalization falls proportionately. If a company is lucky, a rise in stock price more than makes up for the decrease in capitalization. Apple is the current best example of that in share buybacks, but it is, in many ways, a unique company.

The main problem with buybacks is that effects of bad decision-making don’t become clear until much later. To paraphrase Jeff Macke, stock buybacks are an allocation decision that has a hypothetical value to shareholders, but a real explicit value to option-holding executives. These people are supposed to be managing companies for the long term but get compensated over the short term. This misalignment if incentives should be a concern. It does seem like those with a vested short-term interest in stock prices put a thumb on the scale away from investments or dividends and towards buybacks.

There must have been a better use of those funds than stock buybacks. IBM created Watson, more or less as a publicity stunt. While the company was not investing in turning that into a product, Amazon rolled out its Echo, powered by Alexa. GE missed a number of opportunities over this period, as did Exxon.

Perhaps the biggest issue with buybacks is that they avoid risk taking (and a binary, win/lose outcome) for those dollars. The data analytics guru Nick Maggiulli recently wrote that “the biggest risk you can take in life is taking no risk at all.” Corporate managers would do well to heed his advice.

Orginally: Share Buybacks Work Better in Theory Than in Practice