The Future of the Right by Bruce Bartlett Published on Twitter 8/20/2022 I’m glad to see right-wingers abandoning Trump, but...

The Future of the Right by Bruce Bartlett Published on Twitter 8/20/2022 I’m glad to see right-wingers abandoning Trump, but...

Read More

The Day That Richard Nixon Changed U.S. Economic Policy Forever Fifty years ago, in response to rising inflation, he rejected...

The Day That Richard Nixon Changed U.S. Economic Policy Forever Fifty years ago, in response to rising inflation, he rejected...

Read More

It Took the Democrats Half a Century to Rediscover Trickle-Up Economics While Republicans cling to trickle-down delusions, Biden is...

It Took the Democrats Half a Century to Rediscover Trickle-Up Economics While Republicans cling to trickle-down delusions, Biden is...

Read More

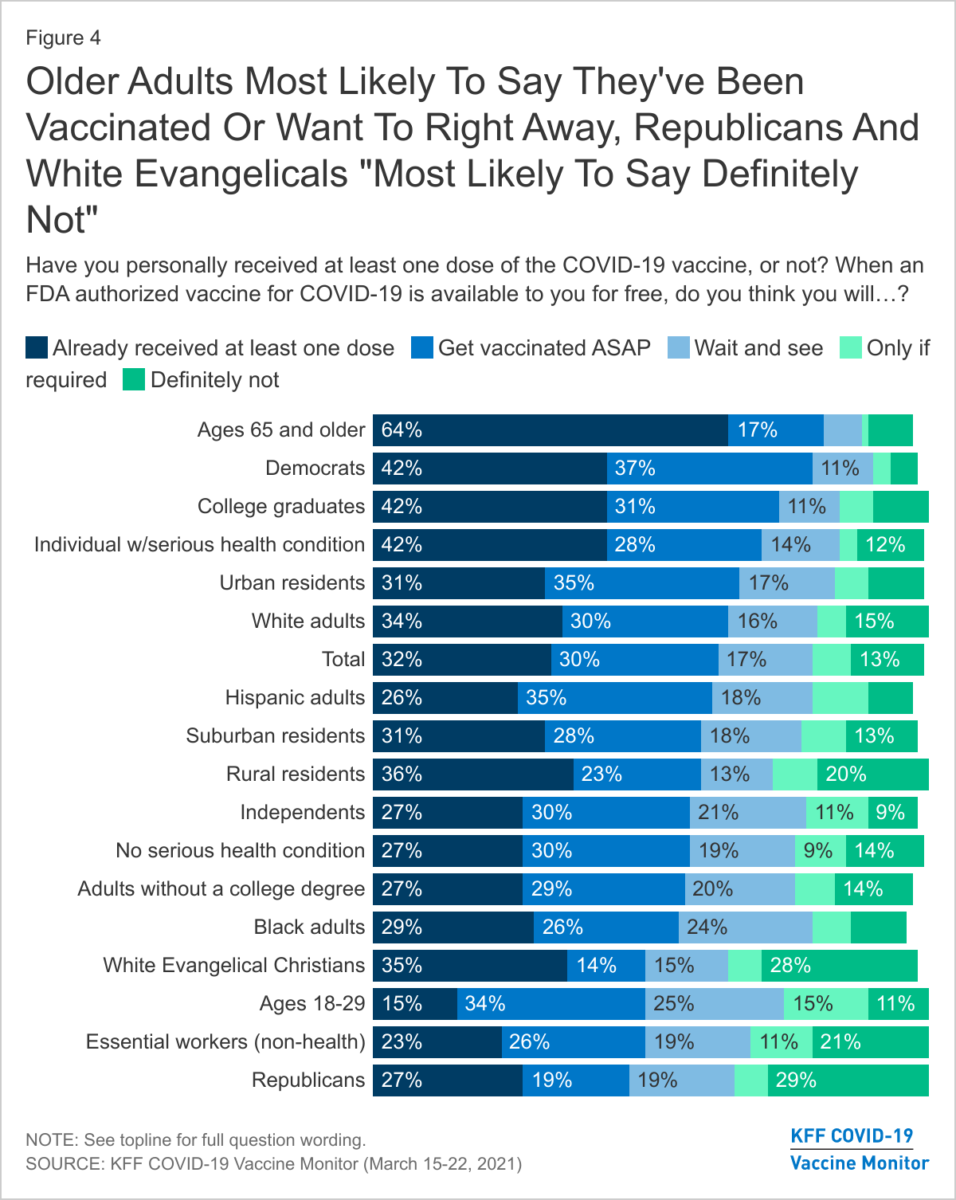

Vaccine Hesitancy and the Long Shadow of Racism in U.S. Health Care Nearly a third of Black Americans are taking a wait-and-see approach...

Vaccine Hesitancy and the Long Shadow of Racism in U.S. Health Care Nearly a third of Black Americans are taking a wait-and-see approach...

Read More

Washington’s Inflation Hysteria Is Fueled by Corporate Greed With the help of Larry Summers and a battery of...

Washington’s Inflation Hysteria Is Fueled by Corporate Greed With the help of Larry Summers and a battery of...

Read More

Remembering the Father of Supply-Side Economics Robert Mundell’s theories spawned decades of economic debate and still...

Remembering the Father of Supply-Side Economics Robert Mundell’s theories spawned decades of economic debate and still...

Read More

Socialism Is as American as Apple Pie The ideology that Republicans love to hate is woven through the fabric of the...

Socialism Is as American as Apple Pie The ideology that Republicans love to hate is woven through the fabric of the...

Read More

Republicans Greet Covid Stimulus with Another Round of Inflation Fearmongering Their cry-wolf act is well practiced but lacks...

Republicans Greet Covid Stimulus with Another Round of Inflation Fearmongering Their cry-wolf act is well practiced but lacks...

Read More

I Was a Rush Limbaugh Whisperer His radio show was once a vital outlet of conservative news—and I was one of his sources. But it became...

Read More

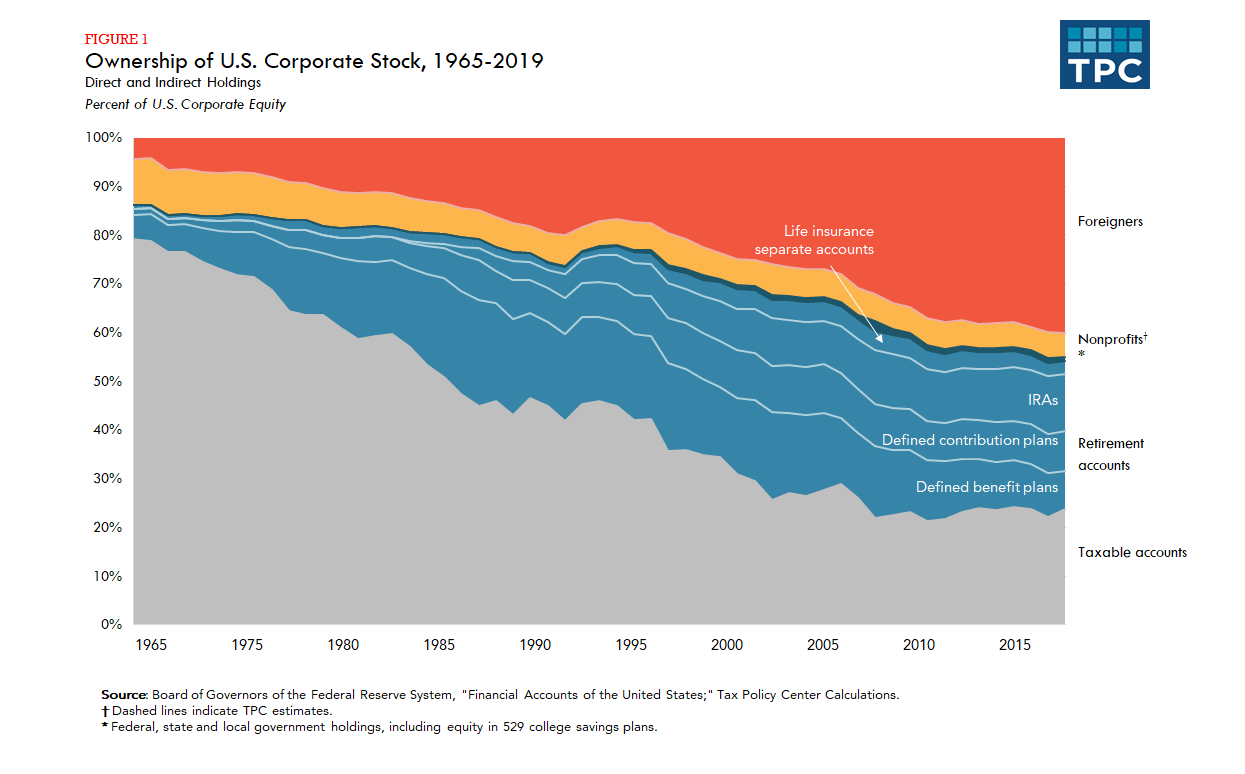

The GameStop Saga and the Incoherent Politics of the Stock Market Republicans have long encouraged stock ownership in the belief that it...

The GameStop Saga and the Incoherent Politics of the Stock Market Republicans have long encouraged stock ownership in the belief that it...

Read More