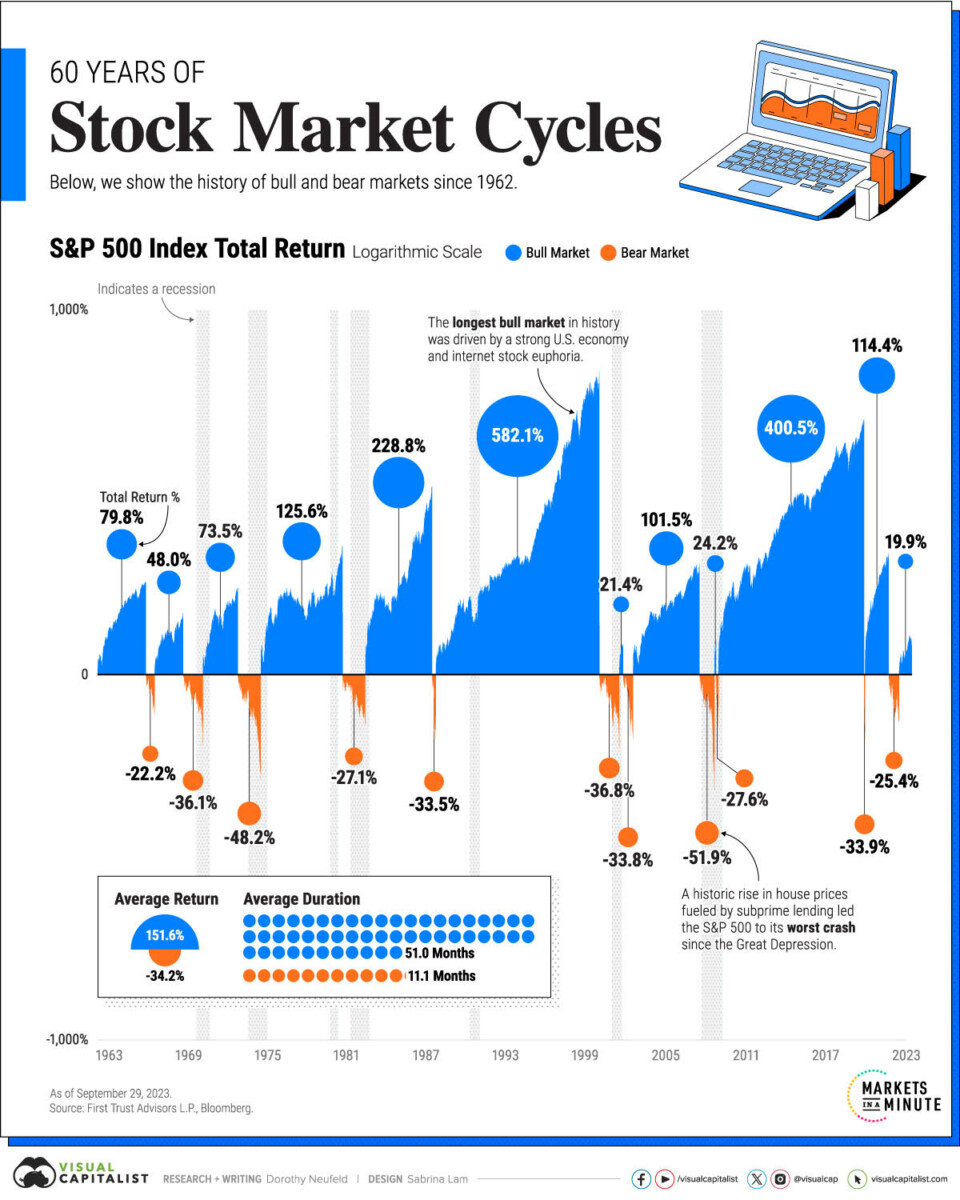

Source: Visual Capitalist

Source: Visual Capitalist

The Challenging Middle

Percentage of S&P 500 Stocks Above Their 200-Day Moving Average We now enter the most challenging part of the bear market:...

Percentage of S&P 500 Stocks Above Their 200-Day Moving Average We now enter the most challenging part of the bear market:...

Valuations, Cycles & Bubbles!

Tomorrow, I am giving a webinar presentation at Princeton’s Bendheim Center for Finance at 12:30pm. The topic is...

Tomorrow, I am giving a webinar presentation at Princeton’s Bendheim Center for Finance at 12:30pm. The topic is...

Managing Your Investments Late in the Cycle

Source: Fidelity How to Manage Your Investments Late in a Cycle Nobody knows for sure whether equities will keep rising or for how...

Source: Fidelity How to Manage Your Investments Late in a Cycle Nobody knows for sure whether equities will keep rising or for how...

BBRG: How to Manage Your Investments Late in a Cycle

How to Manage Your Investments Late in a Cycle Nobody knows for sure whether equities will keep rising or for how long, but knowing a...

How to Manage Your Investments Late in a Cycle Nobody knows for sure whether equities will keep rising or for how long, but knowing a...

How Externalities Affect Systems

It took about a billion years for life – single cell organisms — to develop on planet earth. Another 500 million years led...

It took about a billion years for life – single cell organisms — to develop on planet earth. Another 500 million years led...

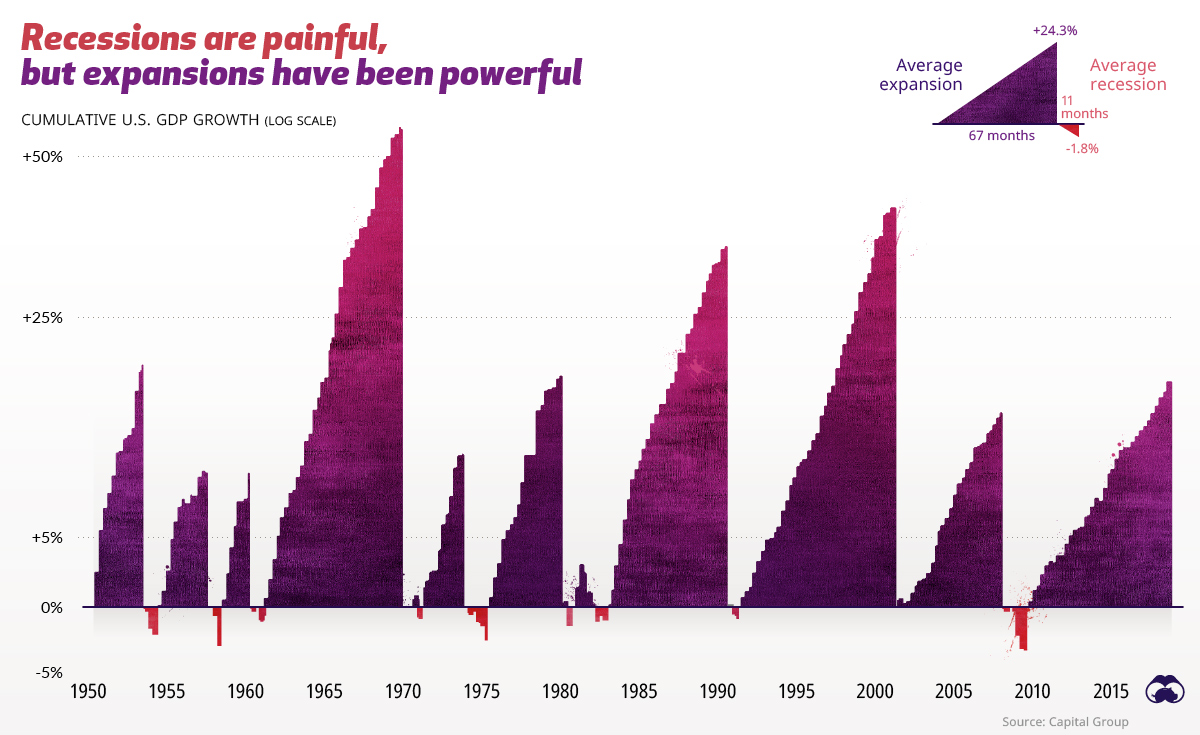

Guide to Recessions

Everything You Need to Know About Recessions Source: Visual Capitalist Persuasive guide to what recessions look like via...

Everything You Need to Know About Recessions Source: Visual Capitalist Persuasive guide to what recessions look like via...

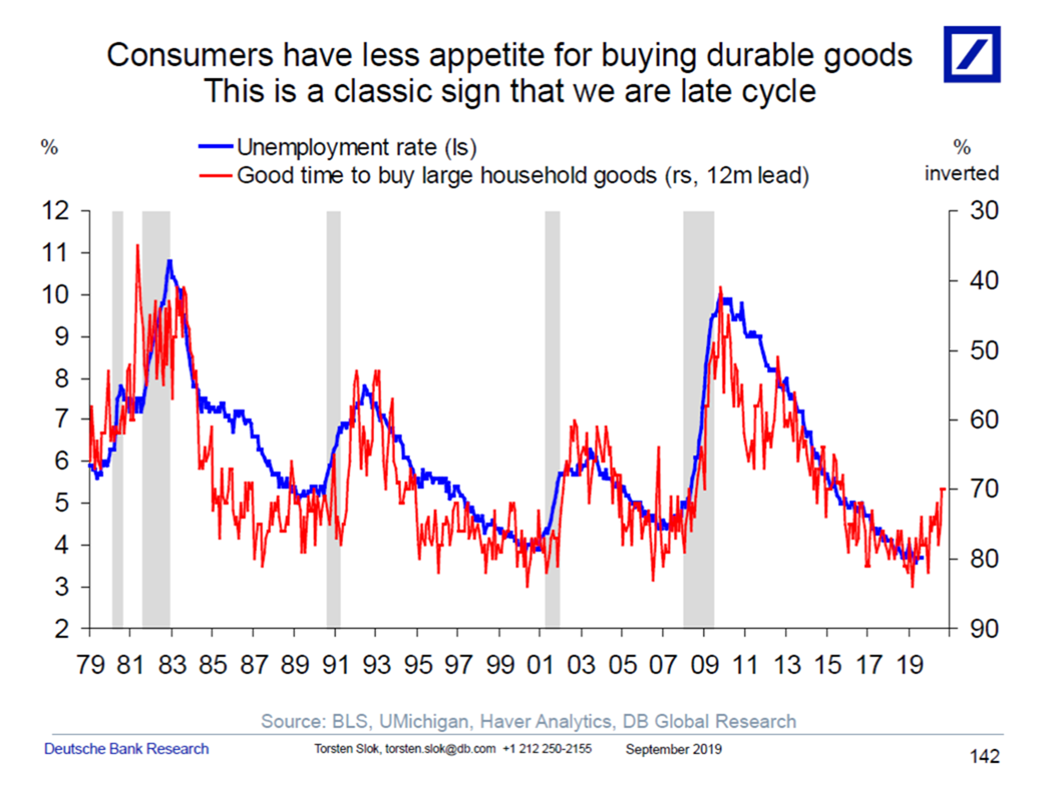

Where Are We In the Cycle?

From Torsten Sløk, Deutsche Bank Securities: Ten different indicators suggest that we are late cycle: 1. Growth in temp staffing...

Recession Risks Rise

From Torsten Sløk, Deutsche Bank Securities: Source: Torsten Sløk, Deutsche Bank Research From Torsten Sløk: For the past year,...

From Torsten Sløk, Deutsche Bank Securities: Source: Torsten Sløk, Deutsche Bank Research From Torsten Sløk: For the past year,...

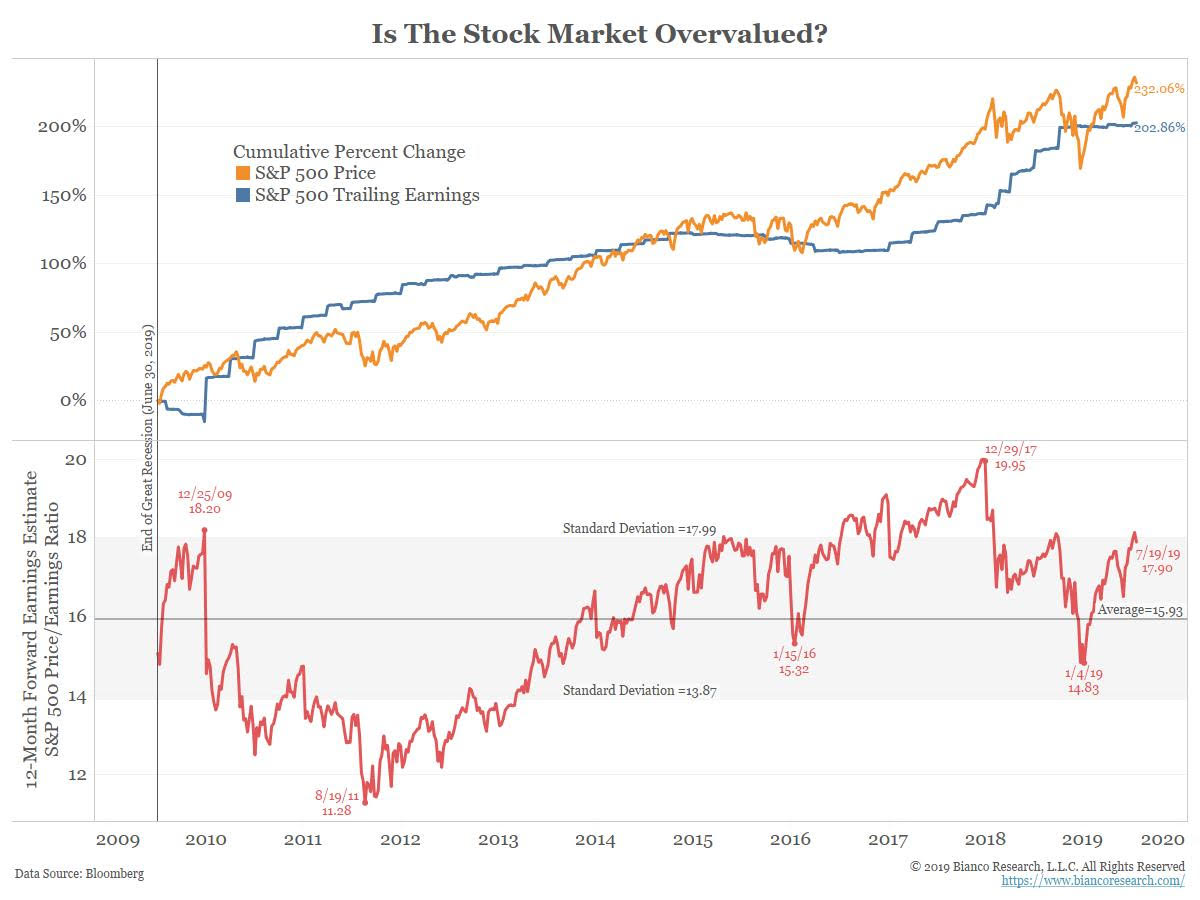

Bull Market: Earnings or Multiple Expansion?

Source: @biancoresearch One of the least understood details of the great 1982-2000 bull market was just how significant the...

Source: @biancoresearch One of the least understood details of the great 1982-2000 bull market was just how significant the...