So let me make sure I completely understand this: If we back out all of the inflationary data from the CPI, and PPI, there is, um, no inflation?

Thanks for clarifying that.

While the Dismal Set — and the majority of CNBC guests — continue to spout such foolish nonsense, its nice to see that at least the WSJ wasn’t bamboozeled. Their online headline read: Consumer Prices Climb 0.5%

“Gasoline prices shot up 8.3%, the biggest increase since February 2003.

Food prices, however, were unchanged for the first time in nine months.

Medical-care prices were unchanged after nearly 30 years of increases.

Housing prices grew more slowly in August, falling to a 0.2% rate from

0.4% in July. Automobile prices fell 0.5%, half the rate of decline

recorded in July.”

You can see more from the dismal set below . . .

UPDATE I: September 16, 2005 10:54 am

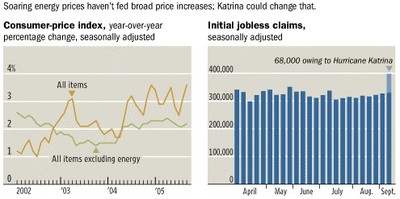

Its the ultimate Hedonic adjustment: Chart of the Day shows us graphically that without the items that are going up in price, there is hardly any inflation at all!

UPDATE II: September 17, 2005 11:54 am

The first official chart from the weekend WSJ:

UPDATE III: September 24, 2005 2:54 pm

Here’s a round up of all our recent discussions on inflation

Sources:

Consumer Prices Climb 0.5%

Katrina Helps Propel Jobless Claims

To Highest Level in Nearly 10 Years

WALL STREET JOURNAL, September 15, 2005 5:44 p.m.

http://online.wsj.com/article/0,,SB112678676740241720,00.html

Consumer prices rose 0.5% in August, but excluding volatile food and energy costs, the core inflation rate held steady at 0.1%. Economists, who weren’t surprised by the numbers, weighed in on the post-Katrina inflationary effects of energy prices and what the trends might mean for the Federal Reserve’s meeting on interest rates next week. Following are a handful of economists’ reactions.

Please name the few Economists you think make some sense, based upon their quotes, in the comments section (below).

Core consumer inflation appears to have peaked after rising for most of the past 18 months.

— Steven Wood, Insight Economics* * *

[P]rospects for a reversal of recent energy-price increases and the absence of other fundamental inflationary pressures indicates inflation provides no significant justification for raising interest rates further at this time.

— Peter Morici,University of Maryland* * *

[W]hile core inflation could well inch up in the coming months, particularly as some of the recent surge in energy prices leaks through, it is unlikely to accelerate by enough to scare the Federal Reserve into a more aggressive tightening mode. We continue to think that a trend of [quarter percentage point] tightening moves are likely at upcoming Federal Open Market Committee meetings (although the aftermath of Hurricane Katrina could cause a temporary pause in the process).

— Joshua Shapiro, MFR Inc.* * *

[We] are still concerned about the potential for either energy price pass-through or higher inflation expectations becoming embedded in the economy as a result of high gasoline prices.

— John Ryding, Bear Stearns* * *

Since more than 90% of the prices in the August survey were collected before Hurricane Katrina struck, the September and October headline CPI numbers will likely be even higher. … Given recent increases in airline ticket prices and the increasing ability of shippers and truckers to pass on higher fuel prices, we will likely see an acceleration of core inflation in the next few months. … Currently Global Insight predicts that the Fed will take a breather in one or both of the next two meetings, before resuming its tightening cycle.

— Nariman Behravesh, Global Insight* * *

[T]he headline CPI could be up as much as 0.8% in September mainly because of surging prices at the gas pump. … We expect to see only a slight uptick [in core inflation] in coming months partly reflecting a reversal of the [downside] quirk in hotel rates. … [W]e look for the core CPI to reach +2.7% by the end of 2006 as some of the recent energy spike is gradually passed through to prices of other goods and services.

— David Greenlaw, Ted Wieseman, Morgan Stanley

Source:

Economists React

Wondering When Energy Costs Will ‘Leak’ Into Core Prices

September 15, 2005 11:04 a.m.

http://online.wsj.com/article/0,,SB112679027103541749,00.html

real average hourly earnings fell 0.5% and are down 1.1% from a year ago. Real total income growth had been positive but is likely to turn negative over the next few months.

If you are going to look at the impact of higher energy prices on the economy you need to look at the overall

inflation rate.

Moreover, it is the overall inflation rate, not core inflation that determines inflation expectations that fees into the wage setting mechanism.

If the Fed is going to keep higher energy prices from leading to higher overall inflation it needs to generate sufficient economic weakness to offset the impact on inflation expectations.

There is a new measure of core inflation called “Hard Core Inflation” which is the CPI excluding all-items. It’s easy to track the history and easy to forecast!

Shhh. Icks-nay on the inflation-talksay. If we have inflation, the Fed will have to keep raising rates, and the market doesn’t want that.

I am always surprised when smart people say silly stuff. The monthly moan that economists don’t understand inflation comes from people who don’t understand inflation.

Inflation is a “general” rise in prices. The cost of living goes up when gasoline prices spike and other prices don’t fall enough to offset that rise. That does not necessarily qualify as inflation, because the rise is not widespread. What we have is a relative price rise – energy costs rising relative to all other costs.

Statistical agencies do not produce core price measures in order to hide inflation, or to argue that energy prices don’t matter. They do it to provide a convenient way to distinguish between generalized inflation and swings the prices of highly volatile components.

Fed officials, and central bankers around the globe, are fighting to prevent a relative price increase from spilling over, from sparking a generalized price increase. That is why they now talk less about energy prices as a drag on the economy and more about energy prices as a potential source of inflation.

Spencer’s points (as always) are apt, but need to be taken a step farther. We need to look at both headline price changes and relative price changes to fully understand the effect of price changes on economic activity. Firms that face higher input costs but are unable to pass them along respond very differently than those which can pass price hikes along. Think GM vs USP. Rising energy prices can spill over to cause generalized inflation (UPS) or be contained by lack of pricing power and cause contraction (GM, Newell, Owings Ill, Dana Corp).

Nobody with half a brain is trying to say that energy prices don’t matter. You are only obscuring the discussion when you pretend they are.

Its not just energy prices that are going up, its also lumber, food, health care, education, housing, cement, metals, raw materials, etc.

The sole reason to look at CPI/PPI Ex- Food and Energy is to remove the month-to-month volatility of the data series — The point is not, as so many cheerleaders have been doing, to show a lower level of inflation.

There are two reasons why inflation — even if it was only energy caused — is important to investors:

1) High Energy prices work their way into everything else, thanks to transportation costs — impacting the consumer, retail spending, etc.

2) Many companies have been unable to pass along all these price increases to their customers — after years of wringing out efficiency improvements, and with productivity slowing, there is a signficant chance that margins will get squeezed. That hurts profits, and may reduce P/E multiples.

And you know what that means . . .

Food prices are up 2.2% y/y, and have risen at just a 1.1% annualized pace over the past 3 months. Health care prices, while rising faster, have decelerated over the past 3 months. Education and community services prices have risen 1.8% over the past year and are climbing at just a 0.7% pace of the past 3 months. Deceleration is notable in many CPI components. While in nearly every case, prices are, as you say “going up”, they are going up at a very modest pace, and less rapidly than over the past 12 months.

Taking out volatility is a valuable reason for looking at core prices, but it overstates the case to say it is the sole reason for looking at core measures. As I tried to point out earlier, looking at divergences between headline and core price measures gives a fair hint as to whether rapid price gains are broadbased or limited to a few categories. Over the past year, rapid price gains have not been broadbased. Over the past 3 months, price gains have decelerated in many categories.

kharris,

Its not just the numbers, though, its how they are calculated. Nobody is arguing that price gains may be decelerating. The problem is that the gains that hurt the most are not being looked at; energy in terms of cost to the consumer and to the overall economy is a much bigger factor than the price of bread. You can stop or slow consumption of bread; how do consumers get around high energy prices, and how do producers do it?

It seems an economic fallacy to just say; people can stop using gas or use less of it. This has a direct effect on many layers of the economy and is also unfeasible for many; due to higher housing prices, for example, which are not accurately reflected in any inflation measure, many people live further and further away from where they might work, in a city for example. This cost cannot be removed or stopped; you still have to go to work everyday.

The general problem with looking at any statistic like this is that it will get twisted on purpose by each side to fit their mode. Why I lean on Barry’s side is that the overwhelming number of statistics point to short and long-term economic weakness; the economic cheerleaders ignore those statistics and tend to grab onto archaic stats like CPI ex-food and energy which does not really measure true economic state in and of itself.

“without the items that are going up in price, there is hardly any inflation at all! ”

I just -love- this statment! :)

It’s a perfect example of adequate “analysis” in this era of Bushinomics.

Along the lines of, “except for all the death and mayhem, everythings going great in Iraq!”

kharris – it’s telling that energy is *excluded* from the statistic instead of averaged/smoothed to eliminate near-term volatility. To pretend that the CPI must exclude this variable entirely, because no one knows how to exclude the volatility component, is to argue that the folks who calculate the CPI are incompetent instead of mischevious.

Oh, good. Yeah, let’s don’t have inflation anymore, just pay workers less. That way it will still make the charts look GREAT!

Love Republican thinking…..

Eric,

Nope. It’s just not true that “gains that hurt the most are not being looked at.” I do this stuff for a living, and I don’t know anybody who thinks gasoline prices don’t matter. This is one of the great fallacies about price measures. The public takes reference to core price measures as evidence that food and energy are being ignored. That is just wrong.

Nobody is arguing that the public can stop using gasoline. Bar stool economic pundits (up to and including CNBC, MSNBC and Fox News) just love this “no inflation as long as you don’t eat, smoke or drive” joke, but it is a caricature of economists’ thinking about inflation, not reality. That is my objection to Barry’s assertion that inflation is being ignored. Misconstruing others’ thinking is just not a productive activity. That, I think, is what happens every time somebody argues that all those dumb, or nefarious, economists don’t take energy into account when thinking about inflation.

Barry seems to think inflation is upon us. Others disagree. That is a legitimate point for debate. It is not true, however, that Fed officials, professional economists or other people who actually make use of the inflation data are generally benighted regarding the data’s uses or implications. Larry Kudlow? Sure, but he’s not a real economist. John Snow? Well he’s a salesman. It’s his job to obfuscate. Sherry Cooper? Mickey Levy? Alan Sinai? Tim Rogers? Brian Jones? No. They understand these thinks perfectly well. Paul Krugman? He understands.. Ben Bernanke? He understands, too (so far).

RP,

I am not aware of anyone associated with constructing official US inflation data who has argued that volatility cannot be dealt with through smoothing. Red herring there. To present smoothed data would be to make the data less useful. You can grab the data and smooth to your hearts content. If it were presented smoothed, you’d be stuck with the smoothed data. CPI data are delivered monthly. Note that the headline index does, in fact, include energy. So nobody is actuall pretending that “the CPI must exclude this variable entirely”, are they? That’s nonsense, and it’s nonsense that has legs because otherwise responsible people, like our host, say things that give it legs.

Who cares about core inflation?

This is another one of those months when you could report pretty much any number you like to summarize the current inflation rate, and, as William Polley noted, new…

Who cares about core inflation?

This is another one of those months when you could report pretty much any number you like to summarize the current inflation rate, and, as William Polley noted, new…

kharris> To present smoothed data would be to make the data less useful.

Then excluding it entirely makes it _____?

My point is that the Core CPI is useless, if one presumes real wages can go no where in a global labor smackdown.

Inflation will NEVER show up in the core CPI within this environment…in a world where everything is relative, a single number without a frame of reference is empty of meaning.

COLA adjustments are pegged to core inflation, correct?

That’s why food and energy are excluded from the equation.

Otherwise firms might be forced to raise salary 5% one year and, in theory, cut salary 3% the next.

The bottom line, however, is energy prices will continue to rise into perpetuity until a economically viable alternative source of energy is realized and brought to market. Until then, only a synchronized global slowdown will dampen energy prices and even then we may be shocked at how little the POO falls. The remaining question is which regional economy (Asia, Europe, US) blinks first.

ah, but you neglect the trimmed-mean PCE inflation rate at your peril :D http://www.dallasfed.org/data/pce/

cheers!

btw, if you’re worried about backing out, why not use the GDP deflator?

Here are a couple of reasons to believe that the core CPI rate has been rendered nearly useless as an indication of inflation:

http://www.gillespieresearch.com/cgi-bin/bgn/

(check the “Primer on Government Reports” links on the upper right side. It’s eye-opening how politics has influenced these important and allegedly neutral economic reports.

Here’s a cool diatribe about it too!

http://www.freerepublic.com/focus/f-news/927887/posts

Higher energy prices aren’t inflationary, they’re contractionary. Rising prices aren’t the cause of inflation, they’re the symptoms of inflation. The core rate is pretty tame right now. And has been for awhile.

Inflation is caused by an increase in the money supply. For example, say the government was going to spend, lets say, hundreds of billions, on a new underwater city somewhere, and they were going to do so by deficit spending. I’d expect that kind of monetary stimulus to show up in the inflation data down the road, wouldn’t you? All that money is going to be gobbling up short supplies of cement, lumber, labor, etc…

kharris,

If these economists understand the threat so well, where are the alarm bells? I don’t see those economists on TV warning of the dangerous effect of inflation. Instead what I see is more a marveling of the “low inflation, economic growth” argument, which seems to be the main economic viewpoint aired by the majority of economists you listed.

They seem more focused on asset markets and GDP numbers and on week-to-week numbers rather than analyzing more long-term economic trends that appear more troublesome by the month.

Re: muckdog

My Indian Engineering counterparts are experiencing a very Silicon Valley wage inflation startup frenzy right now – I hear wages are going up in the low-to-mid teens percentage-wise per year, presuming one can keep the engineers from leaving for a local startup. Higher energy prices are inflationary everywhere but the US, where they are contractionary because of the global imbalances. If you insist on using a canary like US real wages to tell you when inflation has arrived, I’d suggest you at least nail it to it’s perch.

It is a sign of the times that conspiracy thinking has even extended itself to such mundane activity as the calculation of the CPI. And, since all bad things are the result of George Bush and Republicans, including Katrina, Rita and the inability of any Cleveland sports team to ever win a national championship, it only stands to reason that the supposed manipulation of the CPI is also their fault.

More prosaically, there are some assumptions in the way the CPI are calculated that really don’t seem to make much sense. In particular, the way housing costs are measured seems odd. Instead of just using the change in the price of houses sold, the calculation uses rents as an alternative. During the recent period of rapid price appreciation, rents actually remained flat or even declined.

Your title alone has made my day!