Words from the (investment) wise for the week that was (November 24 – 30, 2008)

The holiday-shortened Thanksgiving week brought investors an additional item to be thankful for when stock markets closed higher for five consecutive trading days – a rare winning streak last accomplished in July 2007. The S&P 500 Index gained 19.1% since the start of the rally on November 21 and 12.0% on the week, registering the largest weekly gain since 1974.

Source: Daryl Cagle

Worrisome economic reports were cast aside by equity bulls, arguing that the bad news had already been priced in. However, US Treasury Note yields were less sanguine and fell to its lowest level on record, pointing to deflation concerns and suggesting that investors remained skeptical about the government’s latest moves to help revive the ailing economy. Importantly, US three-month Treasury Bills were trading at a minuscule 0.03%, indicating that liquidity was still being hoarded.

President-elect Obama stressed the need for quick action to expedite an economic recovery and introduced his administration’s economic team, including former Federal Reserve Chairman Paul Volcker as head of a new White House Economic Recovery Advisory Board tasked to revive growth in the US. Involving the 81-year Volcker in this way is a smart move by Obama.

A catalyst for last week’s stock market recovery was the announcement on Monday of the US government’s rescue plan for Citigroup (C), including a direct $20 billion investment and $306 billion in asset guarantees.

With credit markets still not thawing after the introduction of various central bank liquidity facilities and capital injections, the Fed on Tuesday unveiled further steps aimed at lowering borrowing costs for consumers and home buyers. The Fed will buy $100 billion of debt from Fannie Mae (FNM), Freddie Mac (FRE) and the Federal Home Loan Banks, and also purchase up to $500 billion of mortgage paper backed by the agencies. The Fed will furthermore lend $200 million to holders of key asset-backed securities regarding small business and consumer (auto, student, credit card) loans.

Source: The New York Times, November 25, 2008.

Commenting on the US government’s bailout actions and quoting from the Jerusalem Post, Bill King said: “There is one last thing that Hank, Ben and Geithner can do: ‘The country’s chief rabbis are calling for a mass prayer rally on Thursday in the hope that heavenly intervention will stem the global financial crisis.'”

Next, a tag cloud of the text of the dozens of articles I have devoured over the past week. This is a way of visualizing word frequencies at a glance. The usual suspects feature prominently, with “gold” attracting increasing attention.

Has the stock market reached a secular low or is it just bouncing off oversold levels? According to Fox Business Network, legendary investor Jim Rogers said: “We’re ready for a rally. I mean, the market in October and earlier this month has had a huge selling climax. I covered a lot of my shorts. Who knows if I’m right or not. But I expect the market to rally for some time. It may rally into next year. But … this is a false rally. It’s not going to be great. It’s not the end of the problems in America and it’s not the end of the bear market.”

A positive for the bulls is that the period post Thanksgiving through the end of the year has usually been a strong time for stocks. According to Jeffrey Hirsch (Stock Trader’s Almanac), “December is normally a banner month for stocks, ranking second [on the monthly calendar] for the Dow and S&P 500 and third for the Nasdaq.”

Should the bullish seasonal tendencies hold true on this occasion, possible first targets are the November 4 highs of 9,625 for the Dow (current level 8,829) and 1,006 for the S&P 500 (current level 896). This will also result in both indices clearing their 50-day moving averages.

“There is no doubt that time is needed for volatility to settle down before many will have the confidence to return to investing, but if one looks beyond the end of the year, 2009 will almost certainly be a better year for investors than 2008,” said David Fuller (Fullermoney) from London.

Although there is not yet conclusive evidence that we are leaving the corpse of the bear behind (especially with Q4 earnings disasters looming in January), it would appear that the nascent rally could have more steam left. (Also read my recent posts “Is the tide turning for stocks” and “Does the stock market rally have legs?“)

I am about to hit the road again – traveling to New York City – and blog posts will therefore take a back seat for the next week as I explore the Big Apple and meet with friends, blog readers and business associates in the cold weather and depressed economic climate.

Before highlighting some thought-provoking news items and quotes from market commentators, let’s briefly review the financial markets’ movements on the basis of economic statistics and a performance round-up.

Economy

“Global business sentiment is as dark as it has ever been, although the free fall in confidence may be over,” said the latest Survey of Business Confidence of the World conducted by Moody’s Economy.com. “Pessimism is pervasive across the entire globe, with the only distinction being that Asian businesses are somewhat less nervous than elsewhere. Pricing pressures are falling rapidly, although they are not yet consistent with outright deflation.” The global economy is suffering a severe recession according to the results of the business confidence survey.

Economic indicators released in the US during the past week all pointed to a deepening recession. According to Briefing.com, Q3 GDP was revised down to -0.5% from -0.3%, durable orders slumped by 6.2%, existing home sales fell by 3.1%, new home sales dropped by 5.3%, personal spending declined by 1.0%, and weekly initial claims, while improved from the prior week, continued to register a reading above 500,000.

The Chicago Purchasing Managers Index came in at 33.8, the weakest number since the serious recession of 1982. “The national number due next Monday will be just as ugly, as durable goods were down far more than expected, by a negative 6.2%,” added John Mauldin (Thoughts from the Frontline).

Commenting on the outlook for interest rates, Asha Bangalore (Northern Trust) said: “Going forward, real GDP is expected to show a decline that is upward of 4.0% in the fourth quarter of 2008. The Fed is widely expected to lower the Federal funds rate to 0.5% on December 16.” However, the Fed’s quantitative easing approach to monetary policy now seems to be targeting the quantity of money rather than its price.

Elsewhere in the world, the People’s Bank of China (PBoC) slashed its benchmark interest rates by 108 basis points and also lowered the reserve requirement for banks. This move indicates that China will be joining the rest of the world in a marked economic slowdown.

For the upcoming week, the European Central Bank and the Bank of England are expected to reduce interest rates by 50 and 75 basis points respectively in the light of a deteriorating economic outlook.

Week’s economic reports

Click here for the week’s economy in pictures, courtesy of Jake of EconomPic Data.

|

Date |

Time (ET) |

Statistic |

For |

Actual |

Briefing Forecast |

Market Expects |

Prior |

|

Nov 24 |

10:00 AM |

Oct |

4.98M |

5.07M |

5.05M |

5.14M |

|

|

Nov 25 |

8:30 AM |

Chain Deflator-Prel. |

Q3 |

4.2% |

4.2% |

4.2% |

4.2% |

|

Nov 25 |

8:30 AM |

GDP-Prel. |

Q3 |

-0.5% |

-0.3% |

-0.5% |

-0.3% |

|

Nov 25 |

10:00 AM |

Nov |

44.9 |

40.0 |

39.5 |

38.0 |

|

|

Nov 26 |

8:30 AM |

Oct |

-6.2% |

-2.2% |

-2.5% |

-0.2% |

|

|

Nov 26 |

8:30 AM |

11/22 |

529K |

535K |

537K |

543K |

|

|

Nov 26 |

8:30 AM |

Oct |

0.3% |

0.2% |

0.1% |

0.1% |

|

|

Nov 26 |

8:30 AM |

Personal Spending |

Oct |

-1.0% |

-0.6% |

-0.7% |

-0.3% |

|

Nov 26 |

9:45 AM |

Nov |

33.8 |

39.5 |

38.5 |

37.8 |

|

|

Nov 26 |

10:00 AM |

Mich Sentiment-Rev. |

Nov |

55.3 |

58.5 |

58.0 |

57.9 |

|

Nov 26 |

10:00 AM |

Oct |

433K |

450K |

450K |

457K |

|

|

Nov 28 |

9:45 AM |

Nov |

– |

NA |

NA |

NA |

Source: Yahoo Finance, November 28, 2008.

In addition to the Fed releasing its Beige Book (Wednesday) and interest rate decisions by the European Central Bank and the Bank of England (Thursday), next week’s US economic highlights, courtesy of Northern Trust, include the following:

1. ISM Manufacturing Survey (December 1): The consensus for the manufacturing ISM composite index is 38.4 versus 38.9 in October.

2. Employment Situation (December 5): Payroll employment in November is predicted to have dropped by 300,000 after 240,000 jobs were lost in October. The unemployment rate is expected to move up two notches to 6.7%. Consensus:Payrolls: -300,000 versus -240,000 in October, unemployment rate: 6.7% versus 6.5% in October.

3. Other reports:Construction spending (December 1), auto sales (December 2), ISM non-manufacturing, productivity and costs (December 3), and factory orders (December 4).

Markets

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online, November 28, 2008.

Equities

Global stock markets surged during the past week on the back of a combination of bargain hunting and short covering, albeit on light trading volume as a result of the Thanksgiving holiday in the US.

Both mature and emerging markets shared handsomely in the rally that commenced on November 21, as shown by the subsequent gains of the MSCI World Index (+15.7%) and the MSCI Emerging Markets Index (+13.5%). Notwithstanding the improvement, these indices are still down by 43.8% and 57.7% respectively for the year to date.

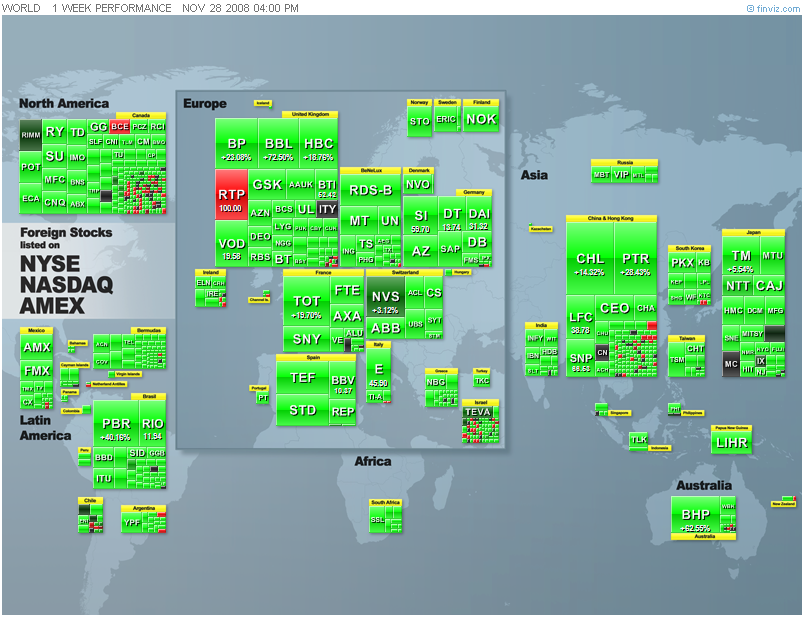

Click here or on the thumbnail below for a (delightfully green) market map, obtained from Finviz, providing a quick overview of last week’s performances of global stock markets (as reflected by the movements of ADR stocks).

The US stock markets all rallied sharply over the week as shown by the major index movements: Dow Jones Industrial Index +9.7 (YTD -33.5%), S&P 500 Index +12.0% (YTD -39.0%), Nasdaq Composite Index +10.9% (YTD ‑42.1%) and Russell 2000 Index +16.4% (YTD -38.2%).

The bar chart below, also from Finviz.com, shows the US sector performances over the week, and specifically how strongly financials and materials have recovered.

As far as industry groups are concerned, the automobile manufacturing group (+82%) was the top performer for the week. General Motors Corp (GM) and Ford Motor (F) rose by 71% and 88% respectively on the expectation that auto makers will receive a government bailout.

The homebuilding group (+59%) was the second-best performer on the prospect that the US government’s latest rescue package will result in lower mortgage rates and mortgage credit becoming more readily available.

Seven of the ten underperforming groups were from the three top-performing sectors for the year to date – consumer staples, health care and utilities. These sectors, which typically outperform in a declining market, tend to lag in a rising market such as the one experienced last week.

Interestingly, the percentage of S&P 500 stocks trading above their 50-day moving averages has increased from almost zero in October to 19% on Friday – a promising improvement.

I often get asked by readers about Richard Russell’s (Dow Theory Letters) latest views. This is what the old-timer said on Friday: “The big question now is whether the tide is in the early process of turning bullish. If so, we should be seeing a series of constructive, even bullish days. … I wonder whether my more aggressive subscribers shouldn’t jump the gun and maybe buy the Diamonds (DIA) at the opening on Monday.”

Fixed-interest instruments

The ten-year US Treasury Note yield declined to its lowest level since records began in 1958, closing 25 basis points lower on the week at 2.93% after falling as low as 2.82% earlier on Friday.

In addition to economic and deflation worries, Treasuries also benefited from lower mortgage rates as a result of the Fed’s decision to buy GSE-insured mortgage paper. The 30-year fixed mortgage rate dropped by 25 basis points to 5.84%.

“The lower mortgage rates threaten to trigger a wave of mortgage refinancing, the prospect of which has pushed investors to hedge that risk by buying ten-year Treasury debt, a benchmark for mortgage rates,” reported the Financial Times“.

The UK ten-year Gilt yield dropped by 9 basis points to 3.78% and the German ten-year Bund yield fell by 12 basis points to 3.26%. Emerging-market bonds also performed well, with the JPMorgan EMBI Global Index gaining 5.1% during the week.

Although some progress has been made as a result of central banks’ liquidity facilities and capital injections, the credit markets are not yet thawing (see my “Credit Crisis Watch” of November 28). The TED and LIBOR-OIS spreads have tightened since the panic levels of October 10, whereas the CDX and iTraxx indices have also shown some improvement over the past few days. However, US Treasury Bills and high-yield spreads are still at crisis levels.

Currencies

Most currencies rebounded against the US dollar during the past week as the greenback came under pressure as a result the Fed’s new measures to unclog the credit markets.

Over the week the US dollar lost ground against the euro (-0.8%), the British pound (-3.1%), the Swiss franc (-0.8%), the Japanese yen (-0.3%), the Canadian dollar (-2.4%), the Australian dollar (-3.7%) and the New Zealand dollar (-4.3).

The US currency also fell against emerging-market currencies such as the Brazilian real (‑7.7%), the Turkish lira (-6.0%) and the South African rand (-4.1%).

Interestingly, the Chinese renminbi (+6.9%) is the only major emerging-market currency that has appreciated against the US dollar over the year to date.

Commodities

The Reuters/Jeffries CRB Index (+4.7%) closed higher by the end of the week – only its fifth positive week since commodities peaked early in July. Arguing against a more lasting reversal of fortune for commodities, the Baltic Dry Index – a benchmark for shipping major raw materials, including coal, iron ore and grain, and generally an excellent barometer of economic activity – declined by 14.5% to its lowest level since 1987.

The graph below shows the movements of various commodities over the past week, indicating an improvement across the whole complex as a weak US dollar pushed prices higher.

Gold bullion (+3.4%) remained in favor with investors as a result of a solid supply/demand situation, store-of-value considerations and a positive-looking chart (see below). A research report from Citigroup, as reported by the Telegraph, said gold could rise above $2,000 within two years. Platinum (+6.9%) and silver (+7.6%) – massive underperformers since March – were also in demand last week.

In the aftermath of Thanksgiving, may I remind you of the following old stock market adage: “The bears have Thanksgiving and the bulls have Christmas.” Let’s hope for an early Christmas! Meanwhile, the news items and words from the investment wise below will hopefully assist in steering our portfolios on a profitable course.

That’s the way it looks from Cape Town.

Big Think: Beyond the crisis – conversation with Larry Summers, George Soros and Robert Merton

Source: Big Think, November 2008.

PBS News Hour: Taleb, the risk maverick

“Interview with Nassim Nicholas Taleb, famous economist and author of ‚The Black Swan’ and Dr. Mandelbrot, professor of Mathematics. Both say that the present economy is more serious than the Great Depression, and the economy during the American Revolution.”

Source: PBS News Hour (via YouTube), October 22, 2008.

IDD magazine: John Bogle – great expectations

“John Bogle founded the Vanguard Mutual Fund Group in 1974. He served as its chairman and chief executive until 1996 and remained on as senior chairman until 2000.

“Recently, he wrote ‘Enough: True Measures of Money, Business and Life’, which was published by John Wylie & Sons.

“To call it a business book – a how-to or memoir – would be too simplistic. In fact, it is far from the typical business book because it offers some interesting life lessons on dealing with people, especially clients and customers.

“Bogle spoke with IDD last week, offering his thoughts on long-term investing and how it may come back – as opposed to rapid-fire maneuvers in and out of a company’s shares – and his thoughts on PE fund managers as well as hedge funds. Not surprisingly, they are not positive.

“As Bogle sees it ‘we have made Wall Street too much of a casino. It is totally dominated by speculation … we are engaged in an orgy of speculation the likes of which has never been seen in the history of this country.’

“His rule of thumb for investors: your bond position should equal your age. ‘I’m about 80% bonds. I started 65% about 15 years ago,’ says Bogle.

“Following are excerpts from the interview:

“IDD: How do you think the credit crisis will play out?

“BOGLE: The market can’t bail itself out of this mess. Wall Street has a lot to answer for to Main Street and yet Main Street, which is really where the tax base is, is going to have to bail out Wall Street for Wall Street’s errors. And that is, of course, a tragedy – an economic tragedy. But I am persuaded because I respect people like Larry Summers, I certainly respect Ben Bernanke. I am not so sure about Hank Paulson. I suppose I respect him in a way, but his issue is that he is an investment banker. So it should come as no surprise to anybody that he looks at these things from an investment banker’s perspective. How else can he look at them? It [the bailout] has to happen. I think it is too bad it has to happen, but I think we ought to get ready for building a better financial system, which means building a smaller financial system because what is going on Wall Street is a casino and our croupier has raked too much off of the table before we get paid.

“IDD: When you say our financial system gets smaller, what do you mean by that?

“BOGLE: Revenues will be less for a whole bunch of reasons. First, they are never going to be allowed – with the government being part owners of them – to have 35-to-1 leverage. Number two, we’re going to have better disclosure about what is on that balance sheet. When you think about it, if you are leveraged 35 to 1 and all your assets are Treasury bills I don’t see that as much of a problem. The problem is that none of them are Treasury bills. They are toxic mortgages and we need much better disclosure of that. The third thing is that they are going to have to be content with less revenues.”

Click here for the full article.

Source: Aleksandrs Rozens, IDD magazine, November 17, 2008.

Spiegel Online: George Soros – “The economy fell off the cliff”

“George Soros, 78, has made billions as a hedge-fund manager and investor. Spiegel spoke with him about the current financial crisis, how he expects President-elect Barack Obama to respond to the economic disaster and the responsibilities borne by speculators.

“SPIEGEL: Mr. Soros, in spite of massive interventions by governments and federal banks the financial crisis is getting worse. The stock markets are in free fall, millions of people could lose their jobs. More and more companies are in trouble, from General Motors in Detroit to BASF in Ludwigshafen. Have you ever seen anything like it?

“Soros: Never. I find the present situation dramatic and overwhelming. In my latest book ‘The New Paradigm for Financial Markets: The Credit Crisis of 2008′ I predicted the worst financial crisis since the 1930s. But to tell you the truth: I did not actually anticipate that it would get as bad as it did. It has gone beyond my wildest imagination.

“‘I find the present situation dramatic and overwhelming.’

“SPIEGEL: What are your fears for the coming months?

“Soros: I think that the dark comes before dawn. The financial markets are under great pressure because of the lack of leadership during the transition period. In the next two months, the markets will experience maximum pressure. Then we will see some initiatives from the Obama administration. How long the crisis lasts will depend on the success of these measures.

“SPIEGEL: The markets don’t seem to have much confidence in the new president – in stark contrast to the enthusiasm in the population. Since Election Day on November 4, stocks have fallen by almost 20%.

“Soros: I have great hopes for Barack Obama. But at the time of the election the financial community had not yet fully grasped the magnitude of the economic decline. They did not anticipate that the default of Lehman Brothers would cause cardiac arrest in the markets. The economy fell off the cliff, you begin to see mangled bodies lying at the bottom.”

Click here for the full article.

Source: Spiegel Online, November 24, 2008.

The New York Times: Paulson on new moves in rescue plan

“CNBC coverage of opening remarks by Treasury Secretary Henry Paulson in a news conference describing new steps to ease credit markets.”

Click here for the article.

Source: The New York Times, November 25, 2008.

Asha Bangalore (Northern Trust): Fed institutes two more programs to support working of financial markets

“The Federal Reserve announced the creation of Term Asset-Backed Securities Loan Facility (TALF) in conjunction with the Treasury. The program that will involve the Federal Reserve Bank of New York lending up to $200 billion to holders of AAA-rated asset backed securities ‘backed by newly and recently originated consumer and small business loans’.

“The US Treasury Department, under the Emergency Economic Stabilization Act of 2008, will provide $20 billion of credit protection to the Federal Reserve Bank of New York for these non-recourse loans. The loans will involve a haircut based on the asset class and there is fee for participation.

“This new program is designed to address problems in the auto, student, credit card, and Small Business Administration guaranteed loans. Loans to consumers have become scarce because securitization of consumer loans has come to a standstill. Funding these loans should result in a resumption of the working of these markets. A date and details are being worked out.

“The Fed also announced it will start purchasing Government Sponsored Enterprises (GSE) – Fannie Mae, Freddie Mac, and Federal Home Loan Banks – this week. Spreads of these securities vis-à-vis Treasury securities have widened sharply in recent days. Purchases of $100 billion in GSE direct obligations and $500 of Mortgage Backed Securities will be undertaken under this program. The objective of this action is to increase the availability of credit for purchases of homes.

“These actions will raise reserves in the banking system and increase the size of the Fed’s balance sheet. The sum of today’s action is $800 billion. The Fed’s balance sheet as of November 25, 2008 had ballooned to 2.19 trillion from $995.57 billion as of September 17, 2008.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary, November 25, 2008.

Bloomberg: US pledges top $7.7 trillion to ease frozen credit

“The US government is prepared to provide more than $7.76 trillion on behalf of American taxpayers after guaranteeing $306 billion of Citigroup debt yesterday. The pledges, amounting to half the value of everything produced in the nation last year, are intended to rescue the financial system after the credit markets seized up 15 months ago.

“The unprecedented pledge of funds includes $3.18 trillion already tapped by financial institutions in the biggest response to an economic emergency since the New Deal of the 1930s, according to data compiled by Bloomberg. The commitment dwarfs the plan approved by lawmakers, the Treasury Department’s $700 billion Troubled Asset Relief Program. Federal Reserve lending last week was 1,900 times the weekly average for the three years before the crisis.

“When Congress approved the TARP on October 3, Fed Chairman Ben Bernanke and Treasury Secretary Henry Paulson acknowledged the need for transparency and oversight. Now, as regulators commit far more money while refusing to disclose loan recipients or reveal the collateral they are taking in return, some Congress members are calling for the Fed to be reined in.

“Bloomberg News tabulated data from the Fed, Treasury and Federal Deposit Insurance Corp. and interviewed regulatory officials, economists and academic researchers to gauge the full extent of the government’s rescue effort.

“The bailout includes a Fed program to buy as much as $2.4 trillion in short-term notes, called commercial paper, that companies use to pay bills, begun October 27, and $1.4 trillion from the FDIC to guarantee bank-to-bank loans, started October 14.

“William Poole, former president of the Federal Reserve Bank of St. Louis, said the two programs are unlikely to lose money. The bigger risk comes from rescuing companies perceived as ‘too big to fail’, he said.”

Source: Mark Pittman and Bob Ivry, Bloomberg, November 24, 2008.

Barry Ritholtz (The Big Picture): Big bailouts, bigger bucks

“Whenever I discussed the current bailout situation with people, I find they have a hard time comprehending the actual numbers involved. That became a problem while doing the research for the Bailout Nation book. I needed some way to put this into proper historical perspective.

“If we add in the Citi bailout, the total cost now exceeds $4.6165 trillion. People have a hard time conceptualizing very large numbers, so let’s give this some context. The current Credit Crisis bailout is now the largest outlay in American history.

“Jim Bianco of Bianco Research crunched the inflation adjusted numbers. The bailout has cost more than all of these big budget government expenditures combined:

• Marshall Plan: Cost: $12.7 billion, Inflation Adjusted Cost: $115.3 billion

• Louisiana Purchase: Cost: $15 million, Inflation Adjusted Cost: $217 billion

• Race to the Moon: Cost: $36.4 billion, Inflation Adjusted Cost: $237 billion

• S&L Crisis: Cost: $153 billion, Inflation Adjusted Cost: $256 billion

• Korean War: Cost: $54 billion, Inflation Adjusted Cost: $454 billion

• The New Deal: Cost: $32 billion (Est), Inflation Adjusted Cost: $500 billion (Est)

• Invasion of Iraq: Cost: $551b, Inflation Adjusted Cost: $597 billion

• ietnam War: Cost: $111 billion, Inflation Adjusted Cost: $698 billion

• NASA: Cost: $416.7 billion, Inflation Adjusted Cost: $851.2 billion

TOTAL: $3.92 trillion

“That is $686 billion less than the cost of the credit crisis thus far. The only single American event in history that even comes close to matching the cost of the credit crisis is World War II: Original Cost: $288 billion, Inflation Adjusted Cost: $3.6 trillion. The $4.6165 trillion dollars committed so far is about a trillion dollars ($979 billion dollars) greater than the entire cost of World War IIborne by the United States: $3.6 trillion, adjusted for inflation (original cost was $288 billion).

“I estimate that by the time we get through 2010, the final bill may scale up to as much as $10 trillion dollars …”

Source: Barry Ritholtz, The Big Picture, November 25, 2008.

Casey’s Charts: Budgeting your future

“The October statement of the US Treasury Department revealed that the federal deficit has reached the largest level on record. Over the last twelve months, the US government spent $618 billion dollars more than it was able to collect.

“The deficit is already enormous and with all signs pointing towards even greater government spending, the implications are astounding. Casey Research Chief Economist Bud Conrad predicts that next year’s budget deficit will be closer to the tune of $1.5 trillion!”

Source: Casey’s Charts, November 21, 2008.

Breitbart: IMF chief economist – worst of financial crisis yet to come

“The IMF’s chief economist has warned that the global financial crisis is set to worsen and that the situation will not improve until 2010, a report said Saturday. Olivier Blanchard also warned that the institution does not have the funds to solve every economic problem.

“‘The worst is yet to come,’ Blanchard said in an interview with the Finanz und Wirtschaft newspaper, adding that ‘a lot of time is needed before the situation becomes normal.’

“He said economic growth would not kick in until 2010 and it will take another year before the global financial situation became normal again.

“The International Monetary Fund on Friday promised to help Latvia deal with its economic crisis after it assisted Iceland, Hungary, Ukraine, Serbia and Pakistan.

“But Blanchard said the IMF was not able to solve all financial issues, in particular problems of liquidity.

“Withdrawals of capital leading to problems of liquidity ‘can be so significant that the IMF alone cannot counter them’, he said, adding that massive withdrawals of investments from emerging countries could represent ‘hundreds of billions of dollars. We do not have this money. We never had it,’ he said.”

Source: Breitbart, November 22, 2008.

The Wall Street Journal: Obama names his economic team

“Looking to hit the ground running on January 20 and restore confidence, President-elect Barack Obama seals up his economic appointments.”

Source: The Wall Street Journal, November 24, 2008.

Bloomberg: Obama names Volker to head panel on reviving economy

“President-elect Barack Obama named former Federal Reserve Chairman Paul Volcker to head a new White House economic board that will propose ways to revive growth as the US grapples with an ‘economic crisis of historic proportions’.

“‘At this defining moment for our nation, the old ways of thinking and acting just won’t do,’ Obama said at a news conference in Chicago, his third in as many days.

“Volcker, 81, will be chairman of the President’s Economic Recovery Advisory Board. The panel’s top staff official will be Austan Goolsbee, a University of Chicago economist who will also be a member of the president’s Council of Economic Advisers.

“The panel, which will include experts from outside government, will meet about once a month and periodically brief Obama with advice on how to shore up financial markets. Volcker’s position will be part-time.

“‘Sometimes policymaking in Washington can become too insular,’ Obama said. ‘The walls of the echo chamber can sometimes keep out fresh voices and new ways of thinking, and those who serve in Washington don’t always have a ground-level sense of which programs and policies are working.’

“Volcker, who throttled the economy to crush inflation in the 1980s, was an adviser to Obama during the presidential campaign. He was a candidate for Treasury secretary, a job that went to Federal Reserve Bank of New York President Timothy Geithner.

“‘He is one of the most independent-thinking guys you could find and brings massive reputation,’ Ethan Harris, co-head of US economic research at Barclays Capital in New York, said before today’s announcement.”

Source: Kim Chipman and Catherine Dodge, Bloomberg, November 26, 2008.

ABC News: Summers to be top white house economic adviser at NEC

“ABC News has learned that President-elect Obama has decided to name former Treasury Secretary Larry Summers the director of the National Economic Council, essentially the president’s senior economic adviser.

“Part of the Executive Office of the President, the NEC was created for the purpose of advising the President on matters related to US and global economic policy. The NEC has four functions, by executive order: ensuring that programs and policy decisions are consistent with the President’s economic goals, monitoring the implementation of the President’s economic policy agenda, coordinating policy-making for domestic and international economic issues, and coordinating economic policy advice for the President.

“Summers was the 71st Secretary of the Treasury, serving from July 1999 until the end of the Clinton administration in January 2001, having previously served as undersecretary for international affairs and deputy secretary of the Treasury. He also served as chief economist of the World Bank.

“At the Treasury Department in the 1990s, Summers worked closely with Tim Geithner, the man Obama intends to nominate to be the next Secretary of the Treasury. The two are said to have an excellent working relationship.

“Some Democrats say that Obama and Summers have an understanding that when current Federal Reserve Chairman Ben Bernanke’s term expires in 2010, Obama will name Summers to take his place.”

Source: ABC News, November 22, 2008.

Fox Business: Wilbur Ross on the next Treasury Secretary

Source: Fox Business, November 21, 2008.

Richard Russell (Dow Theory Letters): “Inflate or die, which one will it be?”

“Suddenly, the whole investment world believes in deflation. The TIPS (inflation adjusted government bonds) have collapsed, commodities have crashed, gold goes nowhere, bonds remain near their highs, the dollar remains strong.

“Meanwhile, Bernanke and Paulson are battling the forces of deflation with all the ammunition at their command. I believe Fed chief Bernanke will fight deflation with the last dollar available at the Fed. Paulson will give the US Treasury away before he gives in to deflation and economic contraction.

“How will we know whether Bernanke-Paulson are winning their desperate anti-deflation battle? If they are winning, the dollar and bonds will head down and gold will head higher. If they are losing the battle, the Dow will break below 7,470 and the bear market will continue to eat away at US stocks and the US economy.

“What we are witnessing now is the single greatest economic battle of the century. ‘Inflate or die’, which one will it be?

“Remember, Bernanke’s worst nightmare is dealing with out-of-control deflation. The Fed can halt inflation by pushing up interest rates, but in the case of deflation, the Fed can be helpless. And I ask myself, what happens if Bernanke finds that he is losing the battle against deflation? In that case, we are all survivors. I’ve been there before – during the 1930s. I survived then, and I’ll survive now, and so will my subscribers.

“If Bernanke and Paulson are winning the anti-deflation battle, I believe the first ‘signal’ would be rising gold. So far, it appears to me that gold is undecided. Gold corrected down to the 717 area, then rallied above 800, and now appears to be in the process of testing the 800 level. It would be a plus for gold if December gold can hold above 800. Gold has never been a more important barometer for the future.”

Source: Richard Russell, Dow Theory Letters, November 26, 2008.

Asha Bangalore (Northern Trust): Q3 GDP preliminary estimate

“Real gross domestic product declined at an annual average rate of 0.5% in the third quarter of 2008, slightly weaker than the advance estimate of a 0.3% drop. Going forward, real GDP is expected to show a decline that is upward of 4.0% in the fourth quarter of 2008. The Fed is widely expected to lower the Federal funds rate to 0.50% on December 16, 2008.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary, November 25, 2008.

Barry Ritholtz (The Big Picture): ECRI leading indicators fall to lowest level ever

“One of the questions I seem to be getting all the time is ‘when is this recession going to end?’ To answer that, I turned to Lakshman Achuthan of the Economic Cycle Research Institute (ECRI). Their leading versus coincident chart provides insight into that question.

“The cyclical turns in the leading occur before the coincident – they seem to diverge now and then, and that can be telling. The current story they tell is clearly one of a quickly worsening recession with no end in sight.”

Source: Barry Ritholtz, The Big Picture, November 26, 2008.

Wachovia: US economy in recession mode

“Economic problems began to show up in our model in the fourth quarter of last year as the recession probability rose sharply to 75%, and since then the probability has remained high. While the official recession call will come from the National Bureau of Economic Research sometime next year, for decision-makers the operational guideline is a recession outlook today.”

Source: Wachovia, November 24, 2008.

Asha Bangalore (Northern Trust): Durable goods orders show widespread weakness

“The 6.2% drop in orders of durable goods reflects widespread weakness in bookings of durable factory goods.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary, November 26, 2008.

Breitbart: First-ever decline in online retail spending

“Online retail spending fell four percent in the first weeks of November from the same period last year, the first ever such decline in e-commerce spending, online researcher comScore reported on Tuesday.

“The Reston, Virginia-based company said 8.2 billion dollars was spent online during the first 23 days of November, four percent less than during the same period last year, when 8.5 billion dollars was spent online.

“ComScore forecast that online retail spending for the November-December holiday period will be flat versus year ago, significantly lower than last year’s growth rate of 19 percent.

“‘With consumer confidence low and disposable income tight, the first weeks of November have been very disappointing, with online retail spending declining versus year ago,’ said comScore chairman Gian Fulgoni.”

Source: Breitbart, November 25, 2008.

Asha Bangalore (Northern Trust): Weakness in consumer spending most likely to persist

“Nominal consumer spending fell 1.0% in October, while inflation adjusted consumer spending dropped 0.5%. Inflation adjusted consumer spending has declined for five straight months, the longest string of declines since the 1981-82 recession. Based on October data and conservative assumptions about November and December, consumer spending is most likely to post a 4.0% drop in the fourth quarter after a 3.7% decline in the third quarter.

“The 0.3% increase in personal income during October follows a 0.1% gain in September that was affected by hurricanes. Personal saving as a percent of disposable income was 2.4% in October compared with 1.0% in September. A small upward drift in personal saving is emerging.”

Source: Asha Bangalore, Northern Trust – Daily Global Commentary, November 26, 2008.

Standard & Poor’s: S&P/Case-Shiller – national trend of home price declines continues

“Data through September 2008, released today by Standard & Poor’s for its S&P/Case-Shiller Home Price Indices, shows continued broad based declines in the prices of existing single family homes across the United States, a trend that prevailed since 2007.

“The decline in the S&P/Case-Shiller US National Home Price remained in double digits, posting a record 16.6% decline in the third quarter of 2008 versus the third quarter of 2007. This has increased from the annual declines of 15.1% and 14.0%, reported for the 2nd and 1st quarters of the year, respectively.

“‘The turmoil in the financial markets is placing further downward pressure on a housing market already weakened by its own fundamentals,’ says David Blitzer, Chairman of the Index Committee at Standard & Poor’s.”

Source: Standard & Poor’s, November 25, 2008.

The Wall Street Journal: US agrees to rescue struggling Citigroup

“The federal government agreed Sunday night to rescue Citigroup by helping to absorb potentially hundreds of billions of dollars in losses on toxic assets on its balance sheet and injecting fresh capital into the troubled financial giant.

“The agreement marks a new phase in government efforts to stabilize US banks and securities firms. After injecting nearly $300 billion of capital into financial institutions, federal officials now appear to be willing to help shoulder bad assets, on a targeted basis, from specific institutions.

“Citigroup is one of the world’s best-known banking brands, with more than 200 million customer accounts in 106 countries. Its plunging stock price threatened to spook customers and imperil the bank.

“If the government’s rescue plan is a success, it could help bring stability to the entire financial system. If it doesn’t, even deeper doubts about the industry’s future could spread.

“Under the plan, Citigroup and the government have identified a pool of about $306 billion in troubled assets. Citigroup will absorb the first $29 billion in losses in that portfolio. After that, three government agencies – the Treasury Department, the Federal Reserve and the Federal Deposit Insurance Corp. – will take on any additional losses, though Citigroup could have to share a small portion of additional losses.

“The plan would essentially put the government in the position of insuring a slice of Citigroup’s balance sheet. That means taxpayers will be on the hook if Citigroup’s massive portfolios of mortgage, credit cards, commercial real-estate and big corporate loans continue to sour.

“In exchange for that protection, Citigroup will give the government warrants to buy shares in the company.

“In addition, the Treasury Department also will inject $20 billion of fresh capital into Citigroup. That comes on top of the $25 billion infusion that Citigroup recently received as part of the broader US banking-industry bailout.”

Source: David Enrich, Carrick Mollenkamp, Matthias Rieker, Damian Paletta and Jon Hilsenrath, The Wall Street Journal, November 24, 2008.

Paul Kedrosky (Infectious Greed): Citigroup – bad bank to create bad bank incubator

“I know it isn’t precisely what this headline means – ‘bad bank’ is a euphemism in bailout circles for walling off from one another functional and non-functional parts of banks – but I still like this from the WSJ today.

“To my way of thinking, if we’re interested in creating bad banks, it’s worth knowing that Citi is a veritable ‘bad bank’ incubator.”

Source: Paul Kedrosky, Infectious Greed, November 23, 2008.

CNBC: Mobuis – attraction of Treasurys will wane with lower yields

“Despite continued woes in the US economy, the greenback has seen an unexpected surge against currencies around the world. As investors become ever more risk averse, emerging markets are bearing the brunt of a flight to safety.

“But Mark Mobius, executive chairman of Templeton Asset Management, sees a reversal around the corner.

“‘As everyone is rushing into US Treasurys, they need US dollars to do that and have therefore sold everything in sight,’ Mobius told CNBC. ‘This is why emerging markets have gone down, why commodities have gone down as everyone is moving into dollars.’

“But Mobius said that ‘as US Treasury rates go down to 1% or below you will see the attraction of US Treasurys waning’.

“Mobius also believes that emerging markets have learnt a bitter lesson since the Asian Crisis of 1997-1998. ‘One big lesson was ‘don’t borrow in a currency you are not earning in’,’ he said.

“Emerging markets have also curtailed lending and built up foreign reserves, which they can call upon in almost ‘a reversal of 1997 where the emerging markets were debtors, they are now the creditors’, he added.

“But the surge in the greenback has taken a lot of investors by surprise, Mobius said.

“Having learned from the Asian crisis, companies hedged currencies and ‘ironically these hedges have really worked against them in some cases … as they are over-hedged and it went against them as they were expecting the dollar to go weaker and it went the other way,’ he said.”

Source: CNBC, November 20, 2008.

Bespoke: GSE mortgage spreads tighten

“The Fed’s actions this morning [Tuesday] have certainly helped to thaw the credit markets so far. As shown below, spreads between 10-year Fannie Mae bonds and the 10-year US Treasury tightened significantly today. While they are certainly moving in the right direction, even after today’s record decline, spreads are still higher today than they were just a little more than two weeks ago.”

Source: Bespoke, November 25, 2008.

Bespoke: 30-Year fixed mortgage rates falling back

“Talk of the 30-year fixed mortgage rate falling back below 6% filled the airwaves yesterday [Tuesday], so below we provide a two-year chart of the rate. Even as the Fed funds rate has fallen from 5.5% to 1%, mortgage rates have failed to decline along with it, which hasn’t done much to help the struggling housing market. Economists and investors are hoping that the Fed’s actions yesterday will start pushing mortgage rates lower. This will help ease the credit crisis as banks will become more willing to lend, providing better interest rates for potential homebuyers. 5.81% is better than the 6.4% seen at the start of the month, but the rate could still stand to drop quite a bit.”

Source: Bespoke, November 26, 2008.

Frank Holmes (US Global Investors): Stock market reversal is near

“According to research from Thomas Weisel, the S&P 500 has been a ‘Buy’ since that index closed at 800 last Friday, based on its probability models. They say a verification could come in early December, when monthly liquidity figures come out – if there is extreme positive liquidity to accompany the technical ‘Buy’ signal, history shows that on average there’s a six-month price rally of 18.5%.

“Our oscillator tells us that, statistically speaking, the S&P 500 is extremely oversold and thus due for a reversal toward the mean. The chart above shows that the S&P 500 is now down about four standard deviations over 60 trading days, which is a far more dramatic decline than we saw in 1998, when Russia endured a currency crisis and the collapse of the hedge fund Long-Term Capital Management threatened the global financial sector, and in 2001 after the September 11 terror attacks.

“The possible turnaround that we are seeing is not wishful thinking, but it’s not a sure thing, either. Our confidence grows with every positive data point indicating that a reversal is near, and we will continue watching for these indicators …”

Source: Frank Holmes, US Global Investors – Weekly Investor Alert, November 28, 2008.

Eoin Treacy (Fullermoney): Start thinking about stocks to buy

“Angst, fear and anxiety are all related emotions which come to the fore when we feel under pressure and begin to doubt our abilities as investors. However, when we see a market fall such as that of the last few months, we have to rein in the temptation to succumb to such emotions. It will prove more profitable over the medium to longer-term, to turn objective about the opportunities we are being presented with sooner rather than later.

“This does not mean one piles into the market with every spare unit of currency right now, but it is a time to begin to think about the shares one wants to own in a recovery environment. From a value perspective there are a number of instruments which have been hit particularly hard and somewhat unjustifiably by the credit / solvency crisis.

“We now need to begin to think more about recovery potential rather than further potential losses. Stocks and corporate bonds are no longer expensive, some are downright cheap. We have not reached the deep value levels seen in the past, but these need not necessarily appear at the numerical low for the market, if they appear at all. However, one looks at the market, given the extent of the fall, this is not a time to become increasingly bearish, but is one in which to make provisions and possible purchases for a recovery scenario.”

Source: Eoin Treacy, Fullermoney, November 27, 2008.

David Fuller (Fullermoney): Watch developments in US rather than invest there

“I believe that America’s problems of debt and deficits are worse than for many other countries. More importantly, I will be guided by price charts, which reflect the collective decisions and views of everyone else. In terms of investment appropriateness, my current view is that I would rather watch developments in the US than invest there.

“The credit / solvency crisis is clearly America’s biggest problem at this time. This is not necessarily true for all other countries, although all are obviously affected to a greater or lesser degree by developments in the USA. I suggest that the West’s credit / solvency crisis was only the second biggest problem for Asia’s developing economies.

“Asia’s biggest recent problem, I maintain, was inflation, not least from previously soaring energy and food prices. That crisis, which in comparison was the USA’s second biggest problem, has largely disappeared today. I suspect commodity inflation will not re-emerge for at least the next year or two, subject to supply, global GDP and the USD.

“Consequently, I believe that developing Asia would be in an excellent position for recovery, were it not for the West’s ongoing credit / solvency crisis. Therefore, the worse the USA’s problems become, the more this will be a drag on Asia’s own recovery. Conversely, if the USA somehow avoids a destructive deflation, Asia should still bounce back more quickly.

“I will invest accordingly.”

Source: David Fuller, Fullermoney, November 26, 2008.

Jeffrey Saut (Raymond James): Geithner gotcha

“We still think October 10 represented the capitulation ‘lows’. As Barron’s notes, ‘For a bullish spin, though a weak one, the market has not made a significantly lower low since October 10. The word ‘significantly’ is important because some major market indexes, including the Nasdaq, have indeed been setting new lows. But the trend, if we can call it that, has been more sideways than decidedly down.

“A better, but still weak, bullish angle comes from trading volume, or the amount of money committed to either the bull or bear side each day. All of the higher volume days that have occurred since October 10 have come on days when prices rose. Theoretically, when prices are going up and volume increases, it means that investors are chasing the market higher. That’s a sure sign of demand. Subsequent declines occurred with lower volume, so we can conclude that the desire to sell was not quite as strong as it was before October 10.”

Source: Jeffrey Saut, Raymond James, November 24, 2008.

Bespoke: Analysts at their least bullish levels ever

“While Wall Street analysts are typically known for being overly optimistic, based on at least one measure, they have never been less bullish. According to Bloomberg statistics that track analyst buy, sell, and hold ratings, only 36% of all ratings are currently buys. As the chart below shows, this is the lowest level since at least 1997, and significantly lower than the 75% level we saw in 1997 and 2000. However, since the Spitzer crackdown on Wall Street research and the bursting of the tech bubble, analysts have grown increasingly shy about putting a buy rating on a stock they cover.”

Source: Bespoke, November 25, 2008.

Bespoke: Q3 and Q4 sector earnings growth

“With about 96% of S&P 500 companies having reported third quarter earnings, current EPS growth numbers for the quarter should be very close to what the final tally will read. As shown below, four sectors have had negative year over year growth in the third quarter, while six have had positive growth. Financials and consumer discretionary were once again the sectors that brought down the index as a whole. Financials have seen earnings decline by 129.7% in Q3 ’08 versus Q3 ’07. Consumer discretionary has seen earnings decline by 41.4%. Telecom and utilities are the two other sectors with negative Q3 earnings growth, and the S&P 500 as a whole currently stands at -18.4%. The energy sector has had by far the largest earnings growth at 57.4% versus the third quarter of 2007. Consumer staples ranks second behind energy at 10.9%, followed by health care, materials, technology, and industrials.

“So what does the fourth quarter look like? Analysts are expecting the S&P 500 to actually show positive year over year earnings growth in the fourth quarter of 4%. This is because the financial sector is expected to show growth of 64.2% due to the fact that Q4 ’07 was so bad. Utilities, health care, and consumer staples are the other three sectors expected to see earnings growth, while consumer discretionary, materials, energy, telecom, technology and industrials are expected to see earnings declines.”

Source: Bespoke, November 23, 2008.

Naked Capitalism: Cheery chart – no corporate profits for two years during depression

“In case you are starting to look to past crises for clues as to how our financial mess might play out, here is a Great Depression factoid (from Levy Forecast, November 2008):

“Note that the report itself argues that the US will have a ‘contained’ depression, with deep recession conditions for a protracted period and an anemic recovery. It does not believe the zero operating profits pattern of the Great Depression will be repeated.”

Source: Naked Capitalism, November 23, 2008.

Bloomberg: Hambro sees “great entry points” for commodity stocks

“Evy Hambro, who manages the world’s largest mining and gold funds at BlackRock, talks with Bloomberg about the outlook for commodities and mining stocks.”

Source: Bloomberg, November 21, 2008.

Bloomberg: Marc Faber says gold is most precious asset

Source: Bloomberg, November 25, 2008.

Ambrose Evans-Pritchard (Telegraph): Citigroup says gold could rise above $2,000 next year

“The bank said the damage caused by the financial excesses of the last quarter century was forcing the world’s authorities to take steps that had never been tried before.

“This gamble was likely to end in one of two extreme ways: with either a resurgence of inflation; or a downward spiral into depression, civil disorder, and possibly wars. Both outcomes will cause a rush for gold.

“‘They are throwing the kitchen sink at this,’ said Tom Fitzpatrick, the bank’s chief technical strategist.

“‘The world is not going back to normal after the magnitude of what they have done. When the dust settles this will either work, and the money they have pushed into the system will feed though into an inflation shock.

“‘Or it will not work because too much damage has already been done, and we will see continued financial deterioration, causing further economic deterioration, with the risk of a feedback loop. We don’t think this is the more likely outcome, but as each week and month passes, there is a growing danger of vicious circle as confidence erodes,” he said.

“‘This will lead to political instability. We are already seeing countries on the periphery of Europe under severe stress. Some leaders are now at record levels of unpopularity. There is a risk of domestic unrest, starting with strikes because people are feeling disenfranchised.”

“Gold traders are playing close attention to reports from Beijing that the China is thinking of boosting its gold reserves from 600 tonnes to nearer 4,000 tonnes to diversify away from paper currencies. ‘If true, this is a very material change,’ he said.

“Citigroup said the blast-off was likely to occur within two years, and possibly as soon as 2009. Gold was trading yesterday at $812 an ounce. It is well off its all-time peak of $1,030 in February but has held up much better than other commodities over the last few months – reverting to is historical role as a safe-haven store of value and a de facto currency.”

Source: Ambrose Evans-Pritchard, Telegraph, November 27, 2008.

James Turk (GoldMoney): Scenario for gold is bullish

“Gold soared $50 this past Friday. It began the day at $748 and was trading at $800 when the day ended.

“It is rare for gold to achieve such a huge one-day gain. In fact, I checked my records for the past twenty years and found only one other instance when gold climbed $50 or more in a day. Interestingly, the other occurrence was on September 17, 2008, barely two months ago. That rally also took gold back above $800.

“That these two rallies – unique and rare in their magnitude – occurred so near to one another is significant. Is there a message from these two events? Yes, indeed!

“Gold itself is telling us two things. First, there is an enormous short position in gold. Huge rallies occur for a reason, and short covering is always a factor. In order to limit their losses, shorts will bid up the market in a desperate attempt to cover their position. The rule of thumb is straightforward – the bigger the short position, then the bigger the rally.

“Second, and more importantly, these huge rallies are signaling that gold under $800 is too cheap. A higher price is needed to bring supply and demand back into balance.

“There is other, more than ample evidence to support this same conclusion. The demand for physical metal remains strong.

“Friday’s trading action adds to the growing body of evidence that the correction in gold that began after making a new record high in March above $1,020 is ending. The low in gold in all likelihood is probably in place. The $700 level has been tested and re-tested, and the huge rallies launched from prices below $800 mean that other attempts to take gold into the $700s will be met with good demand.

“Gold remains in a bull market, and so does silver. National currencies are in a bear market. Get ready for the next leg in the precious metal’s ongoing bull market.”

Source: James Turk, GoldMoney, November 24, 2008.

The Australian: Perth Mint suspends orders amid rush to buy bullion

“Fears of the unknown long-term effects from the global financial crisis have sparked a new gold rush.

“With retail and wholesale clients around the world stocking up on the precious metal, the Perth Mint has been forced to suspend orders.

“As the World Gold Council reported that the dollar demand for gold reached a quarterly record of $US32 billion in the third quarter, industry insiders said the race to secure physical gold had reached an intensity that had never been witnessed before.

“Perth Mint sales and marketing director Ron Currie said the unprecedented demand had forced the Mint to cease orders until January, with staff working seven days a week, 24-hour days, over three shifts to meet orders.

“He said Europe was leading the demand, with Russia, Ukraine, Middle East and US all buying – making up 80% of its sales.

“‘We have never seen this before and are working right at capacity. And we are seeing it from clients in the shop buying one ounce, right up to 30,000 ounces from overseas clients,’ Mr Currie said.”

Source: Sarah-Jane Tasker, The Australian, November 22, 2008.

Mike Wittner (Société Générale): Oil prices susceptible to further deleveraging

“Unless oil prices melt down again this week, Opec will not cut production at this weekend’s informal meeting in Cairo and instead will wait until the cartel’s gathering in December to reduce output quotas by 1 million to 1.5 million barrels a day, says Mike Wittner, global head of oil research at Société Générale.

“Mr Wittner says that Opec simply does not have enough information on the effectiveness of the production cuts that it has already made, or sufficient feedback from its customers, to proceed with further reductions in output. ‘We see (a decision to maintain current production quotas) as a 60-40 probability and the outcome of the meeting could easily be affected by price action this week,’ says Mr Wittner, who notes that signals from Opec have been mixed so far.

“Mr Wittner says tanker tracking data suggest there has been a ‘very significant cut’ in Opec’s oil production in November, down 1.2 million barrels a day compared with October.

“But SocGen says fundamentals will be perceived to be weak until the market becomes convinced Opec has cut supplies, given that a tanker requires six weeks to travel from the Persian Gulf to the US. Only then will November’s cuts appear in lower crude imports and stocks, which is what the market wants to see.

“‘Oil prices will remain susceptible to further deleveraging (by hedge funds) and caution remains the order of the day,’ concludes Mr Wittner.”

Source: Mike Wittner, Société Générale (via Financial Times), November 25, 2008.

Financial Times: EU’s stimulus plan met with doubts

“The European Union’s proposal on Wednesday for a €200 billion economic stimulus plan for the bloc was met by immediate doubts on whether member states would back the measures aimed at avoiding a deeper recession.

“The proposal envisages that about €170 billion would be contributed by the bloc’s 27 member states through tax and infrastructure plans. The European Commission and the European Investment Bank would provide the remaining €30 billion, partly through the accelerated pay-out of selected spending programmes.

“The package, which is larger than expected, represents about 1.5% of the EU’s gross domestic product. It needs to be reviewed by EU finance ministers next week and by government leaders in mid-December.

“Economists and politicians quickly questioned whether all member states would step up as required or whether individual governments’ responses would diverge from the Commission’s suggested measures.

“Analysts at Capital Economics, the consultants, said: ‘The proposed boost has yet to be agreed by member states and would sadly not do enough to bring European economies out of the gloom for some time anyway.’

“Business Europe, the main business lobby group in Brussels, agreed with the proposals but said a ‘clear commitment from EU member states’ was needed to implement stimulus packages of at least 1.2% of GDP.”

Source: Nikki Tait, Financial Times, November 26, 2008.

BBC News: Boost for Spanish and Italian economies

“Spain and Italy have announced plans worth billions of euros to kick-start their economies.

“Italy approved an 80 billion euro emergency package that included tax breaks for poorer families, public works projects and mortgage relief.

“Spain unveiled an 11 billion euro plan aimed at creating 300,000 jobs.

“The announcements are the latest in a series of attempts by EU governments to shore up their economies as the financial crisis bites.

“Italian Prime Minister Silvio Berlusconi called on to Italians to keep on spending. ‘We have helped citizens, the less well off, so that they can continue to consume,’ he said. ‘The intensity and duration of the crisis depends on all of us.’

“Spain’s Prime Minister, Jose Luis Rodriguez Zapatero, said the money will be mainly invested in infrastructure and public works.

“Spain’s unemployment reached 12.8% in October – the highest in the eurozone.”

Source: BBC News, November 28, 2008.

BBC News: German business confidence dives

“Business confidence in Germany fell in November to the lowest level since 1993, according to the key Ifo economic climate index. The index, based on a poll of 7,000 companies, has dropped for six consecutive months, the Munich-based Ifo institute said.

“The index stands now at 85.8, down 4.4 points from October.

“‘The downturn has worsened and will now have an impact on the labour market,’ Ifo said in a statement.

“Germany’s exports have been hard hit by falling demand worldwide, with some auto makers seeking state help to maintain production.

“On Friday another key indicator, the Markit purchasing managers’ index, revealed that business activity in the 15 countries sharing the euro had fallen in November to a ten-year low.”

Sources: BBC News, November 24, 2008 and Victoria Marklew, Northern Trust – Daily Global Commentary, November 24, 2008.

Financial Times: Eurozone set for rate cut of at least 50bp

“Eurozone official interest rates are almost certain to be slashed again next week by at least half a percentage point after a survey on Thursday showed the region facing its worst downturn since the recession of the early 1990s.

“Economic confidence in the 15-country region crashed this month to its lowest point since August 1993, the European Commission reported. With inflation also falling rapidly, the European Central Bank has not sought to stop financial markets assuming its main interest rate will be cut next Thursday from 3.25% to 2.75% or below.

“Public ECB comments show the bank remains cautious about the pace of cuts, pointing to a half-point reduction next week – the same as in October and this month. But economic news has been consistently gloomier than expected, strengthening the case for a larger cut.”

Source: Ralph Atkins, Financial Times, November 27, 2008.

Financial Times: UK tax hit to fund £20 billion fiscal stimulus

“Taxpayers face six years of austerity, paying for the consequences of recession and a £20 billion fiscal stimulus unveiled on Monday by Alistair Darling as he detailed the most dismal Budget outlook seen since 1993.

“National insurance contributions for both employees and employers will rise by 0.5%. Those earning more than £100,000 will pay more income tax – with those on £150,000 facing a new higher tax rate of 45% – and public spending faces its biggest squeeze for 15 years – although all these measures will not kick in until 2011, well after the next election. The tax clawback would leave someone earning £150,000 paying an extra £3,040 in tax.

“Mr Darling detailed the planned tax rises and spending restraint as he sought to show the City and foreign investors that Britain had a clear plan to restore prudence to the public finances after truly shocking forecasts for public borrowing in the next two years.

“Public borrowing will hit a record level of £118 billion in 2009-10 and will fall to a level the government considers prudent only in 2015-16, far later than City forecasts had expected.

“Government debt will blast through the current 40% of national income limit, racing to 57% in 2012-13, when it will top the £1,000 billion mark for the first time.

“Britain’s output will continue to fall until the second half of next year, the chancellor added, as he presented a gloomy forecast with the recession mitigated only in part by the fiscal boost delivered predominantly through a 2.5 percentage point cut in value added tax from next week and lasting until the end of 2009.

“Over the next year, the cut in the VAT rate to 15% will be augmented by £2.5 billion of additional capital expenditure projects brought forward from 2010-11, a £60 payment to every pensioner, an earlier increase in child benefit and a deferral in the planned increases in vehicle excise duties.

“Mr Darling also used the crisis to stage a series of tactical retreats from earlier decisions, announcing a rethink of his plans to reform air passenger taxes and an exemption from tax for the dividends of UK companies’ foreign subsidiaries.

“Together the Treasury assumes the £20 billion package – about 1% of national income for a little over a year – will prevent the economy sinking by a further 0.5%, although Mr Darling’s forecast was for a contraction of 0.75% to 1.25% in 2009.”

Source: Chris Giles and George Parker, Financial Times, November 24, 2008.

James Pressler (Northern Trust): China – getting serious about the slowing economy

“The People’s Bank of China (PBoC) slashed its benchmark one-year loan and deposit rates by 108 basis points apiece today [Wednesday], reducing them to 5.58% and 2.52%, respectively. This dramatic move comes well after the industrialized economies coordinated a major monetary easing – most central banks have already turned their attention toward liquidity concerns and an eventual global recession. Only three months ago, Beijing had a proactive mindset, thinking about economic stimulus to compensate for the post-Games lull and a general slowdown in global production. The first question that comes to our mind is why does the government suddenly seem to be lagging in its response?

“One fact worth noting is that the immediate economic impact on the Chinese economy has not been as clear-cut as in the industrialized countries. The Olympic Games threw in plenty of distractions and had widespread effects on economic indicators. Retail sales were positively impacted from the many tourists flooding into the country, but conversely, industrial production fell off as many factories closed in response to temporary anti-pollution measures. The conclusion of numerous infrastructure projects shifted flows of goods and inputs, and plenty of other one-off factors added a lot of noise to China’s economic statistics. Only after the Games passed and some of those factors fell from the calculations did a clearer picture emerge, and the trends are not promising. Industrial production continues to fall, and monthly export growth is showing signs of weakness.

“To be fair, the PBoC issued minor rate cuts over the past three months, and the government did offer a supplementary fiscal stimulus package. Today’s more dramatic move suggests that PBoC officials are now firmly convinced that China will be joining the rest of the world in a significant economic slowdown. Some forecasts recently suggested that after GDP growth of nearly 12% in 2007, the economy could slow to below 10% this year and perhaps 7.5% in 2009. While the growth rate itself is still enviable, officials in Beijing realize all too well that a deceleration of over four percentage points will not go unnoticed, and they will likely be taking more action before the year is up.”

Source: James Pressler, Northern Trust – Daily Global Commentary, November 26, 2008.

Bloomberg: China reserves to pass $2 trillion; Russia’s fall

“China’s foreign-exchange reserves may top $2 trillion for the first time by the end of this year, giving the world’s most-populous nation more firepower to stimulate its economy during a global recession.

“China’s holdings increased 25% in the first nine months of the year to stand at $1.906 trillion on September 30. Reserves shrank in Japan and Russia, the nations with the second- and third-largest stockpiles. Russia drained a quarter of its currency and gold assets in less than four months to prop up the ruble, which has dropped 14% since June 30.”

Source: Lee J. Miller and Zhang Dingmin, Bloomberg, November 28, 2008.

Breitbart: Analysts – India economy will be OK despite attacks

“The terror attacks that rocked India’s financial capital may depress stocks, dampen tourism and slow new investment, but are unlikely to inflict long-term damage on the nation’s economy, analysts and business people said Thursday.

“‘This is a challenge for the government to maintain law and order in the country,’ said Takahira Ogawa, director of sovereign ratings at Standard & Poor’s in Singapore. ‘At this stage, I don’t think there will be any major impact on the macroeconomic or fiscal position of the government.’

“The attacks, which began Wednesday night when gunmen invaded two posh hotels, a restaurant and several other sites in downtown Mumbai, came as India was struggling to contain fallout from the global financial crisis.

“Foreign investors have already pulled $13.5 billion out of the nation’s stock market this year, driving the benchmark Sensex index down 57% and punishing the rupee. Liquidity has dried up, economic growth is slowing and people are spending less money.

“The attacks are ‘a challenge to the economic resurgence in India’, said Habil Khorakiwala, chairman of Wockhardt, an Indian pharmaceutical company.

“‘The targets identified clearly demonstrate that the intention is to create panic and shatter the confidence in the minds of investors in India and global investors coming to India,’ he said in a statement. ‘This war has to be fought together by all across, to protect the safety of Indian people, for economic resurgence and growth of the Indian nation.'”

Source: Breitbart, November 27, 2008.

BBC News: Saudi Arabia cuts interest rate

“Saudi Arabia has cut a key interest rate and taken steps to encourage lending as it faces the slowdown. The central bank reduced the repo interest rate from 4% to 3%, in an attempt to boost liquidity. It also reduced the cash reserve requirements for banks, seen as a way to improve the availability of credit.

“The move came a day after the benchmark Tadawul All Share Index fell to its lowest level in five years, hit by the global slowdown and falling oil prices. The index shed 9.2% on Saturday, the start of its trading week. Since the start of the year the index is down more than 60%.

“The Gulf region has been hard hit by a huge fall in oil prices, a key export. Oil prices are around two thirds lower than they were in July when they hit a record above $147 a barrel.”

Source: BBC News, November 23, 2008.

What's been said:

Discussions found on the web: