Further to Barry’s post about bank ROE taking a dive, below is a comment we published earlier this week on the economic reality in the banking industry vs. the simulated, subsidized situation of the largest banks — really the top four players which control about a third of the entire banking industry’s assets. The chart below shows the IRA Bank Stress Index as of Q1 with the large banks included at 2.36 (1995=1), which is huge. But if you take the top four lead banks out, the Stress Index score was over 5.5. See the graphic below:

Source: FDIC, The IRA Bank Monitor

What is really significant about Barry’s post, however, is some work we did for one of the Big Four accounting firms, when we calculated the risk-adjusted return on capital or RAROC for the large bank peer group going back 25 years (yeah, we’ve got almost three decades of clean, as-filed data from the FDIC that is aligned properly to do complex analytics). The results show that RAROC for the big banks was actually in single digits in 2007, before the current “correction” occurred. Now the banks are destroying value with both hands, showing that what goes up too far must retrace. That is why we remain extremely bearish about the depth of the trough facing the industry — my pal from Bear Stearns, Joannie McCullough calls it the “mine shaft” — and are predicting over 1000 banks on the current dead pool list. Enjoy the Big Picture conference tomorrow. — Chris

Q1 2009 Bank Ratings Update and GM, GMAC Bank Join the Zombie Dance Party

The Institutional Risk Analyst

June 1, 2009

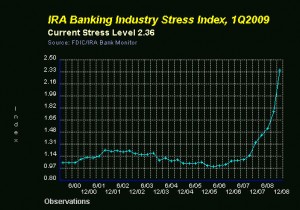

We loaded the final Q1 2009 data from the FDIC into The IRA Bank Monitor on Friday and the results are rather striking. As you will recall, our preliminary Stress Index score for the banking industry was over 5.7 or half an order of magnitude above the 1995 benchmark year. This result excluded the ratings for the lead units of the largest money center banks, data for which was not released until last week.

With the large bank data added to the rest of the industry, however, the Stress Index score fell to “only” 2.36, which still is a 33% increase from the 1.8 at year-end 2008. The final Q1 Stress Index score is higher than any time in the past 25 years. More, the difference between the preliminary results (5.8) and the final Stress Index score (2.36) for Q1 2009 illustrates the degree of subsidy provided to the large banks by the Fed, Treasury, etc. Thus the true economic situation in the broad industry is illustrated by the preliminary result, while the final score for the entire industry inclusive of the largest banks is illustrated by the blended Stress Index result.

At the current rate of deterioration, that could put the Stress Score for the entire industry over 10 by Q4 2009 or a full order of magnitude above the 1995 baseline. Such a worst case scenario suggests that we could see one in four US banks merged or resolved through the cycle. In the event, that suggests that over 2,000 institutions, large and small, will be resolved. Put that into context with the FDIC’s “official” dead pool of 300 or so institutions and that gives you a tangible measure for how much “spin” might live within the official version of the problems facing the US banking industry. We’ll expand further on the possible scenarios for the US banking industry in our PickingNits blog.

As we told subscribers to the IRA Advisory Service last week, in Q1 2009 Citigroup (NYSE:C) and other large banks evidenced improvements in ROE, Efficiency and Exposure thanks to the generous subsidies being provided by the US government from several sources:

1) Government subsidized TARP capital injections,

2) Below-market loans via repurchase transactions with the Federal Reserve Banks,

3) Below-market funding via FDIC guarantees on debt, and

4) Subsidies for Bear, Stearns, AIG and other credit default swap (“CDS”) counterparties of the large banks.

Subscribers to the consumer or professional versions of the IRA Bank Monitor may view the Q1 2009 profiles for all US banks. We’ll be talking more about zombie banks later this week in an interview with Professor Ed Kane of Boston College. As we discussed with Dr. Kane and also with our friend Josh Rosner last week, without the bailouts of Bear, AIG and the work-around of many other CDS counterparties, the capital of JPMorganChase (NYSE:JPM) would have evaporated several times over as CDS contracts were triggered.

What's been said:

Discussions found on the web: