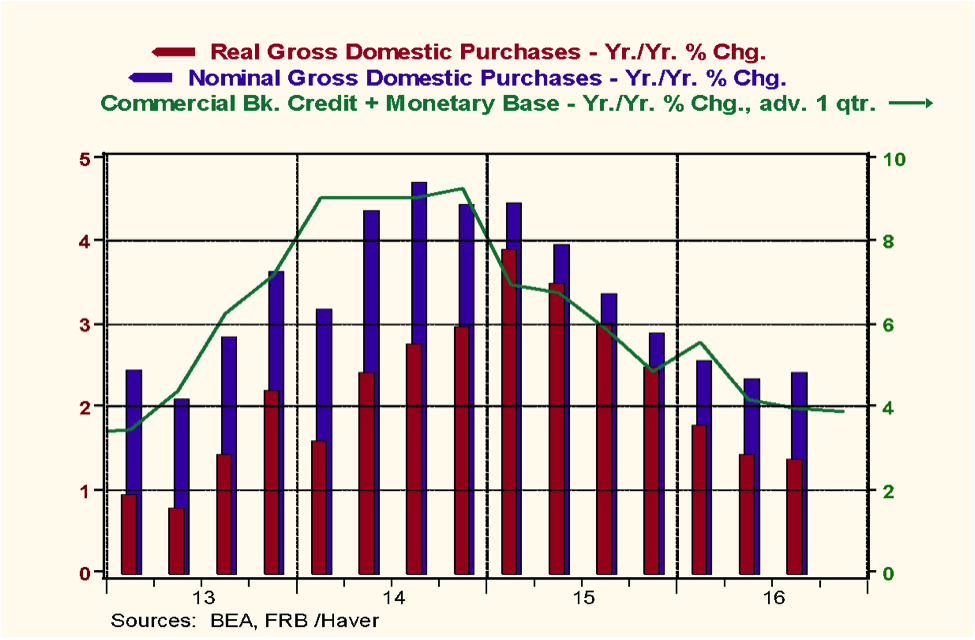

As shown in Chart 1, the year-over-year growth in real and nominal Gross Domestic Purchases (C+I+G) in Q3:2016 was 1.4% and 2.4%, respectively. This compares with 2.8% and 4.7% year-over-year growth in real and nominal Gross Domestic Purchases, respectively, in Q3:2014. So the pace of real and nominal domestic spending in the four quarters ended Q3:2016 was about half that of the pace in the four quarters ended Q3:2014.

Notice the green line in Chart 1. It represents the year-over-year percent change in quarterly-average observations of the sum of commercial bank credit (loans and securities on the books of commercial banks) and the monetary base (reserves held at the Fed by depository institutions and currency in circulation). As regular readers (are there still two of you?) of this commentary remember, this sum is what I refer to as thin-air credit because it is credit that is created by the commercial banking system and the Fed figuratively out of thin air. The unique characteristic of thin-air credit is that no one else need cut back on his/her current spending as the recipient of this credit increases his/her current spending. Notice that growth in this measure of thin-air credit, as represented by the green line in Chart 1, has been trending lower since hitting a post-recession peak in the fourth quarter of 2014. Growth in thin-air credit is advanced by one quarter in Chart 1 because my past research has shown that the highest correlation between growth in thin-air credit and growth in nominal Gross Domestic Purchases is obtained when growth in thin-air credit leads growth in nominal Gross Domestic Purchases by one quarter. This suggests, but by no means proves, that the behavior of thin-air credit has a causal relationship with the behavior of growth in Gross Domestic Purchases. So, I believe that the slowdown in the growth of thin-air credit in the past two years has played a major role in the slowdown in domestic spending during this period.

Chart 1

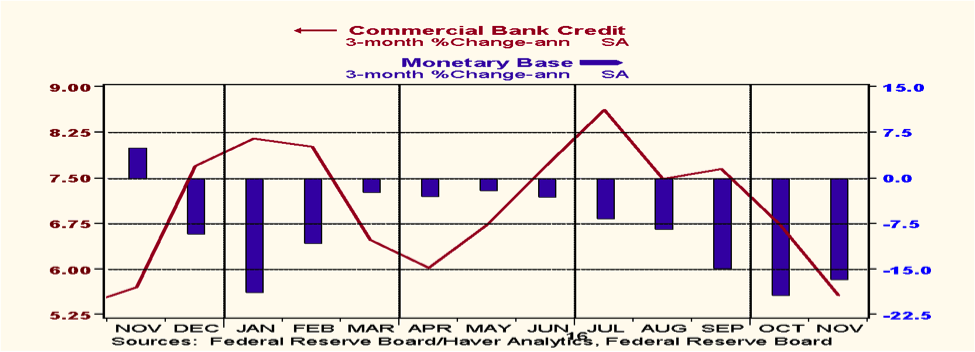

Chart 2 provides some insight as to why growth in the sum of commercial bank credit and the monetary base has been slowing since 2014. The slowdown in the growth of thin-air credit in the past two years is not because banks have been stingy with their granting of credit. On the contrary, as can be seen in Chart 2, year-over-year growth in commercial bank credit (the blue line), after accelerating sharply in 2014, held in a range of about 6-1/2% to 7-3/4% in 2015 and over the first three quarters of 2016. So, despite the increased regulation that banks are now subject to, bank credit growth has returned to a rate approximately equal to its long-run median. No, the culprit has been the Fed. Growth in the monetary base (the green bars in Chart 2), reserves and currency created by the Fed, decelerated in 2014. There was essentially no growth in the monetary base in 2015 and there has been a contraction in it so far in 2016. In 2014, the Fed began to taper the amount of securities it had been purchasing in the open market in connection with its third phase of quantitative easing (QE). This resulted in the deceleration in the growth of the monetary base. In 2015, the Fed ceased its QE operations. In December 2015, the Fed raised its federal funds rate target by 25 basis points.

In order to “enforce” this higher federal funds rate, the Fed had to reduce the supply of reserves it created relative to depository institutions’ demand. This resulted in the contraction in the monetary base in early 2016. For reasons still a mystery to me, the Fed has failed to offset the drain of reserves caused by unusually high Treasury balances at the Fed. In addition, the Fed has been draining reserves from the financial system via reverse repurchase agreements, presumably to satisfy the money market mutual funds’ demand for risk-free assets as a result of regulatory changes that when in effect in October 2016. (See my November 1, 2016 commentary “The Fed Began Tightening Policy in October and No One Knew It, Maybe Not Even the Fed” for a discussion of this.) This has resulted in the continued contraction in the monetary base in 2016.

In sum, the slowdown in the growth of combined commercial bank credit and the monetary base in the past two years is primarily the result of the Fed’s failure to create enough thin-air credit to prevent the stagnation in monetary base in 2015 and the outright contraction in the monetary base so far in 2016. And I would submit to you that the significant deceleration in the growth in combined commercial bank credit and the monetary base in 2015 and 2016 is primarily responsible for the deceleration in the growth of both nominal and real Gross Domestic Purchases in these years as well.

Chart 2

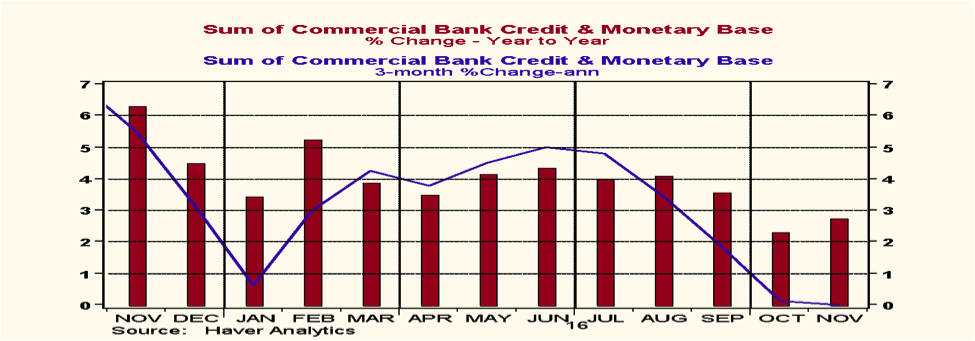

On December 14, 2016, the Fed raised its federal funds rate target by another 25 basis points. Just as the Fed had to reduce the supply of reserves relative to depository institutions’ demand for them in order to push the federal funds rate up to its higher targeted level in December 2015, it will have to do the same thing in December 2016. This implies a further contraction in the monetary base. Chart 3 shows the year-over-year annual and three-month annualized growth in combined commercial bank credit and the monetary base in the past 12 months.

In the 12 months ended November 2016, growth in combined commercial bank credit and the monetary base was 2.7%. In the three months ended November 2016, growth in combined commercial bank credit and the monetary base was a goose egg – that is, zero. To put the recent growth in this measure of thin-air credit into perspective, from January 1960 through November 2016, the median year-over-year growth in monthly observations of combined commercial bank credit and the monetary base has been 7.1%. So, recent months’ growth in this measure of thin-air credit has been exceptionally low, both in absolute as well as relative terms. And, with the Fed’s December 14, 2016 decision to raise the federal funds rate another 25 basis points, growth in combined commercial bank credit and the monetary base will be even weaker in the coming months.

Chart 3

The extreme weakness in the growth in the past three months of combined commercial bank credit and the monetary is not just due to the contraction in the monetary base. As shown in Chart 4, there also has been some weakening in the growth of commercial bank credit, too. To wit, in the three months ended November 2016, the annualized growth in commercial bank credit slowed to 5.6%, the slowest growth since the 5.7% posted in the three months ended November 2015.

Chart 4

Based on published data so far for Q4:2016, the Atlanta Fed is forecasting real GDP annualized growth in this current quarter of 2.4%, down from the previous quarter’s 3.2% annualized growth. With current growth in thin-air credit already very weak and likely to get even weaker after the Fed contracts the monetary base more in order to push the federal funds rate 25 basis points higher, real and nominal U.S. economic growth is likely to slow further in the first half of 2017.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client. References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers Please see disclosures here: https://ritholtzwealth.com/blog-disclosures/

What's been said:

Discussions found on the web: