It happened at least once a year, every year. In a roomful of a dozen Harvard University financial officials, Jack Meyer, the hugely successful head of Harvard’s endowment, and Lawrence Summers, then the school’s president, would face off in a heated debate. The topic: cash and how the university was managing – or mismanaging – its basic operating funds.

“Mohamed was having a heart attack,’’ said one former financial executive, who spoke on the condition of anonymity for fear of angering Harvard and Summers. He considered the cash investment a “doubling up’’ of the university’s investment risk.

But the warnings fell on deaf ears, under Summers’s regime and beyond. And when the market crashed in the fall of 2008, Harvard would pay dearly, as $1.8 billion in cash simply vanished. Indeed, it is still paying, in the form of tighter budgets, deferred expansion plans, and big interest payments on bonds issued to cover the losses.

So how did one of the world’s great universities err so badly in something so basic? It is a story with many actors, the story of an institution that grew complacent as its endowment soared ever higher – an institution that, when the crunch hit, was operating on financial auto-pilot, with many key players gone, and those remaining inattentive, in retrospect, to the risks ahead.

So how did one of the world’s great universities err so badly in something so basic? It is a story with many actors, the story of an institution that grew complacent as its endowment soared ever higher – an institution that, when the crunch hit, was operating on financial auto-pilot, with many key players gone, and those remaining inattentive, in retrospect, to the risks ahead.

“Investing cash alongside the endowment was a long-held strategy that we didn’t decide to change until early 2008,’’ said James F. Rothenberg, Harvard’s treasurer – a part-time, unpaid role. He said the biggest mistake was not to have taken some of the cash off the table, and placed it in safer accounts, as trouble started brewing in the markets and the economy. “We all can look back now and say we wish we did something different,’’ he said.

In the Summers years, from 2001 to 2006, nothing was on auto-pilot. He was the unquestioned commander, a dominating personality with the talent to move a balkanized institution like Harvard, but also a man unafflicted, former colleagues say, with self-doubt in matters of finance.

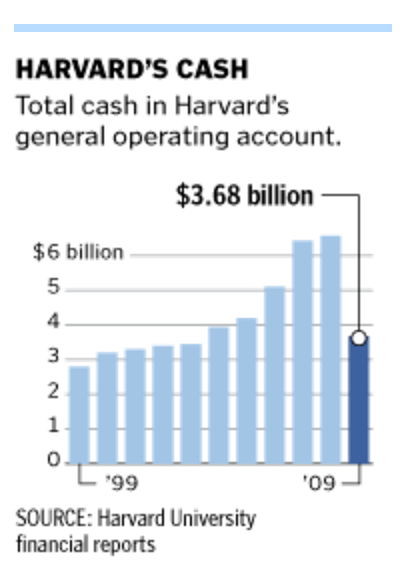

Certainly, when it came to handling Harvard’s cash account, the former US Treasury secretary had no doubts. Widely considered one of the most brilliant economists of his generation, Summers pushed to invest 100 percent of Harvard’s cash with the endowment and had to be argued down to 80 percent, financial executives say. The cash account grew to $5.1 billion during his tenure, more than the entire endowment of all but a dozen or so colleges and universities.

Summers, now head of President Obama’s economic team, declined to be quoted on his handling of Harvard finances. A friend of his who is familiar with Harvard finances said Summers was warning of growing risks in the global markets by 2007, at the World Economic Forum in Davos, Switzerland. The friend, who spoke on the condition of anonymity because of Summers’s current position, said, “In the years after Summers left, market conditions and Harvard’s liquidity changed dramatically. The university’s financial strategies could have and should have changed with them.’’

Investing cash from the general operating account in the endowment wasn’t new under Summers, nor was it unique to Harvard. It had been done as far back as the 1980s at the university, officials say, but on a smaller scale. The aggressive investment of cash accounts is part of how the university has long run its “central bank,’’ an account that holds funds from its various schools and pays them a modest US Treasury rate of return. The “bank,’’ in turn, has invested the lion’s share of that money with the endowment, generating returns that are used to pay for shared needs, like graduate housing and financial aid.

The strategy paid off handsomely for years, as the endowment reaped big gains, providing Harvard presidents with a checkbook for ambitious efforts. Under Neil Rudenstine, Harvard’s president from 1991 to 2001, cash was heavily invested in the endowment and surged from $290 million to $2 billion. Under Summers, the figure more than doubled again, according to a compilation of the data obtained by the Globe. The big project on Summers’s agenda: Harvard’s expansion across the river, into Allston.

Summers had a huge influence over Harvard money matters during his tenure, according to several people who worked with him. Known for his love of intellectual debate, he would hear out the opinions of others but ultimately was forceful in his own views. He was more financially sophisticated than most other Harvard presidents, and more deeply involved in decisions, from how to maximize returns on Harvard’s cash to using financial instruments called swaps, to hedge against the risk of rising interest rates – a hedge that would ultimately backfire.

In Harvard’s 2001-2002 financial report, Summers’s opening letter states, “During my first year as President, we took the opportunity to look anew at some of Harvard’s financial procedures to make sure we are making the most of our resources.’’ He closes the letter noting the need for “prudent fiscal management.’’

Despite the warnings from Meyer, Harvard Management’s chief for 15 years, Summers felt the cash risk was worth taking at the time, according to people who know him. He was not the sole decision maker on the matter: Members of the financial staff, a broader financial advisory committee, and the university’s elite six-member board all weighed in. But Summers was a powerful advocate, and with the returns so good for so long, there was little support for exercising caution.

And soon, Harvard would enter a period of upheaval. Meyer left in the fall of 2005, after clashing with Summers over the compensation of the endowment staff. And Summers announced his own resignation in February 2006 – as it happened, just days after the arrival of Meyer’s successor, El-Erian. A month later, Harvard’s top in-house financial official, Ann E. Berman, vice president for finance, also resigned.

Summers was gone by July that year, but not before El-Erian issued a new round of warnings about what he saw as an alarming amount of cash being put at risk in the endowment pool, according to several people who were there. El-Erian left Harvard after just two years, at the end of 2007, to return to his old bond firm, PIMCO. Both he and Meyer declined to comment on whether the cash concerns contributed to their decision to leave.

For other university officials, warnings about Harvard’s finances were easy to gloss over. The endowment had been a virtual money machine for more than 15 years, and the markets were still rising in 2006. And after Summers resigned, forced out by an angry faculty after comments about women lagging in the sciences and other controversies, there were more urgent fires to tend to.

Derek Bok, a former Harvard president from the ’70s and ’80s, took over as interim president. He was, by his own admission, unplugged from the complexities of the financial picture.

“I concentrated on academic issues,’’ Bok said in a Globe interview. He said that his strength was not in investments and that Harvard had an experienced treasurer and board to oversee those issues. “I think they would have come to see me if there were really important changes,’’ he said.

Harry Lewis, a Harvard professor and a former dean of the college, attributes the failure to address the university’s financial risks to the ancient structure of the Harvard corporation, which functions as its board. “With only the six fellows plus the president, there is inevitably going be a lot of deference to the people who seem to have the most authority, especially if the president is strong-willed,’’ Lewis said. “Whether or not anyone in particular made a mistake in this situation, it shows a fundamental structural problem. The power is just in the hands of too few people with too little accountability.’’

The cash in the general operating account exceeded $6 billion by the time Bok and El-Erian left. Problems were starting to surface in housing and the credit markets in 2007. But still the cash policy went unchanged. It wasn’t until early 2008 that a chorus of concern was rising from members of the financial staff, professors on advisory committees, and the board. They decided to start pulling some of the cash out of the endowment – in $250 million chunks – quarterly, according to Harvard officials briefed on the plan. But it was too late. They got one slug of money out in March 2008, and then the markets seized up.

The very thing that the former endowment chiefs had worried about and warned of for so long then came to pass. Amid plunging global markets, Harvard would lose not only 27 percent of its $37 billion endowment in 2008, but $1.8 billion of the general operating cash – or 27 percent of some $6 billion invested. Harvard also would pay $500 million to get out of the interest-rate swaps Summers had entered into, which imploded when rates fell instead of rising. The university would have to issue $1.5 billion in bonds to shore up its cash position, on top of another $1 billion debt sale. And there were layoffs, pay freezes, and deep, university-wide budget cuts.

While the global markets were in freefall in September 2008, the nation’s most prominent university, with the largest endowment, had barely enough financial hands on deck.

On campus, Daniel Shore was technically the guy at the controls. He was acting chief financial officer and would formally get the job, and the vice president’s title, in October. He was the third person to hold the job in as many years. The head of the endowment was new. And the Goldman Sachs & Co. veteran whom President Drew Faust had just hired to report to her on the university’s finances, Edward Forst, was summoned to Washington for a month to help with the federal bank bailout.

Rothenberg, the treasurer, was home in Los Angeles, tending to his day job as a mutual fund executive. Since becoming treasurer in 2004, in the Summers era, Rothenberg, 63, has made 65 cross-country flights to Cambridge, slightly more often than monthly, according to a tally by his assistant. He handles other Harvard business by telephone, including early-morning conference calls with overseers. But he earns his living as chairman of Capital Research and Management Co., a $900 billion-asset investment firm that manages the American Funds and is admired for producing steadier returns than many rivals, and losing less in bad times. Rothenberg is also a portfolio manager, personally handling billions of dollars in two giant funds, the Growth Fund of America and the Washington Mutual Investors Fund.

In a March 2007 interview, Rothenberg told the Harvard Gazette, “Most investors invest looking in the rearview mirror. The problem with that is you make the most money by anticipating change. I spend a great deal of my time thinking about how the world will look three or four years from now.’’

Even with the losses, Rothenberg said, the cash strategy has earned Harvard returns averaging 8.9 percent over the past 10 years. He and other university officials say the cash pool is still ahead of where it would have been, if invested more conservatively all along. But no one could be specific about what that net gain has been.

Harvard won’t stop investing the cash entirely, Rothenberg said, but the past year has “taught us a great deal about the critical importance of maintaining an appropriate focus on risk and liquidity,’’ he told the Globe.

No one wants to repeat the black day when university officials had to swallow hard and reveal a $1.8 billion loss. For Harvard’s 30 overseers, that news came as a surprise, a full year after they’d been told to expect losses in the endowment. It came at an Oct. 4 meeting on campus, just days before the university disclosed the news publicly.

Said one overseer, speaking on the condition of anonymity because he wasn’t authorized to talk about Harvard business: “It wasn’t a happy thing.’’

Source:

Harvard ignored warnings about investments

Advisers told Summers, others not to put so much cash in market; losses hit $1.8b

By Beth Healy

Globe Staff November 29, 2009 http://archive.boston.com/news/local/massachusetts/articles/2009/11/29/harvard_ignored_warnings_about_investments/

Beth Healy can be reached at bhealy@globe.com. ![]()