Treasury’s Missed Opportunity

Money and Banking, June 19, 2017

“…we expect to be cutting a lot out of Dodd-Frank because, frankly, I have so many people, friends of mine that have nice businesses that can’t borrow money, they just can’t get any money because the banks won’t let them borrow because of the rules and regulations in Dodd-Frank….” President Donald Trump’s remarks to the initial gathering of his Strategic and Policy Forum, February 3, 2017.

“The number one problem with Dodd-Frank is that it’s way too complicated and cuts back lending. So we want to strip back parts of Dodd-Frank that prevent banks from lending. And that will be the number one priority on the regulatory side.” Then Treasury Secretary-nominee Steven Mnuchin, CNBC transcript, November 30, 2016.

Last week, the U.S. Treasury published the first of four reports designed to implement the seven core principles for regulating the U.S. financial system announced in President Trump’s Executive Order 13772 (February 3, 2017). The 147-page report focuses on depositories. Future reports are slated to address “markets, liquidity, central clearing, financial products, asset management, insurance, and innovation, among other key areas.”

Seven years after the passage of Dodd-Frank, it’s entirely appropriate to take stock of the changes it wrought, whether they have been effective, and whether in certain cases they went too far or in others not far enough. President Trump’s stated principles provide an attractive basis for making the financial system both more cost-effective and safer. And much of the Treasury report focuses on welcome proposals to reduce the unwarranted compliance burden imposed by a range of regulations and supervisory actions on small and medium-sized depositories that—if adequately capitalized—pose no threat to the financial system. We hope these will be viewed universally as “motherhood and apple pie.” Others, like the recommendation to relax the Volcker Rule, will be more controversial, but nevertheless warranted in terms of a regulatory cost-benefit analysis.

Unfortunately, at least when considering the largest banks, our conclusion is that adopting the Treasury’s recommendations would sacrifice resilience to achieve cost reductions, yet with little prospect for boosting economic growth. At times, the proposals read more like a financial industry wish-list (see, for example, here) than a desirable and impartial balancing of the country’s needs for both a vibrant and resilient financial system. Put simply, implementation of the Treasury plan would reduce regulation of the most systemic intermediaries, and in so doing, unacceptably reduce the resilience of the U.S. financial system.

It is important to understand that much of the Treasury plan can be enacted by regulators without any legislative action whatsoever. By next year, President Trump will either have replaced, or have had the opportunity to replace, the heads of all the federal depository regulators (Federal Reserve, Comptroller of the Currency, Federal Deposit Insurance Corporation, and National Credit Union Administration). Consequently, many features of the plan are likely to be implemented.

The Treasury report is far too complex and detailed for us to assess it fully in a single blog post. The summary tables (Appendix B) alone present more than 100 bulleted recommendations in areas ranging from capital and liquidity requirements, to living wills and small business lending. Many of these ideas mirror features of the Financial CHOICE Act, passed earlier this month by the House.

Looking at the long list, the most troubling elements of the Treasury’s analysis—what will reduce safety the most—are the proposals aimed at relaxing the stringent oversight and capital requirements that have been imposed since the Dodd-Frank Act on a few very large, complex and highly interconnected U.S. banks. (At the end of 2016, only 36 out of some 12,000 depositories had assets exceeding $100 billion (see here), but these accounted for more than three-fourths of assets in the system.) Again, this pattern mirrors the CHOICE Act, which would relax the regulatory regime over systemic intermediaries in the name of promoting a more cost-effective framework for small and medium-sized banks.

Perhaps the fundamental problem with the Treasury report is the weakness of its two key premises: (1) that post-crisis financial regulation (particularly Dodd-Frank) has impeded bank lending, making it an important contributor to the weakness of the recovery; and (2) concern that “an excess of capital” in the banking sector “will detract from the flow of consumer and commercial credit and can inhibit economic growth.”

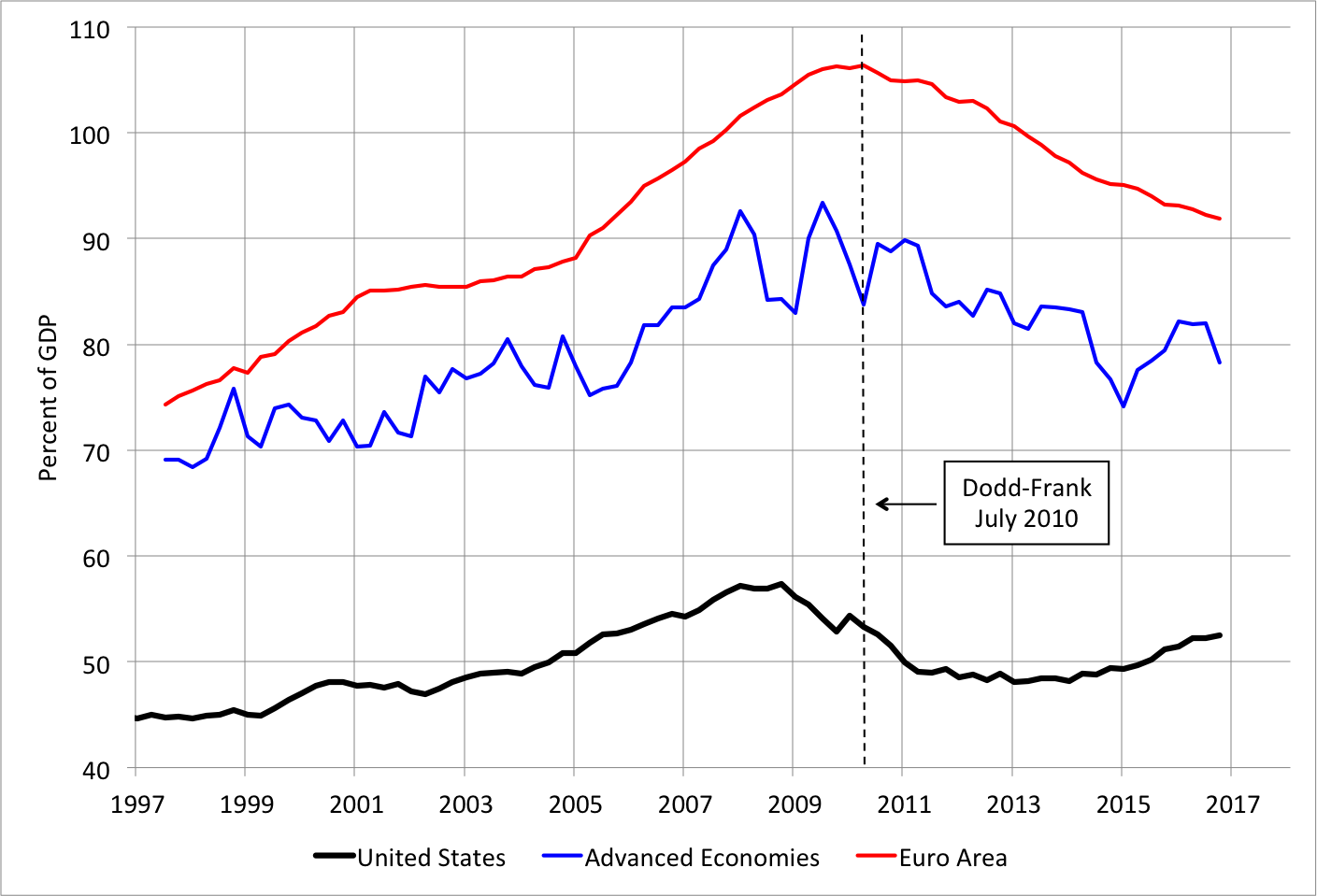

Starting with the recovery, the first question is whether lending has in fact been unusually weak. The chart below shows bank lending to the private nonfinancial sector (including households and businesses) as a percent of GDP in the United States (black line), the euro area (red line) and the advanced economies as a whole (blue line). In the United States, the bank credit ratio declined during and after the deep recession of 2007-2009. But—in sharp contrast to the euro area or the broader set of advanced economies— it has now been rising for more than four years. By 2016, credit to GDP exceeded the average reached in 2005, a year of abundant credit supply that helped fuel the financial crisis. Consequently, despite Dodd-Frank’s well-known compliance costs and distortions, there is little evidence that, since it was enacted in July 2010, it has held back overall bank lending.

Bank lending to the private nonfinancial sector (Quarterly, percent of GDP), 1997-2016

Source: Bank for International Settlements.

The Treasury report alleges constraints at a disaggregated level—that the new regulations are holding back bank lending to small businesses and for residential mortgages. Once again, however, the case is very weak. According to the National Federation of Independent Business’s May 2017 survey, only 3 percent of small firms viewed their borrowing needs as not satisfied, while only 1 percent identified finance as their top problem, far below the shares listing taxes (22 percent), quality of labor (19 percent), and government red tape (13 percent). Similarly, the Financial Accounts of the United States (Table L. 104) show that loans to nonfinancial noncorporate business hit a record $5.1 trillion in the first quarter of 2017, up by nearly 29 percent since the passage of Dodd-Frank, a tad larger than the rise of nominal GDP.

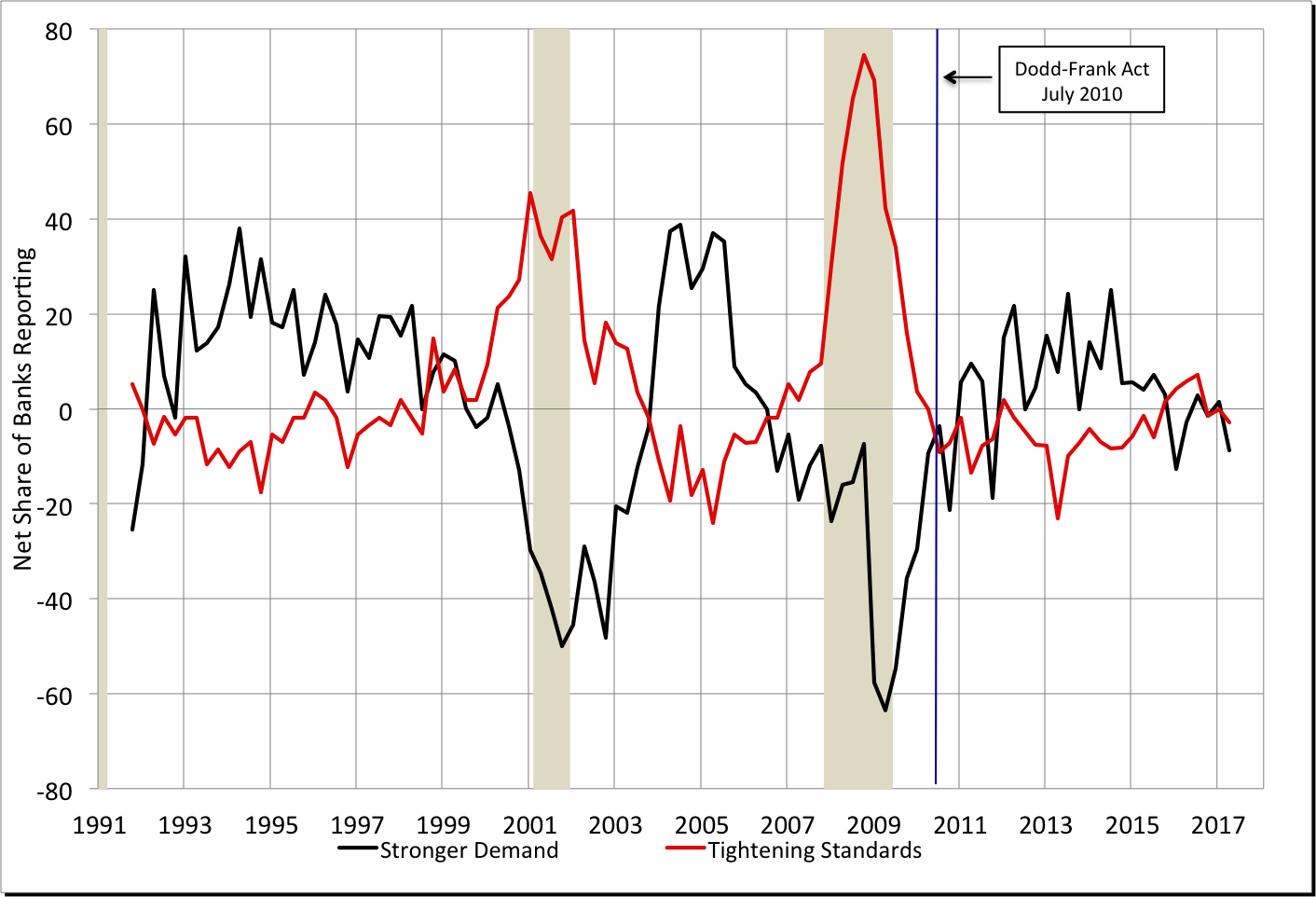

Moreover, there is little evidence of any new regulation-related constraints on the willingness of banks to lend to small firms. According to the Fed’s quarterly survey of senior loan officers, banks tightened lending conditions sharply during the Great Recession, while the recession depressed firms’ demand for funds (see chart below). However, in the period since the July 2010 enactment of Dodd-Frank, there is no unusual pattern of tightening credit supply in the survey. Keep in mind that, because small firms often use real estate as collateral, increased awareness of the risks in commercial real estate could warrant greater bank lending caution. Overall, however, when we look at both the demand side, as reported by the firms, and the supply side, from surveys of the banks, we are led to conclude that credit conditions for small business are supportive of economic growth.

United States: Net shares of banks tightening lending conditions to small firms and facing increased loan demand from small firms compared to three months earlier (quarterly), 2Q 1990-2Q 2017

Note: Shaded areas denote recessions. Source: Federal Reserve Senior Loan Officer Opinion Survey.

The slow recovery of household mortgages presents a stronger case for a constraint on credit supply. Households have delevered substantially since the crisis—lowering the ratio of liabilities to disposable income by 30 percentage points from the 2007 peak—while rising asset prices boosted their net worth to a record 6.6 times disposable income in the first quarter of 2017. Yet, according to the Urban Institute’s Housing Credit Availability Index, the willingness of lenders to tolerate borrower default risk has not recovered to levels that prevailed in the early 2000s, prior to the pre-crisis credit bonanza. In addition, the market for private-label securitizations remains a fraction of its pre-crisis size.

However, we question whether regulations are the primary cause of this hesitance to lend. Having been burned in the earlier private-label securitization boom, creditors are naturally reluctant to trust the process (see, for example, Goodman). In addition to concerns about originator and issuer conflicts of interest, potential buyers worry about litigation risk that may accompany any improperly originated loans in the securitization pool. This naturally favors reliance on the mortgage pools guaranteed by government-sponsored enterprises (GSEs), which still dominate U.S. housing finance.

Moreover, in contrast to the Treasury’s assertions of regulatory constraint, private funds are clearly being supplied to absorb mortgage risk through credit risk transfers (CRTs) from the GSEs. Since 2013, Fannie and Freddie have sold off to private investors 29 percent and 42 percent, respectively, of the risk from their outstanding guarantees (see page 22 of the Urban Institute’s May 2017 Housing Finance at a Glance). This year, their regulator is calling for the credit risk transfer of 90 percent of new guarantees. (While a broad privatization of the mortgage market would be far better over the long run—see Richardson, van Nieuwerburgh and White—expanding CRTs to limit the government’s role to that of catastrophic insurer would help restore private willingness to absorb mortgage risk as the key market driver.)

What about the Treasury’s second premise—that an “excess of capital” is constraining the supply of bank credit? Neither theory nor experience provide much support for this common industry view. The most fundamental theorem of corporate finance implies that firms should be indifferent about the composition of their financing (see, for example, Admati and Hellwig). And, a range of evidence suggests that better capitalized banks lend more (and lend better), not the other way around. First, rather than boosting costs, higher capital requirements in the aftermath of the crisis were associated with narrower interest rate spreads and lower operating costs for internationally active banks (see here). Second, increases in capitalization tend to lower funding costs and increase lending volumes (see Gambacorta and Shin). Finally, we have learned at great social cost that when banks accumulate high levels of debt—especially Japan in the 1990s and the euro area in recent years—they then lend to zombie firms in a way that hurts, rather than fosters, economic growth (see Caballero, Hoshi and Kashyap for Japan and Acharya et al for the euro area).

Looking at some of the report details, our conclusion is that the Treasury’s new regulatory approach potentially adds to systemic risk. The prime reason is that it would relax constraints on the small number of systemic intermediaries that account for the lion’s share of U.S. banking assets. To keep the discussion short, we’ll provide five examples.

- First, and most important, Treasury “supports an off-ramp exemption” from stress tests and other prudential standards for banks with sufficient capital, citing the 10-percent leverage ratio threshold in the CHOICE Act. While adequate capitalization ought to be sufficient to relax scrutiny of most banks, an off-ramp for supervision of the largest, most complex, most interconnected players would invite renewed gaming of the rules that can make the system fragile. The key point is that capital can be difficult to measure (see, for example, here and here), while the complex activities of some very large banks afford them the opportunity to conceal risk. The Treasury report also suggests changes in the leverage calculation, exempting certain assets, that would make banks appear better capitalized, without making them so.

- Second, while the Fed’s stress test procedures can be improved and streamlined, the Treasury report proposes changes that would make the tests insufficiently effective (including reducing their frequency and altering their modeling assumptions about capital distributions).

- Third, Treasury calls for “recalibration” in cases where regulators have set requirements on the largest U.S. banks in excess of international standards (see Table 3 in the report). “Gold plating” of U.S. regulations is alleged to make U.S. firms less competitive. However, in the post-crisis world, the relatively better capitalization of top U.S. banks compared to European banks has not prevented them from competing and may even have served as a competitive advantage on the international stage.

- Fourth, Treasury would remove the FDIC from the review of banks’ “living wills”—the documents that the largest banks must prepare to simplify their resolution in a crisis. Excluding the FDIC from this process is inconsistent with its Orderly Liquidation Authority (OLA) so, absent other changes, it would threaten the credibility of the resolution process for too-big-to-fail banks. While the Treasury does not address OLA in this report (it will do so later in response to the Presidential Memorandum of April 21), it is difficult to interpret this living-will proposal as something other than a strike against OLA (again mirroring the Financial CHOICE Act’s abolition of OLA).

- Finally, Treasury would relax current or planned liquidity requirements. One example would be to include highly illiquid municipal debt in the definition of high-quality liquid assets (page 54 of the report and our earlier discussion here).

We could go on about ways in which the Treasury report downplays important mechanisms to control or anticipate systemic risk and build resilience. For example, Treasury criticizes activities-based regulation for its impact on credit supply, but there is little evidence for that. More important, an activities orientation helps focus regulation on economic function, in contrast to the usual regulation by legal form of the intermediary (which promotes shifting rather than reducing systemic risk).

The bottom line: only 8 years after the end of the worst financial crisis since the Great Depression, the U.S. Treasury has shifted from becoming a leading proponent for enhancing the resilience of the global financial system to an advocate for the private interests of a few financial behemoths in the name of boosting growth. At the same time, Treasury’s aim to enhance the supply of credit as a means to increase economic growth—expressed by the President and his then-Secretary-designate in the opening quotes—is, at best, unlikely to have much growth impact. We can only hope that, in the future, we won’t look back at Treasury’s shift as the start of a trend that once again makes our financial system highly vulnerable to severe disruption.

Disclosure: One of us currently serves on the Financial Research Advisory Committee of Treasury’s Office of Financial Research (OFR).

Source: Money and Banking