Only the Foolish Pay the 45% Estate Tax

Nobody pays the 45 percent estate tax unless they want to or they’re not too bright.

Bloomberg, January 30, 2014

By now, you must have heard about Tom Perkins’ letter to the Wall Street Journal (Progressive Kristallnacht Coming?), where he made a foolish comparison to the “parallels of fascist Nazi Germany to its war on its ‘one percent,’ namely its Jews, to the progressive war on the American one percent, namely the ‘rich.’ ”

The PR disaster Perkins ignited – yeah, he is that Perkins from venture capital firm Kleiner Perkins – ignited a firestorm. The reaction was so intense he had to go on Bloomberg TV to sort of, but not quite, apologize. In the course of his comments, he said something several other really dumb things (you may be detecting a pattern here) on unrelated subjects.

But the thing which really stood out to me was his plea for lower taxes. Perkins said: “Upon my death the government will take 45%” of my estate.

To which I am compelled to respond: Only if you are an idiot.

Or, perhaps, if you were on the way to your lawyer’s office when you got hit by a bus, and died intestate (without a will), then that makes sense as well. Short of those things occurring, no one in America actually pays “45 percent” in estate taxes. It is simply too easy to avoid paying estate taxes. (The top federal rate currently is 40 percent, although in some states the total bill can easily reach the Perkins 45 percent level.)

First, some numbers: About 314 million people live in the U.S. Each year, a bit fewer than 2.5 million people shuffle off this mortal coil, according to the Centers for Disease Control and Prevention. The first $5.25 million is exempt from estate taxes (double that for married spouses). In other words, only the wealthiest 0.14 percent of Americans pay any estate tax. That’s fewer than two out of every 1,000 people who die.

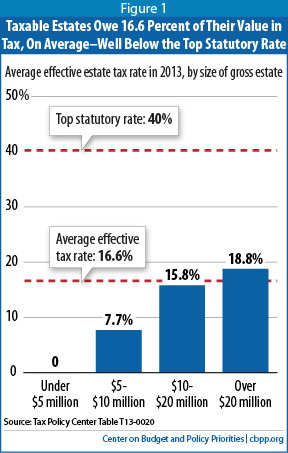

But here’s where things get interesting: With a little planning, those folks don’t pay anywhere near a 45 percent rate. As the Center on Budget and Policy Priorities has observed, a more typical tax rate on large estates is about 17 percent.

Take a guy like Perkins, who said “I am not a billionaire.” Let’s assume he has a net worth of $100 million dollars (or some multiple of that). It is a rather simple thing to reduce his estate taxes to almost zero.

I am not referring to any complex or exotic tax strategies like the “Double Irish” or “Dutch Sandwich” that so many American companies have used to great effect. Rather, all that is required is some basic planning using run-of-the-mill insurance policies and trusts. Nothing cutting edge or daring, just put a few well-paid lawyers, accountants, and financial planners to work using existing policies and tax laws.

If you don’t want to pay a 45 percent estate tax, consider these four basic strategies:

Second-to-die life insurance is a very effective tool. Combined with an irrevocable life insurance trust (ILIT), this allows a fortune to pass to the next generation effectively tax-free. Uncle Sam still gets his cut paid out by the insurer, but to the estate it looks and feels like there are no taxes to be paid. The costs are the premiums (which vary by the age and health of the insured), plus whatever your lawyer charges you to set up the trust. Figure that two 60 year olds in good health will pay about $20,000 per $1 million for the insurance; the trust costs less than $10,000. For Perkins’s $100 million dollar estate, avoiding a 45 percent tax would cost about $750,000 per year. Not cheap, but that avoids $45 million in estate taxes right off the top.

Grantor retained annuity trust, or GRAT, is another commonly used tool. It not only avoids the estate tax, but sidesteps any gift taxes as well. This trust’s donor (that’s you) receives annual payments during a fixed period of time (that’s the annuity part). Once this term ends, the remaining value gets passed on to the named beneficiary as a tax-free gift. No worries if you aren’t around to see that; this trust allows the balance to pass to the beneficiary free of estate tax also.

Charitable giving with a charitable remainder unit trust (CRUT) is a similar mechanism. Similarly to the GRAT, the CRUT pays out income over the lifetime of the donor, then provides your selected charities with the remaining principal. The inverse of the GRUT is the charitable lead trust (CLT). Income during your lifetime goes to your favorite charity, and the principal at your death goes to your beneficiaries. (Note: the CLT has some complications to it).

Of course, the easiest way to avoid estate taxes is to give it all away. Warren Buffett decided to put his entire $60 billion fortune in the Bill & Melinda Gates Foundation, run by his pal Bill Gates. Uncle Sam’s take is precisely zero.

While the formal rate on any estate greater than $10.5 million dollars per couple can reach 45 percent, nobody actually pays that. Not unless they’re an idiot.

Originally Only the Foolish Pay the 45% Estate Tax

What's been said:

Discussions found on the web: