The Economic Populist is a Community Blog and Forum. Leave your partisanship at the door, bring your shrinking middle class paycheck and let’s discuss real trade, economic, budget, fiscal, tax, labor and immigration policy that is in our interests and the United States National Interest

~~~

On December 3, John Bergstrom of Bergrstrom Automotive, a major auto dealer, appeared on CNBC and said,

on about September 10, we saw our business fall off 30-35%.

A similar sudden decline in consumer spending during September was reported by Shoppertrak:

Throughout 2008, the American shopper has endured record high gasoline prices, hurricanes and flooding, and a stalled housing market in their quest to shop. While the consumer has remained fairly resilient during this time, two very recent events are dramatically impacting mall visits and consumer confidence.

– Once the financial crisis emerged at the beginning of September, retail traffic declined even further. Between August 31 and September 20, SRTI total U.S. traffic fell an estimated 9.2 percent per day….

– After the failure of Washington Mutual, President Bush’s address to the nation, the presidential debate and the initial rejection of the TARP bailout, traffic fell by an average of 10.5 percent (September 21 – 29).

– The day the TARP bailout package was rejected by congress (September 29) and the NYSE Dow Jones Industrial Average lost 778 points, consumers again responded negatively as shopper traffic fell 12 percent as compared to the same day in 2007

– Sales, which were up 4.0 Percent for the Month of July, and up 3.5 Percent for the Month of August, fell 1.0 percent in September – “the first year-over-year sales decline since March 2003.”

Shoppertrak has subsequently reported that “retail sales rebounded slightly, posting a very slight 0.7 percent increase in October. sales for the week ending November 15 dropped 3.1 percent as compared to the same period in 2007.” But car sales have not recovered at all. In August car sales were already down about 19% YoY. In September the loss was 21%. In October it was 23%. By November car sales had declined close to 40% from already depressed levels in 2007.

And the stock market, which was only down (-18%) from its all time high in 2007 of 1565 to 1282 at the end of August, by October 10 was down (-43%) to 899.

In the 40 day period between September 1 and October 10, the shallow recession which had crippled the housing industry and Wall Street, but left Main Street virtually intact, suddenly metastasized into a collapse of the consumer economy that some were beginning to liken to the 1930s.

This diary is “the first draft of history”, an attempt to look at not only what has happened, but as best we can tell from the vantage point of several months later, why it happened.

Part 1. In August, the Real Economy just had a Cold

Now we know. From the vantage point of December 2008, the NBER, which is the official arbiter of these thiings, has reported that a recession began a year ago in December 2007. The official report of GDP for the 4th quarter of 2007 shows a decline of ( -0.2%). Until revised away (not unlikely) the first quarter of 2008 was mildly positive ( +0.9%), and marked by the receipt of $250 billion worth of stimulus checks, the 2nd quarter of 2008 was more robust at ( +1.9%). By the end of August, it seemed likely that the economy was undergoing a mild recession even though Wall Street was suffering a near-catastrophe.

The first ill winds of the present calamity began in February 2007 as the “subprime mortgage market” began to collapse, with mortgage brokers “Imploding” seemingly by the day. Although the Best and Brightest of new finance assured us that this was a minor, “contained” malady, in August 2007 the destruction of bad debt suddenly spread to hedge funds, as two Bear Sterns funds which had improvidently made leveraged bets on bad mortgages, blew up. Despite this the stock market made new highs in October 2007, as measured in both the DJIA and the S&P 500, before beginning to decline.

In March 2008 the financial system suffered its first major shock with the failure and forced merger of Bear Sterns, Wall Street’s fifth largest investment bank. Many thought that the worst was over, and stock markets ralied back for several months. Then, in July, after unnerving warnings from the Bank of International Settlements in its annual report warning of a global economy at a “tipping point,” and possibly an orchestrated bear raidcampaign of naked shorting, America’s two mortgage giants, Fannie Mae and Freddie Mac, nearly failed and at the insistence of foreign sovereign bondholders, the US formally agreed to backstop their debt. This happened only days after Fed Chairman Ben Bernanke told Congress that the two mortgage giants were adequately capitalized, and were in no danger of failing.

At virtually the same time, one of the biggest bank underwriters of toxic subprime mortgages, Indy Mac Bank, failed, and was taken over by the FDIC, resulting in a ~$6 billion loss to the fund, the second largest outlay ever.

Despite all of these things, the unfolding events seemed to be a Neutron Bomb over Wall Street, leaving Main Street unscathed. For example, Prof. Brad DeLong, who has been an astute observer of the collapse, noted that

The Financial Economy Has Galloping Pneumonia, Influenza, *and* the Grippe, But the Real Economy Just Has a Cold

,,,,the U.S. economy expanded in the second quarter, and not at too shabby a rate considering the many drags… about a 2.5 percent annual rate in the second quarter…. “The second quarter appears to be actually better than expected,” Federal Reserve Chairman Ben S. Bernanke said at a congressional hearing on July 15. “We’re looking at the remainder of the year as being probably positive growth but certainly not robust growth.”…

The August Fed Beige Book reported that the pace of economic activity was slow in most Districts. Many described business conditions as “weak,” “soft,” or “subdued.” The graphs below, all taken from that time show an economy that was weak, but growing in some areas, but in recession-ish territory in others, although still not even as bad as the very shallow recession of 2001 which barely affected consumers at all.

For example, ISM manufacturing and service indeces were lukewarm:

Retail sales were positive year over year at least on a nominal basis:

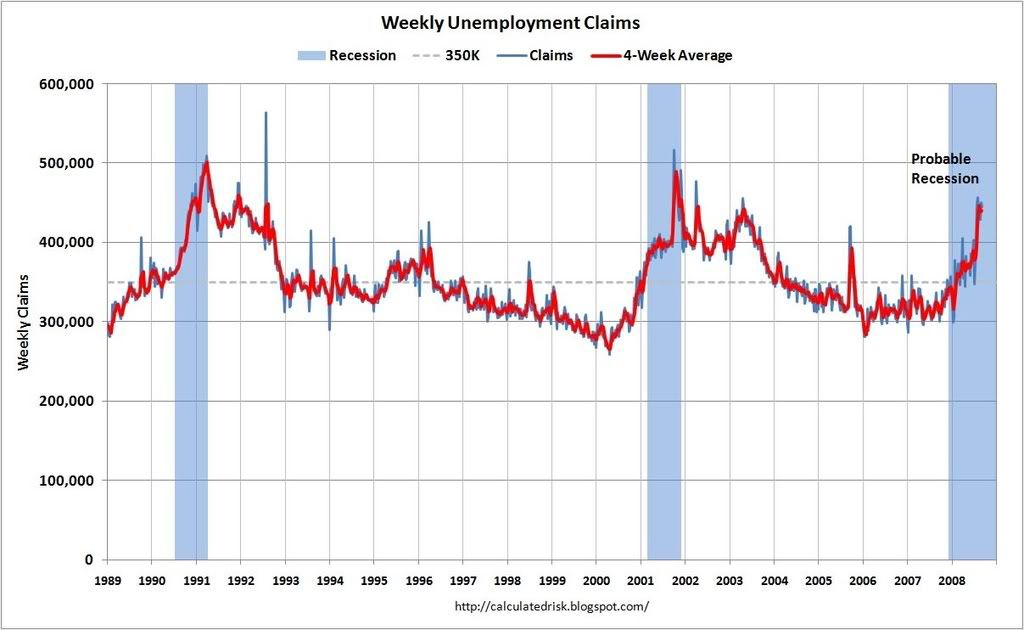

And unemployment was no worse than in 2001 or 1991:

In short, the August picture of the economy as a whole showed a recession, but so far a shallow one.

Part 2: September. A Chronology of Corporate Collapse and Government Panic

Even as late as September 5, only five days before Bergstrom’s auto dealerships saw a precipitous decline in foot traffic,a blogger at Angry Bear noted:

this is looking like an extended shallow near recession.

But only 11 days later, commentators like myself and Prof. Brad DeLong were noting that Main Street was finally becoming infected by the slowdown:

For about a year we have been blessing the disconnect between financial chaos and construction depression on the one side and real-side economic “weakness” elsewhere in the economy. Let’s hope the disconnect continues. But it looks as though it isn’t: the recession has spread out from construction into goods production broadly

And by the 30th of the month, an analyst was lamenting that:

The money markets have completely broken down, with no trading taking place at all. There is no market any more. Central banks are the only providers of cash to the market, no-one else is lending.”

The onrush of the stunning financial mishaps that took place in that brief time is shown in the day by day chronology of events below, culled from news sources and the archives of The Big Picture and Calculated Risk:

- Sept. 2

- market starts at 11,800 rolls over for no apparent good reason ends at 11,500

- and T Boone Pickens predicts Oil will hit a new record by the end of 2008

- Sept 3

- reports that Aug auto sales off about 20% year over year

- Sept 4

- Societe Generale predicts stock market meltdown is “imminent”, says corporate profits for Q2 down dramatically

- Sept 5

- first 100,000 non-farm payroll loss shown for June, Aug nonfarm payrolls are -84,000

- Report that treasury is going to do $500Bln bailout/backstop of Fannie/Freddie in a “conservatorship”

- Sept 6-7

- weekend leaks about Fannie/Freddie bailout continue (announced officially Sun)

- Sept 8

- Prof. James Hamilton’s recession indicator spikes to 95%

- Big Picture blog reports huge spike in traffic

- Treasury officially takes control of Fannie/Freddie

- The late Tanta, in one of her last posts notes that US Today headline says taxpayers on hook for $5.4 trillion, says that’s what average Americans are reading

- WaMu in “memo of understanding” w/ OTS

- Sept 9

- Lehman in imminent peril per news – faills from $13 to $9 in one day – put on “credit watch” by S & P

- hedge funds reported to be raising cash for major redemptions later in Sept.

- DJIA falls from 11,500 to 11,230

- WaMu “cliff diving” credit outlook cut to “negative”

- Sept 10

- WSJ rpts intervention/bailouts losing ability to boost market

- WaMu “cliff diving” more

- Sept 11

- Lehman falls to $4, WaMu to $2 Merrill Lynch at $9

- Lehman bailout expected over the weekend

- Sept 12

- reports: no deal for Lehman

- retail sales in Aug off -0.3

- WaMu in advanced talks with JP Morgan Chase, losses rising rapidly

- AIG threatened with credit downgrade

- Sept 14

- report: Lehman liquidation likely

- Merrill sold to Bank of America

- Sept 15

- Lehman fails

- AIG seeks $40 Billion bailout, is downgraded

- DJIA falls 500 to 10,900

- Big Picture reports traffic explodes

- Prof. Paul Krugman calls allowing Lehman to fail “financial russian roulette” with entire financial system

- Ted spread increases to over 2%

- WaMu bonds cut to junk rating

- Sept 16

- US considering AIG “conservatorship” agrees to inject $85 billion to AIG to avoid collapse. Breadth of AIG failure a complete surprise

- The NYT reports:

If A.I.G. had collapsed — and been unable to pay all of its insurance claims — institutional investors around the world would have been instantly forced to reappraise the value of those securities, which in turn would have reduced their own capital and the value of their own debt.

- rumor that large money market fund has halted redemptions

- Sept 17

- Ted spread to 2.76$

- Goldman, Wachovia, Morgan Stanley cliff diving

- WaMu for sale

- Sept 18

- report: SEC leverage exemption of 5 Wall Street firms helped lead to collapse

- Vix spike to 40

- SEC to ban short selling

- Putnam, BNY Mellon money market funds break the buck, collapse, close

- DJIA ends week at 11,400

- Big Picture blog reports all time daily high of 158,000 traffic

- commercial paper yield blowout

- WaMu gets no bidders

- Sept 19

- Treasury to insure money market funds possible downgrades of MBIA, Ambac

- From the NY Times: Congressional Leaders Stunned by Warnings

As the Fed chairman, Ben S. Bernanke, laid out the potentially devastating ramifications of the financial crisis before congressional leaders on Thursday night, there was a stunned silence at first. Senator Christopher J. Dodd [said] the congressional leaders were told “that we’re literally maybe days away from a complete meltdown of our financial system, with all the implications here at home and globally.”

- Sept 21

- Paulson announces $700 bln bailout plan

- WaMu says talks continuing

- Sept 23

- Paulson and Bernanke to testify before Congress

- report: hedge funds suffer mass redemptions

- Sept 24

- Ted spread at 3.02%

- Standards & Poors, Fitch cut WaMu to poor quality

- From the WSJ: Bush Addresses Bailout Plan

President George W. Bush on Wednesday warned Americans and legislators reluctant to pass a historic financial rescue plan that failing to act fast risks wiping out retirement savings, rising foreclosures, lost jobs, closed business and “a long and painful recession.”

- From the NY Times: President Issues Warning to Americans

- From the WaPo: Bush: ‘Our Entire Economy Is in Danger’

Bush painted a grim picture view of the future if Congress doesn’t act, but he really didn’t address how the plan would work. Bush did comment that the plan was to buy assets “at the current low price”, seemingly contradicting the comments from Bernanke and Paulson earlier today that they would buy at above the current “fire sale” prices.

- Calculated Risk observes:

I’m not sure if this speech will motivate people to call their representatives, but it might motivate people that haven’t been paying attention to say: “Wow, this is bad. Let’s make sure our money is safe, and watch our expenditures.” And that could lead to a deeper recession.

- Sept 25

- WaMu fails, is sold to JP Morgan Chase

- Ted spread at 3.27%

- Sept 26

- Wachovia, National City banks “cliff diving”

- Sept 27

- From MarketWatch: Bush confident of financial rescue plan bill ‘very soon’

President Bush said Saturday morning he’s confident that Congress will pass a bill … “very soon.” … The president also stressed … “our entire economy is in danger.” Negotiators from Congress and the administration are returning to talks Saturday with an eye toward finalizing a deal by Sunday.

- From MarketWatch: Bush confident of financial rescue plan bill ‘very soon’

- Sept 28

- Wachovia folds, to be acquired by Citigroup

- Sept 29

- bailout plan passed DJIA off 330

- house of representatives votes down plan, DJIA off 770 interday

- opens at 11,000, closes at 10,600

- Sept 30

- Libor surges overnight by 4.31% to 6.88%

- Christoph Rieger, a fixed- income strategist at Dresdner Kleinwort, says:

“The money markets have completely broken down, with no trading taking place at all. There is no market any more. Central banks are the only providers of cash to the market, no-one else is lending.”

- Last day to get in requests for hedge fund redemptions

- Financial markets react with relief to the news of the bailout. Stocks up ~1% in the US, up ~2% in Asian markets

It would have been a chain reaction,” said Uwe Reinhardt, a professor of economics at Princeton University. “The spillover effects could have been incredible.

The business and financial losses of the companies that unfolded in September were almost certainly by that time unavoidable. What was capable of being controlled was the Government’s reaction to them.

And what positively leaps out from the chronology is how officials of the already higly unpopular Administration and Congress, who particularly in a crisis should have projected control, competence and confidence, instead came off as perplexed, unnerved, and arbitrary. The Treasury Secretary dithered over whether to save Lehman or not; the Federal Reserve Chairman spoke of being days away from total financial meltdown. Worse, leaders of Congress leaked the depth of the officials’ panic to the public, and then with no assurances that disaster can be averted. Worst of all, in a complete reversal from FDR nostrum that all that had to be feared was fear itself, the President himself told the American people that their “entire economy is in danger.”

Coupled with a media that portrayed events in the most dire and sensationalistic way, subconsciously the message that was conveyed to the American people was indeed:

“Wow, this is bad. Let’s make sure our money is safe, and watch our expenditures.”

Part 3: The October aftermath

Despite all of the bad news in September — the failure of Lehman Brothers, the forced marriage of Merrill Lynch, the bank failures, the imminent failure and takeover of AIG, the takeover of Fannie and Freddie, and despite all of the other awful news from Wall and Main Streets — the DJIA ended September at 10,600. Not a pretty month, but not a crash either. On September 30, 2008, the DJIA was off only about 25% from its all-time highs. In other words, a bear market to be sure, but on the other hand, a perfectly normal bear market.

And then came the first 10 days of October. New auto sales and non-farm payrolls were bad, but not Armaggedon bad. There was one very big piece of news, and one would have expected it to have been treated as a positive: on October 3, Congress passed and Bush signed the $700 billion Wall Street bailout.

Despite this, the DJIA finished the week down 4%, and the S&P 500 fell 9%. In the next 4 days of trading, the DJIA fell another 25%, to as low as 7884 at its low on October 10. Market observers at the time seemed mystified. A perfectly normal market would, at 3 p.m. each afternoon, decline precipitously. If it was already off, it would just fall off a cliff. Almost as if it was an “aritificial” move.

And artificial it was. The hedge fund redemption requests of September were liquified in the early part of October, most likely intensified by forced liquidations as underwater Titanic leveraged bets spawned margin calls, spilling over into the next compartment of Titanic leveraged bets.

That hedge funds were the primary driver of the October stock market crash was revealed in statistics revealed later by CNN Money:

Hedge fund assets fell by $100 billion in October as investors withdrew their money and funds were forced to sell stock, exacerbating the severe volatility that pounded global markets during the month.

About $60 billion of the $100 billion in asset losses during the month came from investor redemptions, according to a report Wednesday released by Eurekahedge, a data and research provider. Hedge funds’ assets [had] totaled $2.497 trillion at the end of the third quarter, according to HedgeFund.net, a hedge fund data provider.

“It’s pretty clear that hedge fund redemption has had an impact,” said Donn Vickrey, co-founder and chief analyst at independent research firm Gradient Analytics.

This was hardly a trivial amount. The worth of the entire stock market, at the end of September, was about $10 Trillion, meaning that 1% of the entire value of the market was pulled out, most of it no doubt in less than 2 weeks. According to Reuters:

pension funds and wealthy individuals alike are leaving hedge funds faster than ever before, lawyers and managers said.

Between July and September, investors pulled out a record $31 billion, which helped shrink the industry 11 percent to $1.7 trillion.

Hedge funds were the primary, but not the only driver of the crash. Individual investors also pulled about $20 billion out of equity mutual funds in October, although most of the withdrawals occurred after the crash, according to Barron’s.

Part 4: The poverty effect

The decline in housing values did not have a major effect on most American consumers’ behavior. The 30%+ who do not own houses, and the 20%+ who own their houses in full, were completely unaffected. Of the remaining minority, most of them had purchased their houses before the height of the housing bubble, and although their home equity position may have declined, even now 90% of all homeowners are “above water”, meaning they have positive equity in their houses.

But the dramatic 45% decline in the stock market from its October 2007 highs is another matter entirely. It has created perhaps the biggest single negative wealth effect (let’s call it a “poverty” effect) in all of American financial history. As set forth by Brooke Harrington in Pop Finance: Investment Clubs and the New Investor Populism :

Once limited to a tiny elite among America’s wealthiest families—the 1 percent of adults who owned stocks in 1900, which by 1952 had risen to just 4 percent—investing in stocks became a mass activity, involving over half the U.S. adult population by the end of the twentieth century.2 Much of this growth in “market populism” occurred during the 1990s. For example, at the beginning of that decade, about 21 percent of American adults owned stocks; seven years later, the percentage had more than doubled, rising to 43 percent; by 1999, the figure was 53 percent. The last time the number of investors doubled in America, the change took twenty-five years: from 10 percent in 1965 to 21 percent in 1990.

Indeed, despite the hoopla about shoeshine boys and margin calls, only 3% of the public owned shares of stock at the very height of the bubble in 1929.

A recent estimate indicated that in 401(k) plans alone, 50 million participants held $3 Trillion in assets with an average balance of about $60,000. Although the top 1 percent of the US population owns just under 50 percent of all the stock outstanding, and the top 10 percent of the population owns 85 percent, a 40% loss of value in equities is a very large hit for most households to take.

Thus, although previous studies had shown that the stock market’s service as a leading barometer of the economy was was not based on the wealth effect, insofar as they were based on relatively few households’ ownership of stock, and those households primarily being those with large asset cushions, those studies almost certainly are no longer accurate given the tremendous growth of public stock market ownership. Rather:

the aggregate relationship between consumption and stock market wealth is consistent with a “direct” view of wealth effects, in which changes in total consumption stem from changes in the consumption of households that own stocks. The consumption growth of Consumer Expenditure Survey households holding securities has a strong positive correlation with both contemporaneous and lagged movements in stock prices…. Meanwhile, the consumption growth of households that do not hold securities has little correlation with movements in stock prices

In short, in Black September and the ensuing market crash of October, 78,000,000 Americans probably lost over a trillion dollars of wealth, the most tremendous downdraft in the “wealth effect” ever.

Conclusion

American consumers sustained two massive shocks as a result of Black September. First, their confidence was shattered not just by news of corporate collapses, including sensationalistic reports that they were newly responsible for trillions of dollars’ worth of mortgages, but more importantly by the magnification of those collapses by the public figures (the President, the Treasury Secretary, the Chairman of the Federal Reserve, Senator and Members of Congress) in statements that quite plainly advised Americans that imminent panic over the fate of the entire economy was a proper reaction. And panic American consumers did, as millions of households listened to a President’s speech telling them that the End was Imminent, and then had sober discussions over the kitchen table in which they decided to drastically pull back on discretionary spending, literally overnight.

Second, hope that the decimation of consumer confidence might be short-lived was destroyed as the majority of American households, including all of the more affluent middle class, saw major damage done to their balance sheets and their savings and retirement dreams in the stock market crash of October brought on by the Black September redemption orders to hedge funds. Retirement plans for peak earners in their 40s, 50s, and early 60s, suddenly were no longer viable. In their kitchen table discussions, millions of American couples decided that another 1 or 3 or 5 years of work had suddenly become likely, and additional saving a necessity.

Consumers en masse simply stopped spending, an “autonomous consumer decline” resembling the one which was critical trigger of the Great Depression. Meanwhile banks, newly refurbished by government largesse, became much more conservative about the terms of their extension of credit to those who were not the most creditworthy; and corporations determined not to wait for a rebound, but to curtail temporary hiring for the holiday season, and layoffs accelerated instead. In a grim harbinger of more financial destruction, Reuters reported that “more [hedge fund] redemptions [were] expected to flood in by November 15, the deadline to get money back by year’s end.”

A minor recession focused on Wall Street and Housing had turned into the first Major Deflationary Bust since the 1930s.

What's been said:

Discussions found on the web: