How Do I Hate Thee?

By John Mauldin

August 31, 2013

How Do I Hate Thee? Let Me Count the Ways…

The Silver Lining

Investing in a Market to Hate

Money for Nothing World Premiere in Dallas, September 6

Chicago, Bismarck, Denver, Toronto, and New York

How do I love thee? Let me count the ways.

I love thee to the depth and breadth and height

My soul can reach, when feeling out of sight

For the ends of Being and ideal Grace.

… I love thee with the breath,

Smiles, tears, of all my life! — and, if God choose,

I shall but love thee better after death.– Elizabeth Barrett Browning (1806-1861)

When I was growing up, Labor Day always marked the official end of summer, since we started school the next day. These days everyone seems to start school sometime in August, but for those of us of a certain age, the natural annual rhythm is still to see the last few days of August as the end of a carefree summer. So with a nod to your need for a little more summer relaxation, I will try to keep this letter shorter than usual. And with apologies to Elizabeth Barrett Browning, I will list a number of reasons why I hate this market and then suggest a few reasons why that should get you excited. We will look at some charts, and I’ll briefly comment on them. No deep dives this week, just a survey of the general landscape.

When I was growing up, Labor Day always marked the official end of summer, since we started school the next day. These days everyone seems to start school sometime in August, but for those of us of a certain age, the natural annual rhythm is still to see the last few days of August as the end of a carefree summer. So with a nod to your need for a little more summer relaxation, I will try to keep this letter shorter than usual. And with apologies to Elizabeth Barrett Browning, I will list a number of reasons why I hate this market and then suggest a few reasons why that should get you excited. We will look at some charts, and I’ll briefly comment on them. No deep dives this week, just a survey of the general landscape.

How Do I Hate Thee? Let Me Count the Ways…

The market is down about 3½% since early August, with trading rooms short-staffed the last few weeks. Will the senior traders come back from vacation rested and looking for value? Or will they survey the gains they have banked so far this year and decide to lock them in to assure their year-end bonuses? Finding value these days is tough. It won’t be hard for them to find reasons to head for the sidelines.

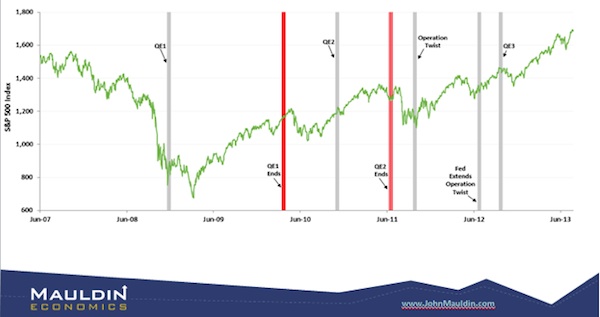

- There is a reason tapering is on everybody’s radar screen. When the Fed ended its last two rounds of quantitative easing, the resulting sell-off was not pretty. Some think that happened because the Fed was not really providing “juice” to the market. There is an element of truth to that analysis, but I think a more fundamental reason has to do with sentiment. Fighting the Fed is very difficult. Or it might be more apt to say, fighting the narrative of the Fed that produces positive sentiment is very difficult. I remember more than a few commentators coming on CNBC in January of 2001, when Greenspan lowered interest rates by 1% in the span of 30 days, and telling us “Don’t fight the Fed! You have to go long the stock market today!”

I was writing at the time that there was a recession coming, so I was saying pretty much the opposite. Perhaps the more appropriate lesson is to not fight the Fed unless there is a recession coming.

Here is a graph from a webinar (see below) that I will be doing in a few days. The last two times the Fed has ended a period of quantitative easing, the air has come out of the market balloon. Has this coming move been so telegraphed that the reaction will be different than in the past, or will we see the same result? Want to bet your bonus on it? Or your retirement?

- Global growth is in a funk (that’s a technical economic term), and this market just doesn’t seem to care. One of the first market aphorisms I learned was that copper is the metal with a PhD in economics. While you can get into a great deal of trouble regarding that as a short-term trading axiom, it is definitely a longer-term truth. Copper is a metal that is closely associated with construction, industrial development and production, and consumer spending. One can argue that the price of copper is falling today because of a fundamental increase in supply, but for those of us of a certain age, the following chart is nervous-making. Unless the long-term correlation has disappeared, the data would indicate that either the price of copper needs to rise or the market is likely to fall.

- There is a full-blown crisis developing in the emerging markets that has more than one serious commentator thinking of 1998. On Thursday, the lead article in the business section of USA Today asked “Are we poised for a repeat of 1998 — or worse?” Yet as I highlighted in last week’s Outside the Box, the US Federal Reserve has very clearly said that problems in the emerging markets are not the concern of US policy. One of my favorite thinkers, Ambrose Evans-Pritchard over at the London Telegraph, wrote this on Wednesday:

This has the makings of a grave policy error: a repeat of the dramatic events in the autumn of 1998 at best; a full-blown debacle and a slide into a second leg of the Long Slump at worst.

Emerging markets are now big enough to drag down the global economy. As Indonesia, India, Ukraine, Brazil, Turkey, Venezuela, South Africa, Russia, Thailand and Kazakhstan try to shore up their currencies, the effect is ricocheting back into the advanced world in higher borrowing costs. Even China felt compelled to sell $20bn of US Treasuries in July.

Back in 1998 the developed world was twice as big as the developing world. Today that ratio is about even. We all know what a crisis for the markets 1998 was. And now, more than a few emerging markets have clear debt problems denominated in currencies other than their own.

Evans-Pritchard goes on to say:

Yet all we heard from Jackson Hole this time were dismissive comments that the emerging market rout is not the Fed’s problem. “Other countries simply have to take that as a reality and adjust to us,” said Dennis Lockhart, the Atlanta Fed chief. Terrence Checki from the New York Fed said “there is no master stroke that will insulate countries from financial spillovers”.

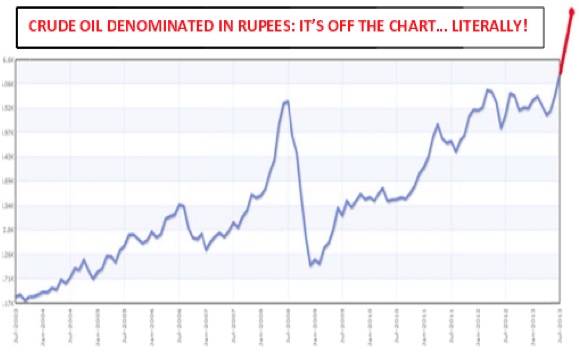

The price of oil in Indian rupees has gone from 1100 to 7800 in the space of 10 years. Think about what a move like that would do to the US economy. (Chart courtesy of Dennis Gartman)

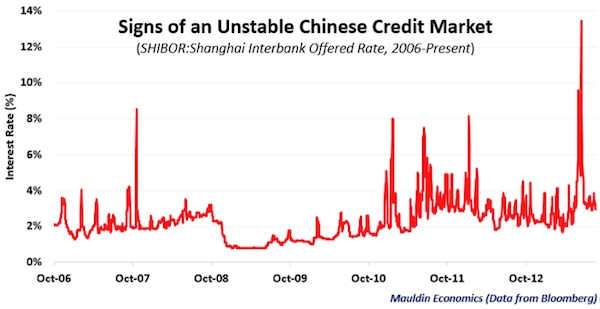

The next chart shows the recent price spike in the Chinese SHIBOR (their short-term interbank rate, more or less equivalent to LIBOR). It is difficult to trust any of the economic data (positive or negative) coming out of China, so we really do not know whether China’s growth story is simply moderating or whether we are seeing a hard landing in progress; but the sudden shock in interbank lending rates is an important sign that all is not well in the Middle Kingdom. The big question: is the recent SHIBOR spike a harbinger of a banking crisis, or does it presage an RMB devaluation? Interbank rates do not spike from 3% to 13% (in about 2.5 weeks) in a healthy economy, and a big event along these lines in China would have enormous implications for global growth.

And while we are on the subject of emerging markets, I have to give you the lead paragraph of the latest note from my good friend and uber-bear Albert Edwards of Societe Generale. It is just too delicious.

The emerging markets “story” has once again been exposed as a pyramid of piffle. The EM edifice has come crashing down as their underlying balance of payments weaknesses have been exposed first by the yen’s slide and then by the threat of Fed tightening. China has flip-flopped from berating Bernanke for too much QE in 2010 to warning about the negative impact of tapering on emerging markets! It is a mystery to me why anyone, apart from the activists that seem to inhabit Western central banks, thinks QE could be the solution to the problems of the global economy. But in temporarily papering over the cracks, they have allowed those cracks to become immeasurably deep crevasses. At the risk of being called a crackpot again, I repeat my forecast of 450 for the S&P, sub-1% US 10 year yields and gold above 10,000.

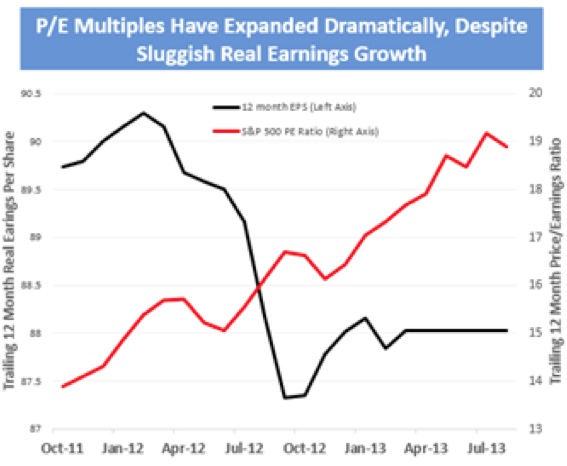

- I have highlighted at length in recent letters (here and here), the significant rise in valuations in this latest stock market rally, which explains a significant portion of the run-up. Here is another chart, which shows that the rise in prices is not being accompanied by a rise in corporate earnings. This situation just screams for a correction. Either corporate earnings have to rise above their already rather significant margins (at least in terms of overall profits to GDP), or the market needs to reflect the lack of earnings growth. That can happen by the market’s either going sideways for a long period of time or dropping in price. Choose your frustration wisely.

- The Fed is telling us they’re going to begin to reduce their purchases of bonds and mortgages. Three academic papers at Jackson Hole, plus the paper that I showed you a couple weeks ago from the San Francisco Federal Reserve, all suggest that QE has not been as helpful as was originally hoped. However, many other respected academics and the market itself disagree. If you are in the latter camp (and believe that QE has given a significant boost to the economy and not just the stock market), you should be very nervous.

The table below shows the revision of second-quarter GDP released Thursday. We should all be happy that growth was revised upward by 85 basis points — 2.5% annualized growth is about as good as we could expect. In fact, this result would argue that tapering should begin sooner rather than later and should proceed faster than most market observers expect. If the economy has recovered that much, it is time to take the foot off the gas pedal.

The problem I want to point out is highlighted in bold, and that is the implicit inflation deflator used by the Fed. Notice that it did not move at all with the revision, even though the economy was seen to grow almost 50% faster. That’s a tad unusual though certainly within the realm of possibility. But if after the massive quantitative easing we have seen, all you can get is 0.7% inflation, that simply illustrates one of my main contentions: we are in an overall deflationary environment. What happens if you then suck the juice from the markets? Will we see a further fall in inflation?

Q2 Advance (7/31) Q2 Revision (8/29)

Real GDP 1.67% 2.52%

Nominal GDP 2.39% 3.25%

Deflator 0.71% 0.71%

Just for fun, the next table gives us the numbers on CPI inflation for the last eight years. Notice that the number moves around a lot.

|

Date |

US Inflation Rate |

|

Jul 1, 2013 |

1.96% |

|

Jan 1, 2013 |

1.59% |

|

Jan 1, 2012 |

2.93% |

|

Jan 1, 2011 |

1.63% |

|

Jan 1, 2010 |

2.63% |

|

Jan 1, 2009 |

0.03% |

|

Jan 1, 2008 |

4.28% |

|

Jan 1, 2007 |

2.08% |

|

Jan 1, 2006 |

3.99% |

|

Jan 1, 2005 |

2.97% |

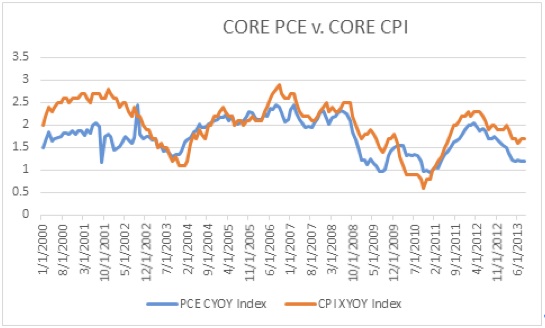

The Fed prefers to use Personal Consumer Expenditures (PCE) as its measure of inflation. For the last 12 months, inflation has been only 1.2% as measured by PCE. Even if you use core CPI, inflation is still rather tame.

Couple tame inflation with the velocity of money’s continuing to fall and you get a deflationary environment. What will happen when the Fed removes QE?

- Given the rise in interest rates of 30-year bonds, real interest rates (interest rates minus inflation) have increased to 2.6% if we use CPE. The long-term average for real interest rates is 2%, which suggests that rates need to come back down, or inflation should rise. You make the call as to which will happen when the Fed begins to reduce QE. This development suggests a rotation back into bonds, which is again another reason not to be thrilled with the equity markets.

- And this is not something I can talk about in specifics, but I follow a number of money managers who use various systems to manage risk. The number of managers who have raised the cash portion of their portfolios to very high levels is significant. These are managers with long-term systematic models designed to keep their emotions out of investment decision-making. Talking with them, they all wish they could raise even more cash.

Yesterday after the markets closed I was invited to a local watering hole here in Dallas to meet with some younger but generally successful hedge fund managers (although younger for me is becoming a relative term). They were all interested in the macro environment, and they were all nervous. What interested me most, though, was not what they wanted to sell; it was what they wanted to buy. They were starting to find value in Saudi Arabia and Turkey and India and Indonesia — stocks of serious companies in those countries had fallen to very low levels. Some were getting on planes to go check things out. And here and there some of the longer-term investors were teasing out opportunities in the US market. For these young Turks, market corrections were not a problem but simply an opportunity to find value.

And I picked up one other key thought from them. You would think, given their view of the world (which I generally share), that they were short a great deal of their book. That is not the case. Today’s environment is a very, very difficult short, because the carry costs are so high. (Definition: Costs incurred as a result of an investment position. These costs can include financial costs, such as the interest costs on bonds, interest expenses on margin accounts, interest on loans used to purchase a security, and economic costs, such as the opportunity costs associated with taking the initial position.)

The Fed has distorted the interest-rate environments both in the US and internationally, and it is simply too costly to put on a short position for very long and be wrong. If you short something, you need to be right fairly quickly, or you will watch your portfolio begin to bleed. For young managers, their track record is critical, so they become quite sensitive to making longer-term macro calls that can go against them for a period of time. They have even more ways to hate the market than I do.

In my August 3rd newsletter (“Can It Get Any Better Than This?“) I shared research supporting our forward-looking prospects for the markets. There was no way to sugar-coat our conclusions: if history is any indication, we are looking at the potential for a significant peak-to-trough drawdown and negative annual returns in equity markets for an extended period of time. We pointed out that where there is danger, there is also opportunity. Investors have a lot to gain from diversifying as broadly as possible and reducing their reliance on equity risk. It therefore makes sense to embrace alternative strategies that are either less correlated or negatively correlated.

Which brings me to a timely webinar, “How Long Can the Bull Run? A Discussion on Long Short/Equity,” that I am hosting on Tuesday, September 10, at 12:00 PM ET / 9:00 AM PT with members of the investment team at Altegris. We will be having a robust discussion on the markets and providing a perspective on the role that a long/short equity strategy can play in a well-diversified portfolio. Altegris has an interesting approach to long/short equity that I’d like you to hear more about. And while the bull market could certainly run longer, we strongly believe that now is a terrific time to diversify away from growth-oriented risk factors that dominate most investors’ portfolios. This webinar is for US-based investors and financial professionals interested in learning more about long/short equity. To receive an invitation, just click on this link and provide some basic information: www.altegris.com/mauldinelsaxreg. After confirmation, you will receive a webinar invitation email from Altegris within the week. Space is limited. A recorded replay will be available to all registrants.

Money For Nothing World Premiere in Dallas, September 6

Let me remind those of you near Dallas that the world premiere of Money for Nothing, the blockbuster documentary on the Federal Reserve, will be Friday, September 6, at 7:30 PM at the AMC theaters in NorthPark Mall in Dallas. You really don’t want to miss this. You can now buy tickets online at the AMC website, and I suggest you do, as I think there is a reasonable chance they will sell out. You can see a trailer by clicking here (select the 8.16.13 entry), or you can arrange for the movie to come to a city near you by going to http://www.moneyfornothingthemovie.org/. I hope you can join me at the world premiere in Dallas. It will be a special evening.

Chicago, Bismarck, Denver, Toronto, and New York

I am in San Antonio as I finish writing this letter, attending the geekfest otherwise known as WorldCon, the science fiction and fantasy book convention. I’ve been reading science fiction for over 50 years, since reading my very first sci-fi thriller in the second grade (Danny Dunn and the Antigravity Paint). Those of us who are sufficiently advanced can remember the Weekly Reader Book Club, which introduced me to all manner of books and opened the world to this country boy. I fell in love with the written word and have remained smitten ever since.

This weekend I will have the privilege of getting to meet and on occasion have dinner with authors who’ve been opening up the universe to me for decades. My good friend and Science Fiction Hall of Fame writer David Brin has been kind enough to introduce me to some of my favorite writers. I’ve been reading L. E. Modesitt for decades. How can Jack McDevitt be 78 years old? The leading science fiction magazines (Clarke’s World, Analog, and Asimov’s) will be hosting events and meetings in my suite with some well-known names, but even more importantly, with up-and-coming writers that I’m really looking forward to meeting. It is a long list of excellent authors who will be in attendance, and I get to play groupie. I know 99% of you are rolling your eyes by now, and the rest of you are consumed by a frenzy of jealousy. I’m sure the talk will focus on how our planet will evolve, and I’m really looking forward to it.

On Tuesday, September 10, in Chicago, I will be joining my longtime friend Steve Blumenthal to present my most recent thoughts on the economy, the Fed, and the direction of interest rates and their impact on the economy and equity markets, at the Trinity Financial Advisors Investor Forum, hosted by John Wimbiscus. The Forum will be held at 6:30 PM at the Gleacher Center of the University of Chicago, located at 450 North Cityfront Plaza Drive, Chicago, IL 60611. Please contact Linda Cianci at linda@cmgwealth.com or call 610-989-9090 x140 to reserve a seat. I hope to see you there.

I will be traveling from there to Bismarck, North Dakota, to delve deeper into the Bakken shale oil boom and to speak for BNC Bank on September 12. My great friend Dr. Lacy Hunt will also be presenting. If you are in the area, you should plan to attend. Then I will be in Denver with my partners at Altegris Investments on September 19 for a presentation to clients and prospects, before flying to Toronto to be with my good friend Louis Gave for a morning seminar on September 23. If you would like to attend, you can register at http://gavekal.com/seminar.cfm or contact Chris Lightbound with any questions. From Toronto I will fly on to New York City for a few days of media and meetings.

I fly back Monday afternoon to spend the rest of the Labor Day weekend with family and friends. But right now I see a little Mexican food on the River Walk in my future. And that may be the most accurate prediction in this letter. Have a great week.

Your getting ready to turn loose his inner geek analyst,

John Mauldin

What's been said:

Discussions found on the web: