Birds, Boats, and Bonds in Venice: The First AAA Government Issue

Dr. Bryan Taylor, Ph.D., Chief Economist, Global Financial Data

When most people think of Venice, they think of the visuals of Venice: the canals, the gondoliers, the paintings by famous artists such as Canaletto or Titian, the Bienniale, or St Mark’s Square (named after the saint whose relics the Venetians stole from Alexandria in 828 by hiding them beneath pork to get them past the Muslim inspectors) and its pestering pigeons.

Birds, Boats and Bonds

When I think of Venice, I think about three things. I think about the first time I went to Europe with my dad. For an entire week before we got to Venice, all I heard about was his insistence on going on a gondola, and passing through the canals while the gondolier sang his Venetian songs. By the time we got to Venice, I was so sick of this that the first thing I did was take him to the place where you hired gondoliers so I would never have to hear about the canal ride again. My dad asked our potential gondolier how much the ride was, and when he found out it was the equivalent of $50 (this was a long time ago), he swore at the gondolier and said he wasn’t wasting $50 on a stupid boat ride. I was ready to kill my dad, but I didn’t cherish the idea of spending the rest of my life in a Venetian prison and having to pass over the Bridge of Sighs.

Since I am an economist, the other two things I think about deal with finance. First, Venice was one of the three city-states in Italy (Florence in 1252, Genoa in 1253, and Venice in 1280) that reintroduced gold into the Italian peninsula eight centuries after the fall of Rome. The other important financial contribution that I associate with Venice are the prestiti: the government bonds Venice began issuing in the 1100s to fund its wars. The prestiti were the first Eurobonds and if Moody’s and S&P had been around in the 1300s, they would have been the first AAA-rated government bonds, though they eventually would have been downgraded.

Prestiti: The First AAA Eurobonds

Venice was the first country to issue government bonds to its citizens in the same way governments currently issue government bonds. Before the Venetian prestiti, and even after, kings, queens, emperors and others borrowed money to fight wars or feed their royal megalomania. When the rulers were unable to pay back the loans, they simply defaulted, often bankrupting their creditors.

Venice was different. Venice was the medieval equivalent of Athens, a democracy for the elites. In 726, the Venetians rebelled against their Roman/Byzantine rulers over the Iconoclast controversy and elected the first of 117 doges before Napoleon conquered the city in 1797. Venice became a city-state, expanding its commercial reach, and became an imperial power, eventually capturing and sacking Constantinople in 1204 during the Fourth Crusade. By the late thirteenth century, Venice was the most prosperous city in all of Europe. At the peak of its power and wealth, it had 36,000 sailors operating 3,300 ships, dominating Mediterranean commerce. Defending their empire meant wars with other Italian city-states, such as Florence and Genoa, and wars meant borrowing money.

Price of Prized Perpetuities

Venice introduced the prestiti in the twelfth century. Subscriptions were obligatory on wealthy citizens in proportion to their wealth, and the elites of Venice found forced loans preferable to outright taxation. In 1262, Venice lost control over Constantinople, and the outstanding loans, which had been considered temporary, were consolidated into one permanent fund called the monte vecchio. This move institutionalized the prestiti as long-term loans rather than short-term borrowings. The prestiti paid a nominal interest rate of 5% on the outstanding capital, two installments of 2.5% paid per annum. After 1377, interest rates were variable, and rates were reduced to 4% in the 1400s. In 1482 a new series of prestiti, the monte nuovo, was issued based upon a new kind of tax and the interest rate was restored to 5%. Another new series, the monte novissimo, was issued in 1509 during the war with the League of Cabrai, and finally the monte sussidio was introduced in 1526.

The prestiti were perpetuities that had no specific maturity date. No physical bonds were issued, but all bonds were registered through the Loan Officers, the Ufficiali degli Prestiti. The claims on these bonds could be sold and transferred to others who then had all the rights of the original purchasers. When possible, the Venetian government repaid the principal. The prestiti became popular forms of investment for Venetian nobles. They were used as endowments for charities, and were used as dowries for daughters upon their marriage.

Since the elites of Venice owned prestiti and were part of the government, this reduced the likelihood the city would default on its debts (though the government did forgo interest payments in 1379-1381, 1463-1479 and 1480). Owning prestiti was a privilege. Foreigners, who trusted the Venetian government more than their own, could only obtain prestiti through an act of the Council of Venice. The prestiti were fully paid off by the government of Venice in the late 1500s.

As with any bond, as the price of the prestiti went down, the yield went up. During a war, the price of prestiti would fall as new bonds were issued and owners faced the risk of delays in payment of principal and interest. During peace time, the price rose as the risk diminished. Since the price of trades in prestiti was a matter of public record, potential purchasers could use these prices to determine the riskiness of their investment. Thus, the prestiti became a barometer of the Venetian Republic. When there was peace, the government would repay outstanding prestiti, sometimes by issuing new prestiti, rolling over old loans into new, but when Venice was at war, the government would issue new prestiti. The prestiti were exempt until 1378 from assessment of new forced loans if held by the original owner, and new assessments were levied largely on real estate.

Venice was successful with the issue of prestiti because the right to transfer the bonds through the Ufficiali degli Prestiti made the bonds liquid and fungible. The Venetian government established a long record of regular payment of interest even when war and disaster threatened the state, assuring investors that they would not lose their money from a royal default. As Venice prospered, confidence in payments rose. The government was under a legal obligation to pay the prestiti, and payment was not left to the whim of the king. During peace time, extra revenues were directed to repayment of the prestiti, rather than setting aside money for the Venetian war chest or expanding services. The government had a deliberate policy of repurchasing prestiti whenever their price fell. In short, the prestiti were the AAA bonds of their day, and as Venice prospered, so did the city and its bondholders.

The Vagaries of War Impact the Prestiti

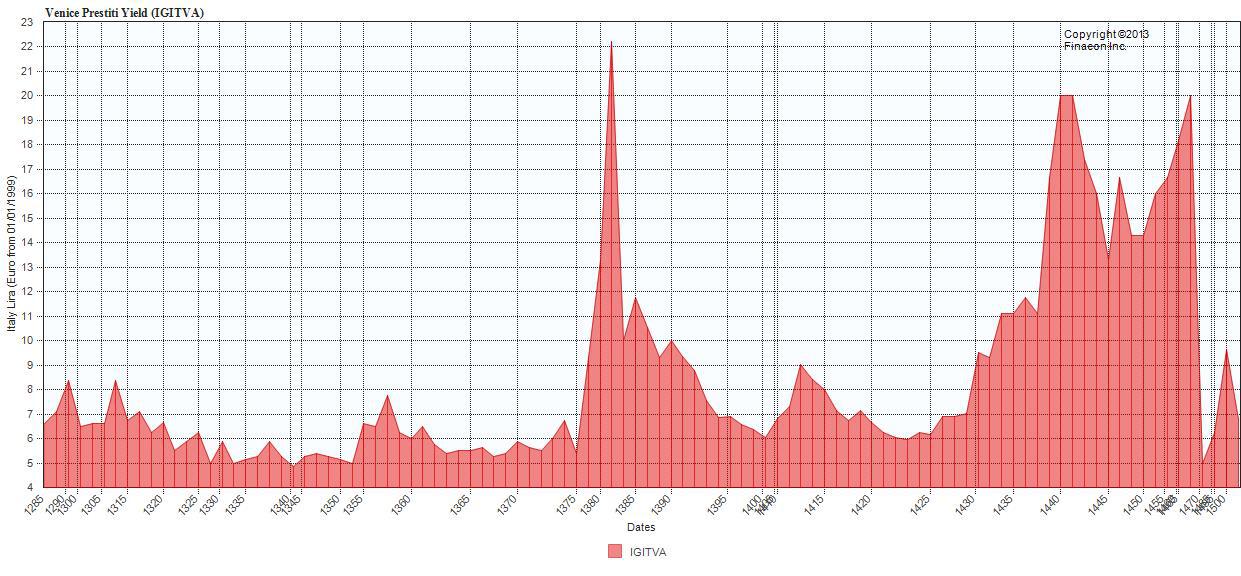

As all nations know, wars do not always go as planned. Sidney Homer, in his History of Interest Rates, provides historical data on the prices of prestiti, and you can see how the price of the bonds and their yield fluctuate in response to the fortunes of Venice. When Venice imposed large assessments, as in 1311-1314, the price of the prestiti fell, and when Venice made large repayments, as in 1344, the price could exceed 100. The worst decline in the fourteenth century came during the War of Chioggia between 1378 and 1381 with Genoa, during which Venice imposed very large assessments, suspended interest payments, made the prestiti no longer immune from tax levies, and expanded the debt 6 to 9 times its level in 1344. The price sank as low as 19 as a result.

After the War of Chioggia ended, the prestiti fought their way back as confidence in the Venetian government returned, causing the price to rise to the 60 level. Unfortunately, the fifteenth century was one of ongoing wars in the Mediterranean. Venetian wars with Hungary in 1412, the Turks in 1416, Milan during the 1420s, and wars with both Florence and Milan in 1450 and the costs associated with these wars reduced confidence in the Venetian government’s ability to fund the prestiti. Emboldened by the fall of Constantinople in 1453, Sultan Mehmet II declared war on Venice, leading to a disastrous and protracted conflict between 1464 and 1479 which drove the price of prestiti back to the 20s. This led to the reissue of new prestiti as monte nuova in 1482.

The graph below shows the yield on the prestiti from 1285 to 1502, assuming a 5% coupon (though in reality the prestiti paid a variable rate after 1377 and 4% during part of the 1400s). The impact of the War of the Chioggia in the 1370s and the wars with Milan and the Turks after 1420 are clearly seen. As the Venetian Republic’s empire shrank, holders of the prestiti suffered. Venetian bonds would definitely have been downgraded as the heavy impact of the Venetian wars had their effect on the city-state’s finances.

Venice never recovered from the devastating war with the Turks, not only because of the loss of its colonies in the Mediterranean, but because Portugal’s discovery of a sea route to India and Christopher Columbus’s discovery of America shifted the locus of economic power from the Mediterranean to the Atlantic. The ocean-faring sailing ships of France, England and the Dutch Republic replaced Venice’s oared galleys. Amsterdam replaced Venice as the financial center of Europe, and during the 1600s and 1700s the East India Company dominated the oceans around Asia the way Venice had dominated the Mediterranean until then. On May 12, 1797, Napoleon Bonaparte brought an end to the Venetian Republic.

Though Venice is no longer a city-state, it has left us a beautiful city which tourists cherish. It also leaves us an important financial legacy: a record of the first international government bonds which were used throughout Medieval Europe by investors who wanted a safe place to store their wealth. Today, U.S. Government Bonds play the same role in the twenty-first century that prestiti played in the fourteenth century. Let’s hope U.S. Government Bonds can continue to pay that role for the century to come.