Good Sunday morning. Here are my early morning reads to round out your weekend:

• Bridgewater’s Ray Dalio Explains the Power of Not Knowing (Institutional Investor)

• Schwab’s Service for Investors Seeking Thrifty Advice Raises Eyebrows (NYT)

• Twilight of GE’s Immelt Era (Bloomberg View)

• Investor Behavior Following Large Gains & Losses (A Wealth of Common Sense) see also Nobody knows anything (The Economist)

• Apple is making an audacious bet with the Apple Watch (Quartz)

• DOA: Wall St. will crush Obama’s plan to protect 401(k) savers (MarketWatch) see also Why Obama’s Recommendations For The Brokerage Industry Are Sensible (Charles Sizemore)

• I Tweet, Therefore I Am (Four Pins)

• How copyright became the best defense against revenge porn (Washington Post) see also Man who made thousands posting women’s stolen nudes goes after news sites that posted pictures of him (Washington Post)

• Outside Man: Scott Budnick produced the Hangover movies. He’s also one of the most effective advocates for prison reform in California. It doesn’t make any sense until you see him at work. (California Sunday)

• Here is the average penis length, according to science (Salon)

What are you reading?

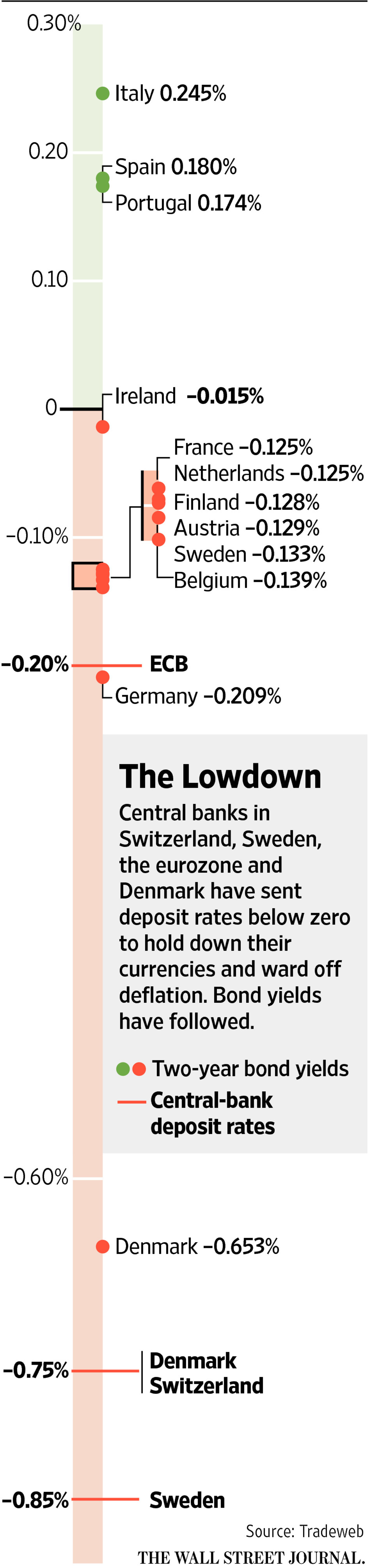

Chart: Negative Interest Rates Test Technology at European Banks

Source: WSJ

Americans Aren’t Saving Enough for Retirement, but One Change Could Help

”…It’s not hard to find evidence of Wall Street’s rapaciousness...”

http://www.nytimes.com/2015/03/04/business/americans-arent-saving-enough-for-retirement-but-one-change-could-help.html

Obama wants to make it the law that financial advisors must be your fiduciary like doctors, lawyers, accountants, etc…

http://time.com/money/3718640/obama-advocates-fiduciary-standard/

Fox says it’s bad

http://fsroundtable.org/fox-business-features-fsr-ceo-pawlenty-obamas-fiduciary-rule/

The Republicans want to stop it.

http://www.investmentnews.com/article/20150225/FREE/150229932/republican-introduces-bill-to-halt-obamas-dol-fiduciary-push

Bogle supporters want THEIR financial manager to get the medal of freedom.

https://petitions.whitehouse.gov/petition/john-c-bogle-should-get-presidential-medal-freedom/tMKz5zyh

So who are you going to trust?

Obama: the guy that told people to invest six years ago at the bottom of the market.

http://thecaucus.blogs.nytimes.com/2009/03/03/obama-says-he-isnt-focused-on-stock-market-gyrations/

http://www.usnews.com/news/obama/articles/2009/03/04/obama-says-buy-stocks-now-good-deals-there-for-long-term-investors

Halved the deficit

http://www.whitehouse.gov/blog/2013/10/30/deficit-more-cut-half-2009

Has five million job openings?

http://www.bls.gov/jlt/

Or the Republican who turned the Clinton Surpluses into TRILLION dollar annual deficits, that said free-market health insurance will wreck the economy and not have job growth? Obama’s policies were bad for the American economy? Obama will not halve the bush deficit? That lied to get us into a war in Iraq and tortured people to ex-poste justify it?

Simple. Go with the facts.

Want to sue Chicago? Asshat whore Attorney Thomas Geoghegan will do it? Why?

“You can’t bring these cases unless you’re right on the law.”

http://www.chicagobusiness.com/article/20150307/ISSUE01/150309816/want-to-sue-the-city-hes-your-guy

What a moron. You can sue anybody, You don’t have to be right. What a tool.

Loser pays legal rulings will get this guy out of our expensive courts and back this asshat back to washing windows on street corners

I sure hope Bush will shut down stem cell research

http://en.wikipedia.org/wiki/Stem_cell_controversy

Concerns About Deflation Show Up in an Obscure Derivatives Market

Something unusual is happening to prices right now: They are falling.

The recent sharp decline in gas prices is part of the story, but there is now growing fear that the Federal Reserve will undershoot its own 2 percent inflation target, hindering the economic recovery. There’s also a small but worrying risk that the economy could enter a deflationary rut.

At issue are inflation expectations. …Beliefs about inflation create a self-fulfilling prophecy in which today’s expected inflation becomes tomorrow’s actual inflation. The trick to managing inflation then, is to manage inflation expectations. In practice, though, it is very hard to observe what people expect inflation to be.

That’s why it’s worth paying close attention to the disturbing portents from a relatively young and obscure derivatives market that provides new perspectives on inflation expectations …

BR, it would be funny if that last link for the story on penis length didn’t actually work, and was just a way to see how many people would click on it!

Happy Sunday!

I don’t get the Quartz article on Apple’s audacious bet. For example, they are equating the iPod with the Sony Walkman market at the time. What Apple was really trying to do was integrate an Internet music buying service with a piece of equipment that could hold the shelf full of music that you were playing on a home stereo while still able to fit into your pocket. The Sony Walkman didn’t fit any of those categories – another example of Sony totally missing the boat on tech’s move into the consumer space.

Apple recognizes that a large percentage of the planet wears a watch. A large percentage of the planet also uses a mobile phone. Putting those two together is a market of billions of people. Apple has to go after markets like this or they will cease to be relevant when somebody else does (think iPhone vs. Blackberry vs. Palm). Their real competitors in this market right now are Timex, Casio, Citizen, Seiko, Swatch etc. If Apple can displace those products on people’s wrists and beat Samsung to the punch, then they have another decade or two to breathe before they have to figure out another billion plus product.

I think Cullen Roche misses the point of the Dow. He takes an academic view that the S&P 500 etc. are more relevant. Technically, he is correct. However, he misses the fact that the DJIA is a trademark owned by a major news agency while S&P 500 etc. are owned by other corporate entities. Dow Jones will make sure that the DJIA headlines their publications because they own it.

If Cullen Roche wants to have a better proxy used across the board, (I think a total US stock market index is really the best thing), then he will need to set up a free index that news agencies can cite without paying licensing fees. He and a bunch of academics can put together the necessary structure so that it can be reported accurately on a second by second basis and distributed widely. Should be easy to do at no cost.

http://www.pragcap.com/is-it-time-to-dump-the-dow

Because of the disproportionate impact of losses in relation to the gains required to recover losses and overcome the impact of the “fees”, it would seem that one of the more brilliant moves that one could make and put favorable probablities in one’s favor, would be to not run a hedge fund or invest in one at all ! In these articles, why not have interviews with investors that resisted the impulse in investing in them. That would provide a much more valuable lesson in self control and wisdom than interviewing these “geniuses”. …

There are a lot of interviews with Warren Buffet out there

Warren Buffett wants to raise tax on hard working American families. He must be destroyed.

Saturday, Mar 7, 2015

The myth destroying America: Why social mobility is beyond ordinary people’s control

Americans overwhelmingly believe they control their financial destinies, but a huge body of research says otherwise

Sean McElwee

In America, there is a strongly held conviction that with hard work, anyone can make it into the middle class. Pew recently found that Americans are far more likely than people in other countries to believe that work determines success, as opposed to other factors beyond an individual’s control. But this positivity comes with a negative side — a tendency to pathologize those living in poverty. Indeed, 60 percent of Americans (compared with 26 percent of Europeans) say that the poor are lazy, and only 29 percent say those living in poverty are trapped in poverty by factors beyond their control (compared with 60 percent of Europeans).

Such beliefs are just that: beliefs. While a majority of Americans might think that hard work determines success and that it should be relatively simple business to climb and remain out of poverty, the reality is that the United States has a relatively entrenched upper class, but precarious, ever-shifting lower and middle classes. While many Americans might hate welfare, the data suggest they are fairly likely to fall into it at one point or another.

In their recent book, “Chasing the American Dream,” sociologists Mark Robert Rank, Thomas Hirschl and Kirk Foster argue that the American experience is more fluid than both liberals and conservatives believe. Using Panel Survey of Income Dynamics (PSID) data — which has tracked 5,000 households (18,000 individuals) from 1968 and 2010 — they show that many Americans have temporary bouts of affluence (defined as eight times the poverty line), but also temporary bouts of poverty, unemployment and welfare use. (The study includes food stamps, Medicaid, Temporary Assistance to Needy Families/Aid to Families with Dependent Children, Supplemental Security Income and any other cash/in-kind program that relies on income level to qualify.) The researchers conclude that a large number of Americans eventually fall into one of these categories, but that very few Americans stay for long. Instead, the social safety net catches them, and they get back on their feet.

…

http://www.salon.com/2015/03/07/the_myth_destroying_america_why_social_mobility_is_beyond_ordinary_peoples_control/

Here’s What Happens When You Install the Top 10 Download.com Apps

http://www.howtogeek.com/198622/heres-what-happens-when-you-install-the-top-10-download.com-apps/

Re: Schwab’s roboadvisor

Much of the piece seems to focus on their recommendation of cash in portfolios. While many financial advisors don’t recommend cash that doesn’t mean it is not a valid approach. Here is an interesting piece looking at using cash instead of bonds in a portfolio, especially if the portfolio is in a rising interest rate environment: http://awealthofcommonsense.com/an-alternative-to-the-6040-portfolio/

I find it a bit of a stretch to think Schwab is recommending cash in the portfolio just so they can have slightly higher bank deposits. They would probably make more money from a bond ETF that they run.

Something the piece doesn’t look into much is the relative makeup of the portfolios with a mutual fund vs ETF structure. My guess is that they will find that the mutual funds in the Schwab Target Date funds tend to hold significantly more cash than the equivalent ETFs in the robo-advisor portfolio due to the differences in the nature of the funds. That by itself could be much of the difference in the cash percentage of the portfolio.

The biggest issue that I have had with the Schwab Target Date funds is their expense ratio. While not up to the usual high fee standards of Wall Street and the insurance industry, they are still up in the 0.7% range, which I think is too high.

Given all of the numerous high fees and conflicts of interest, I find it interesting that the criticism is focusing on a free service that will result in relatively low expenses (less than 0.5%) for a diversified portfolio. If the entire industry was this rapacious, almost every American investor would be far better off financially today.

The NYT wants the Fed to stay put except to stop bubbles.

http://mobile.nytimes.com/2015/03/07/opinion/jobs-and-the-federal-reserve.html

Rates are at zero to 0.25%. Are they saying if we went to 25 basis points flat and said they will keep raising only if data warrants that the economy would losrle momentum? C’mon.

Florida Officials Say They Were Banned From Saying ‘Climate Change’ and ‘Global Warming’

But you can say Tittie Bars!

http://www.bloomberg.com/politics/articles/2015-03-08/florida-officials-say-they-were-banned-from-saying-climate-change-and-global-warming-

It will be a real scream when the whole state is waist deep in sea water and they’re all screaming how it’s Obama’s fault.w

@rd, I had a similar reaction — the overall expenses with Schwab looked to be in the 0.3% range, definitely not rapacious.

However, it seems like they may have been too clever by half, in that they advertise “free”, but then it turns out that if you read the fine print, it is probably more like 0.3%-ish.

Once again, it may be that it isn’t the crime, it’s the coverup. To re-purpose Shakespeare a little — first we kill all the lawyers, next we kill all the marketing people. As a marketing person myself, sometimes I think that might be well-deserved ;-)

I think they mean free in the same way that Vanguard and T Rowe Price mean “free” with their “all-in-one” funds in that the only fees are the underlying asset expenses while the expertise for asset allocation is a “free” service unlike external advisors who would superimpose a fee. I thought Schwab was pretty clear on outlining the types of expenses that would be built in.