We are wrapping up a long and productive (and fun) week on the West Coast, where we ate our way from Napa to SF to Cupertino and back. (Better order that seatbelt extender). The last of our West Coast morning reads:

• A Dozen Things Taught by Warren Buffett in his 50th Anniversary Letter that will Benefit Ordinary Investors (25iq)

• How Pimco Lost its Mojo (Bloomberg View)

• Male Investors vs. Female Investors: Studies show men and women could learn from the other’s approach (WSJ)

• What Big Companies Get Wrong About Innovation Metrics (Harvard Business Review)

• College Majors Figure Big in Earnings (WSJ) see also Getting Rich in America Depends on a Lot More Than a College Degree (Bloomberg)

• Why Elizabeth Warren Makes Bankers So Uneasy, and So Quiet (Bloomberg)

• FiveThirtyEight Dissects The Deflategate Report (FiveThirtyEight)

• Meet the outsider who accidentally solved chronic homelessness (Washington Post)

• Big and Weird: The Architectural Genius of Bjarke Ingels and Thomas Heatherwick The next Googleplex goes way beyond free snacks and massages. It’s a future-proof microclimate (Businessweek) see also Why Google’s Hometown Said “No” to a Massive New Googleplex (Slate)

• This is the first news article ever written about Apple (Business Insider)

What are you reading?

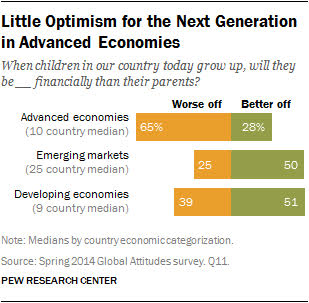

Little Optimism for the Next Generation in Advanced Economies

Source: Pew Research

A very good piece on Experience vs. Expertise. http://awealthofcommonsense.com/experience-or-expertise/

I am an engineer with a fair amount of experience and expertise, so I have an additional comment to add to his piece. In engineering we use predictive models all the time. However, the world is a very non-linear place, so many of our factors have to be derived empirically and it is very important to know which models apply to which situations and conditions.

When I review a detailed predictive model study, I focus my questions on the experience of the modeling team and the empirical data set used in the model to validate if it is the appropriate model and if it is being applied correctly with an adequate data set.

On the other hand, when I am in the field and working with the investigation or construction teams, I focus my questions on whether or not predictive models were used for developing the study or design, to see if I get the response “We did it this way on a different site and it worked, so we are assuming it will work on this one.” This past experience is sometimes valid, but often is not as the sites may be wildly different.

So predictive expertise should be used to apply a theoretical framework to which the practical experience can then be applied to address those empirical factors and complexities for which we have no models at this time.

Junior staff come out of school raring to apply models but frequently find out that the world is much messier than their textbooks implied. The gray hairs then help with the real-world application of the new tools that the young engineers have learned.

Nike to create 10,000 U.S. jobs if Obama trade deal gets OK

http://money.cnn.com/2015/05/08/news/nike-jobs-obama-trade/

If they want it, they better stop calling it “Obama’s Trade Deal” or the GOP will concoct another completely phony outrage and vote it down along with a new impeachment, canceling of all payments on ACA invoices, and convince their flock that Nancy Pelosi and Harry Reid are to blame

Hey it turns out Tom Brady was a softball player

http://www.nbcnews.com/news/sports/tom-sucks-report-reveals-damning-deflate-gate-text-messages-n354816

Wonder how he will do when he is forced to play football?

April jobs report: much better, but an alarm on leading indicators

The best news in the report, beyond the headline numbers, was the positive movement in the underemployment statistics: …

But …The manufacturing workweek was down. Overtime was down. Unemployment from zero to 5 weeks increased significantly. Revisions to prior months were negative. This is the third month of this negative trend in the leading indicators in the employment report.

It appears that the financial industry has not quite figured out that the millenials that have grown up with Amazon for shopping, iTunes for music, and smartphones for communicating are unlikely to focus on paying front-end loads to brick-and-mortar advisors. This is also a generation that has the full suite of Roth and regular IRAs and 401ks available to them. As a dad, I have pointing my kids to saving a bunch of cash for emergency funds and then simple Target Date Roth IRAs as well as getting their company matches in their 401ks. They won’t need advisors for those items for at least a couple of decades as the entire objective is to do nothing other than put money in each year. Getting them in the habit of tweaking their allocations based on market conditions would just teach them bad behavior.

Some of the comments are from a Schwab person. One thing that has baffled me is why Schwab’s Target Date funds pretty much only use active funds. I have been surprised that they haven’t done a Target Date mutual fund series using a combination of Schwab index and fundamental funds which would be a different value-oriented twist compared to the Vanguard Target Date funds. They could also do a similar series parallel to the Vanguard Lifestrategy funds. Instead they have focused on the robo-advisor concept with a very complex set of ETFs.

http://www.marketwatch.com/story/fund-industry-says-its-struggling-to-reach-millennials-2015-05-07

could be they dont believe that the money will be there when they will retire? after if the government cannt be trusted to fund SS, why should they trust finance to do any better?

I think there are other reasons:

1. Many of their employers view them as disposable and want them as temps or independent contractors without access to 401k.

2. Most financial firms want $1,000 or higher initial minimum investments. One of my kids went with a T Rowe Price Target Date in 2008 simply because they had no initial minimum if you had a $50/month auto-deduct (now I think it is $100). That account is now worth over $20k. Its a decent diversified fund with reasonable costs (not as low as Vanguard, but less than the employer’s 403b fund) and a good track record.

3. The info sent to my kids by the various fund companies for their 401ks is nice-looking, glossy, and almost useless for real planning. The salesmen that they send in generally are looking for people to sell insurance and other financial products to (single 26 year olds without kids don’t need much insurance). So I end up interpreting the stuff for them, sifting through their options to show the hidden costs, and generally end up just recommending the Target Date fund in their plan which is usually one of the lowest cost options in their plan. It also means that they don’t have to learn much about the markets in the near-future as the whole objective is for them to simply save and do nothing with their accounts for the next 20-30 years.

4. The US retirement fund system is an accidental smorgasbord of gibberish names based on tax code provisions. IRAs, Roth IRAs, rollover IRAs, inherited IRAs, 401ks, Roth 401ks, 403bs, Roth 403bs, ESOPs all embedded within a complex personal income tax code with lots of different tax rates, deductions, and credits. One of the main things I have done with my kids is to try to simplify the stack of crap put in front of them down to a handful of key points regarding different types of tax-sheltered savings and the basics of asset allocation. Once they understand those, then they tend to make excellent decisions. Before that, they were just frustrated and were just as likely to do nothing. Some of the people in my office have told me the same thing. The financial sector is selling complexity and obfuscation while the millenial consumers are looking for efficient simplicity – a complete disconnect.

5. However, they are very loyal to the companies that they find that are focused on good products with good communication and good ethics. So far both Vanguard and T Rowe Price have been building up loyalty with my kids. An insurance firm is a 403b provider for one of them and their offerings will get rolled over into another firm if they leave that employer as they have not been earning the trust – however a 6% employer match is just too good to pass up, so you put up with so-so products and higher costs.

Millennials respect brick-and-mortar advisers who can apply their experience and expertise to their concerns.

will jobs continue to exist for most much longer? hard to tell

http://www.ibtimes.com/jobs-unemployment-will-robots-algorithms-permanently-replace-humans-labor-force-1913082

but the next 15 years will tell us that

BLS estimates

http://www.bls.gov/opub/mlr/2013/article/occupational-employment-projections-to-2022.htm

I thought baby boomers refusing to retire – were permanently replacing the labor force…

Not to mention the very real potential to eliminate most, if not all, driving jobs in the next 10-20 years. I seem to recall that driving (in all its varied forms) is generally the number one job numerically in just about every state. That includes truck driver, Uber driver, taxi driver, bus driver, train driver, etc.

So why does the BLS fail to include DRIVING as an at-risk industry?

There are going to be an awful lot of unemployed people in the future. Even part-time jobs (as all the job gains in this months report apparently were) are not going to be around to fill the gaps. The only solution is to reduce birth rates significantly or open up wormholes to ship the many unemployed to other places in the universe.