Still a Lot of Negativity on Housing

Maybe the millennials will fix things.

Bloomberg, August 24, 2016

There has been a steady drumbeat of negativity about housing ever since the residential real-estate market crashed. While there are somesigns of recovery, psychological damage persists.

It has been a few years since we last looked at this issue, so we’re overdue for a revisit.

Everyone has to live somewhere, and where and in what kind of housing you choose is crucial to your quality of life, your kids’ education and your ability to save for retirement. And because so many resources are devoted to sheltering the 320 million-plus Americans, the industry makes up a significant part of the economy.

Before we go further, I am not advocating an expansion of home ownership as a government policy. But I will say this: given the state of the economy, housing prices and historically low interest rates, many people should buy a home.

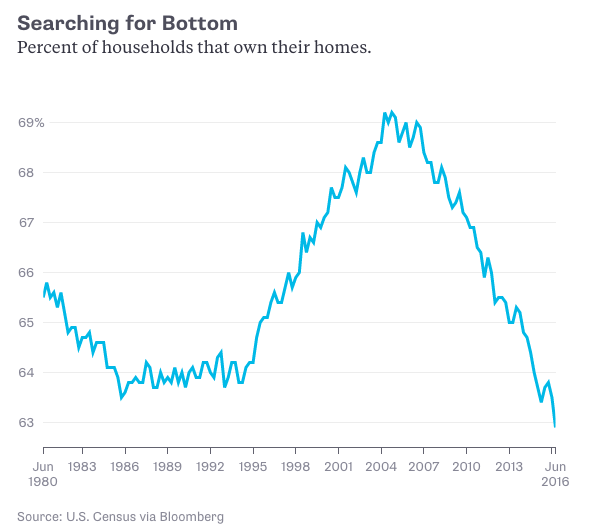

A little history: The post-World War II suburbanization of America, along with car culture and housing envy, helped to drive home ownership rates to a postwar peak of 65.8 percent in the late 1970s and early 1980s. That seemed like a reasonable balance between renters and owners, relative to factors such as employment, credit availability and the scale of the housing stock.

Following that peak, a severe recession and sky-high mortgage interest caused ownership rates to fall to about 64 percent; ownership rates wouldn’t pass their previous high until 1997. As the economy took off during the 1990s tech boom and the Federal Reserve continued lowering interest rates as inflation abated, home ownership surged. Then, after the dot-com bust, the Fed under Alan Greenspan lowered rates even more. That, along with lax lending standards and a public wariness of investing in the stock market, helped to kick off a real-estate driven economic expansion.

Millions of people who had been renters suddenly were able to obtain mortgages. As the chart below shows, home ownership rates skyrocketed to more than 69 percent.

That was then. Ownership rates have since fallen to a level last seen in the mid-1960s, even amid some of the lowest mortgage rates ever and a slew of government initiatives designed to make owning a home more affordable. So this suggests that the housing market still has room to rebound.

There are, of course, lots of good reasons to rent: you have more geographic mobility, minimal long-term financial commitment and fixing a leaky pipe is someone else’s headache.

However, at some point in life, you probably no longer want to have a landlord telling you what color your walls can be or become tired of having strangers share a wall with you. I am not a zealous believer that everyone should go out and buy a home. However, for many people, buying makes sense — especially with mortgage rates as low as they are (the current rate of about 3.45 percent for a 30-year fixed-rate mortgage is just 0.10 percent higher than the record low).

There are lots of other reasons to buy, based on whether someone plans to live in the same area for five years or more, wants or needs a tax deduction, is concerned about the quality of local schools or simply wants the greater social stability that ownership tends to confer.

Obviously, not everyone or every time is suitable for buying.

However, home ownership still seems to be out of favor. I have blamed the recency effect for this in the past, but as home ownership rates continue falling, it make me wonder if what was once the American Dream has given way to a cultural shift in attitudes toward housing.

Whether that is on the verge of changing anytime soon will likely be determined by how soon the millennials move out of their parents’ basements, form households and start having kids. If that happens, that should bode well for the housing market.

Originally: Still a Lot of Negativity on Housing

What's been said:

Discussions found on the web: