Millennials Leave the Basement to Buy Homes

This points to a rise in spending on furniture, appliances, electronics and cars that will lift earnings and power stocks.

Bloomberg, November 10, 2017

A few years ago, I wrote “The economy will one day improve, and the millennials will move out of their parents’ basements. When that happens, expect to see homeownership rates move back higher.”

That day has arrived. Millennials are forming new households, 1 moving to the suburbs, buying furnishings and SUVs. According to Zillow Group data, people aged 18 to 34 have become the largest group of homebuyers in the U.S.

This wasn’t the case just a few years ago, when the Pew Research Center did an analysis of U.S. Census Bureau data. It found that in 2012, “36% of the nation’s young adults ages 18 to 31 were living in their parents’ home. This is the highest share in at least four decades.”

The reversal of this phenomenon is an important contributor to the momentum behind the economic recovery from the credit crisis; it also is potentially significant for the next leg up in U.S. equity markets.

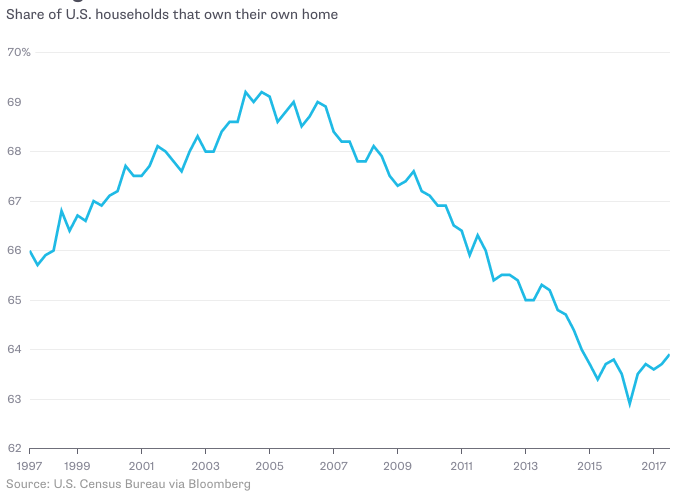

Have a look at the chart below showing homeownership rates. 2 It shows that the percentage of Americans who owned their own homes peaked in 2004. That was, not surprisingly, about the high point of the credit bubble.

Coming Off the Bottom

Before the financial crisis, the basis for credit and lending was the borrower’s ability to service the loan. Job history, credit score, income and other debt all figured into any lending decision, especially for mortgages. From 2002 to 2007, the basis of that credit decision shifted to the lenders’ ability to sell the mortgage to a third-party securitizer. That is why so many nonbank lenders were offering loans without the standard documentation, sometimes referred to as no-doc or liar loans. My favorite description of these buyers was “renters with an option to default” — and as we saw in the financial crisis, millions of them were unable to repay their loans.

Amid a flood of easy credit, home sales peaked in volume in 2005 and prices in 2006. Once the crisis hit, foreclosures soared and prices fell 30 percent or more nationwide, though some areas such as South Florida, California, Nevada and Arizona fared much worse. This ultimately led to broad tightening of lending standards, along with doubts about the value of owning a home and a decade-long decline in ownership rates.

We have now seen that pattern reverse during the past year or so. Homeownership bottomed in mid-2016, and has gained a full percentage point since then. If this were a stock, you would say the trend has been broken.

Several forces play a part here:

No. 1 Rising rents: As they go higher, the calculus of buying versus renting tilts more toward ownership than being a tenant

No. 2 Strengthening economy: Increasing job creation and faster wage growth makes ownership and the attendant mortgage-interest tax deduction more attractive

No. 3 Household formation: The decline that followed the credit crisis is ending and millennials are vacating their parents’ basements, moving in together, getting married. The next step, along with having children, often is buying a home;

No. 4 Passage of time: As the credit crisis recedes from memory, fear of making large financial commitments is in decline.

People like to debate why residential real estate has a special place in the U.S. tax code. There are two main reasons: ownership brings with it obligations, including commitment to neighborhoods, local schools and good municipal government. The other is that owners stimulate the economy more than renters.

While we can debate exactly how true the first point is, there is no debate about the second: Owners tend to improve their properties — they buy more furniture and appliances; put in new kitchens and bathrooms; own more cars; spend more on landscaping. This consumption results in higher revenue and profits for corporations, and it eventually works its way into higher stock prices.

All of this should figure in any debate about reducing or eliminating the mortgage deduction. Although there may be some sound grounds for cutting or ending this tax break, it should be balanced against the harm its elimination might do as an incentive for homeownership. The housing market is still recovering. Let’s hope no one does anything foolish at this time to disrupt it.

__________

1. Household formation –people living together or getting married — tends to precede home purchases. For this reason, I find it worthwhile to follow Federal Reserve (and other) research on household formation such as this, this, this, and this.

2.Some people, including Jed Kolko, chief economist and vice president for analytics at Trulia find fault with this metric. I don’t.

Originally: Millennials Leave the Basement to Buy Homes