Are we heading into a recession? According to quite a few observers, this is almost no longer a question, but rather seems to be a fait accompli.

I am skeptical, but others are much less so. Here is the usually sober Planet Money:

“So, are we heading into a recession? Darkening animal spirits — or bad vibes — suggest we may be. Fed policy suggests likewise. Ditto continued turbulence with COVID, and sky-high oil prices. In short, despite low unemployment, continued job growth, and other signs of economic health, there are warning signs flashing that a recession is coming, if it isn’t already here.” (emphasis added)

As a reminder, the official NBER’s definition states “a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months.” Specifically, the criteria include “depth, diffusion, and duration” — none of which is present today.

Given the economic data, it is startling (if not foolish) to state we are in a recession right now. As noted, “low unemployment, continued job growth, and other signs of economic health” make that timing moot. Second, because the economy is cyclical, it means a recession is always coming. (It’s called a “Business Cycle” for a reason).

The key issue is timing. Is a recession imminent?

I think not. Not in this quarter, or the third quarter. I am doubtful even the fourth quarter of 2022 (possible, but improbable).

Why? Because most of the leading indicia of economic contractions are not present today. Inflation remains a concern, and the biggest warning sign is the stock market: Year to date, the S&P 500 is off 13.3% and fell nearly 20% from its all-time highs. But neither of those are determinative. As my colleague Ben Carlson points out, bear markets can occur outside of a recession, and “they tend to be shallower and less lengthy while recessionary bears are greater in both.”

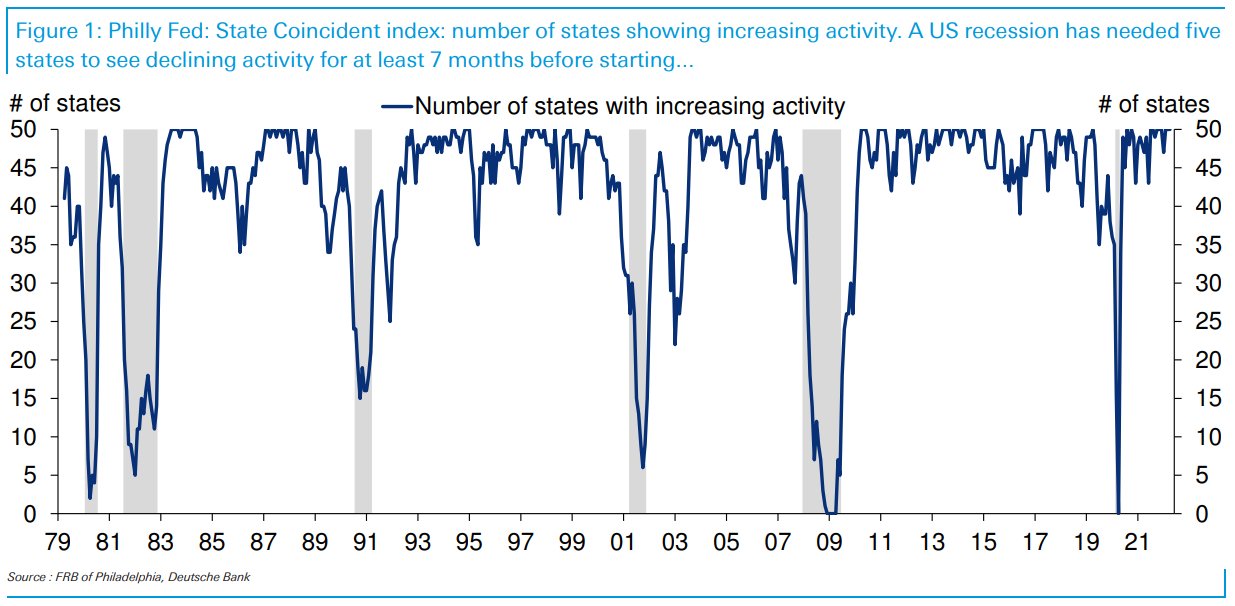

Instead, consider the chart above, via Matt Luzzetti of Deutsche Bank. It shows the Federal Reserve Bank of Philadelphia’s monthly State Coincident Indexes. I cherry-picked this chart because of its good historical track record of showing a drop before recessions, and because by its nature, it includes diffusion (50 states) and duration (time series) — that is 2 of the 3 NBER contraction factors.

When we do a “Compare & Contrast” of 2022 with each of the 6 prior recessions going back 43 years to 1979, we see none of the early signs of contractions in any of the 50 states. This data series has shown an early warning that recessions were increasingly probable. But the state-by-state slowings took several quarters or even years to develop. Instead of 50 states showing expansion, before recessions, that dropped to 45, 40, then 35 before the recession began (and the number of expanding states fell to 10, 5, or 0).

The current monthly coincident state index shows all 50 states economically expanded. That not only makes it impossible for us to be in a recession today but also makes it highly unlikely we will be in a recession anytime soon.

See also:

The 2 Types of Bear Markets (Wealth of Common Sense, May 23, 2022)

Previously:

Economic + Market Scenarios (May 23, 2022)

The Post-Normal Economy (January 7, 2022)

The Great Reset (June 2, 2021)