This weekend’s cover story in Barron’s was devoted to the impact of this year’s presidential election on investors. New policies on income taxes, spending, capital gains and trade issues — plus the current and future Supreme Court openings — all weigh heavily on the minds of the people who put capital at risk.

Barron’s conclusion is that Democrat “Hillary Clinton is the more investor-friendly of the two” major party’s frontrunners, the other being Republican Donald Trump.

Here is a corollary conclusion: the hand-wringing of the investor class is wildly overdone.

Why is that? If you have read this column before, you probably are familiar with my views: Investors don’t know what the future holds and cannot know in advance all of the complex machinations that follow any sort of major political event. Even if they could know, it likely won’t matter, at least it won’t in the short run.

For that reason, which candidate ultimately becomes president is much less consequential to your portfolio than you have been led to believe.

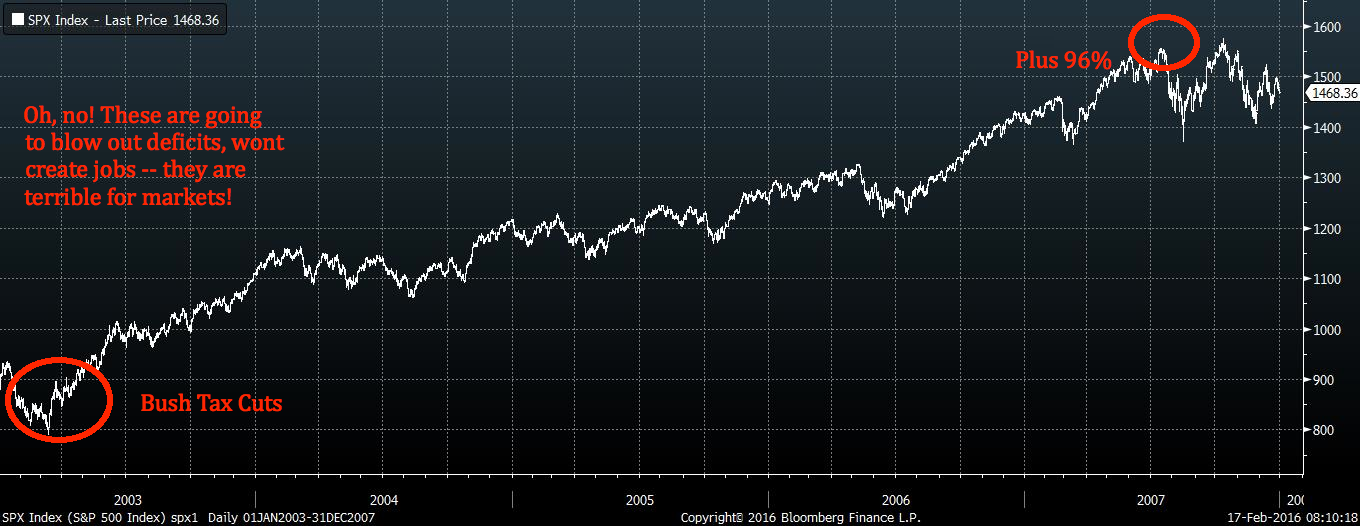

Recall as we noted last month that a substantial number of Americans, including some investors, believe that President Barack Obama is a Muslim, Kenyan-born socialist who was going to destroy the U.S. and take the stock market with it. Meanwhile, the Dow Jones Industrial Average almost tripled during his first six years in office (though it has fallen about 7 percent from its 2015 high). Before Obama, other voters expected that George W. Bush was going to blow out the deficit and kill employment. Instead, the market almost doubled from 2003 to 2007 (before collapsing in a disastrous financial crisis the next year).

{kind=link}

{kind=link}

Barron’s is less skeptical than I am about the immediate impact of any presidential candidate. The presumption is that whoever is elected will have a significant and immediate affect on both the economy and the markets.

I have argued against this kind of analysis: markets and the economy determine which candidate does well, and not the reverse. Strong economies, with good job creation and wage gains, tend to help incumbent candidates and parties. Whoever gets elected can certainly change market cycles, but that occurs over time and around the edges. Presidents get too much credit for good economies and markets, and too much blame for bad.

Regardless, Barron’s makes the argument that Clinton would be fairly predictable, be more accommodating than Obama and be more willing to compromise. They find her “moderate political instincts and left-center policy goals suggest a president who wouldn’t stand in the way of the financial markets.”

Further, the weekly investment newspaper argues that Clinton is “a knowledgeable Washington player, she might even be able to strike a bargain with House Speaker Paul Ryan and Senate leaders on tax reform.”

That’s all well and good, but I would imagine that to be true of whoever succeeds Obama. It is as much a function of Congress and the economic circumstances of the moment as it is a matter of who occupies the Oval Office.

But Barron’s couldn’t quite commit and engaged in some furious backpedaling. One must be at least slightly bemused by Barron’s non-endorsement statement:

Make no mistake. We are not endorsing Hillary Clinton for president of the United States. Nor are we saying that she would be the best president for investors from among the current crop of candidates. We are simply weighing the impact of a President Clinton on the financial markets, based on her stated positions and past actions, against those of her most likely rival, Donald Trump.

Regardless, the question isn’t whether Republicans will vote for Clinton, or even whether she will win; the question is, would it even matter that much?

Originally: Picking the Best Presidential Candidate for Markets