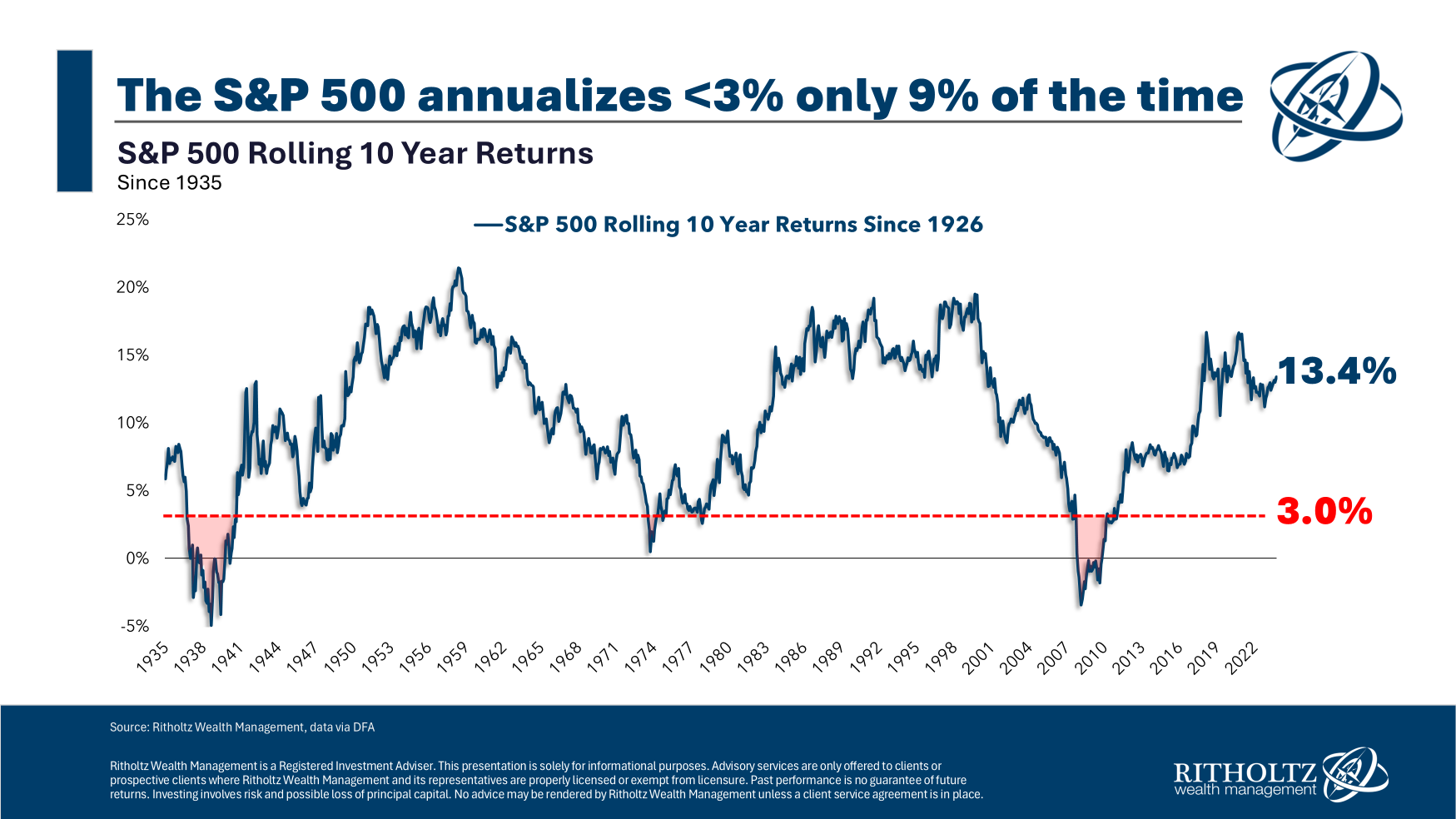

What do the Great Depression, the Great Financial Crisis, the Stagflationary 1970s, and the upcoming 10-years have in...

What do the Great Depression, the Great Financial Crisis, the Stagflationary 1970s, and the upcoming 10-years have in...

Read More

Why Stocks Are Your Best Bet with Jeremy Schwartz, WisdomTree (September 25, 2024) Are equities the best long-term investment? If...

Read More

The transcript from this week’s, MiB: Mike Wilson, Morgan Stanley, is below. You can stream and download our full...

Read More

This week, we speak with ith Mike Wilson, Chief Investment Officer and Chief US Equity Strategist at Morgan...

Read More

I have known Josh for nearly 15 years. Despite his writing in public that entire time, hosting two weekly shows on our YouTube channel,...

I have known Josh for nearly 15 years. Despite his writing in public that entire time, hosting two weekly shows on our YouTube channel,...

Read More

The transcript from this week’s, MiB: Heather Brilliant, Diamond Hill, is below. You can stream and download our full...

Read More

This week, we speak with Heather Brilliant,, chief executive officer of publicly traded Diamond Hill Investment...

Read More

Why Fees Really Matter with Eric Balchunas, Bloomberg Intelligence (August 28, 2024) Fees matter more than you think. Over...

Read More

My keynote at the Greater Kansas City FPA Symposium 2024 is above. They are a great group of people, and very motivated to serve...

My keynote at the Greater Kansas City FPA Symposium 2024 is above. They are a great group of people, and very motivated to serve...

Read More

At the Money: Investing With Personal Values with Ari Rosenbaum, O’Shaughnessy Asset Management (Nov 1, 2023) The term...

Read More