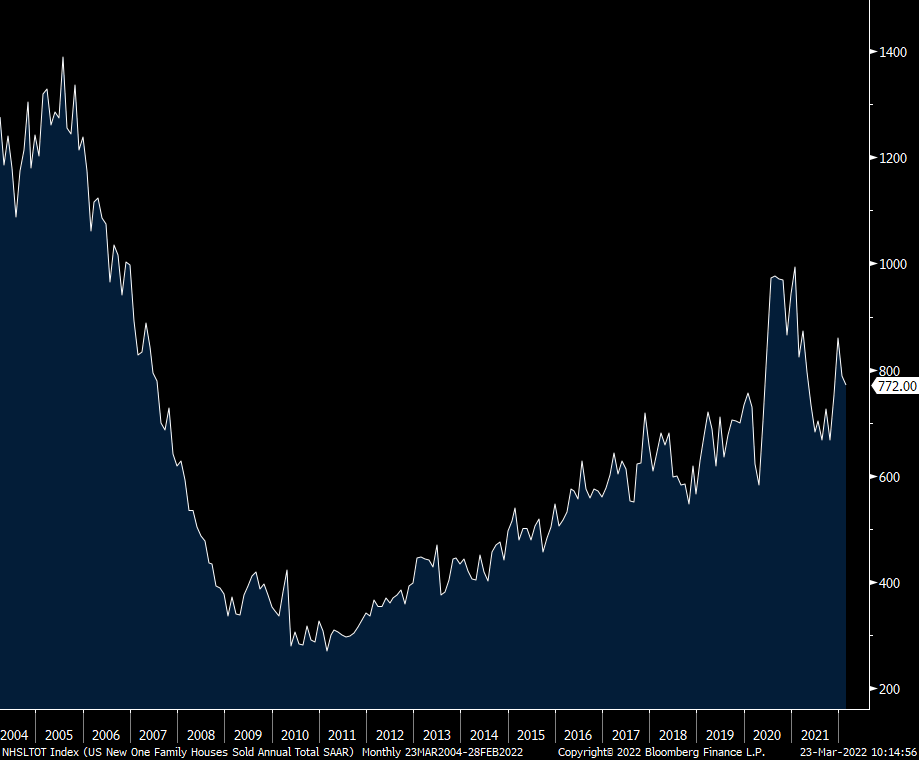

New home sales in February totaled 772k, 38k less than expected and January was revised down by 13k to 788k. Keep in mind that the...

New home sales in February totaled 772k, 38k less than expected and January was revised down by 13k to 788k. Keep in mind that the...

Read More

Peter Boockvar is the CIO of Bleakley Advisory Group and Editor of The Boock Report. So Powell was asked...

Peter Boockvar is the CIO of Bleakley Advisory Group and Editor of The Boock Report. So Powell was asked...

Read More

Peter Boockvar is the CIO of Bleakley Advisory Group and Editor of The Boock Report. ~~~ Before I get into the details of the bill, I...

Peter Boockvar is the CIO of Bleakley Advisory Group and Editor of The Boock Report. ~~~ Before I get into the details of the bill, I...

Read More

Peter is the CIO of Bookmark Advisors, an asset management firm and the Editor of The Boock Report, a macro economic and market...

Read More

Peter Boockvar is the CIO of Bleakley Advisory Group and Editor of The Boock Report. ~~~ After listening to the Home Depot conference,...

Read More

Peter is the CIO of Bookmark Advisors, an asset management firm and the Editor of The Boock Report, a macro economic and market...

Peter is the CIO of Bookmark Advisors, an asset management firm and the Editor of The Boock Report, a macro economic and market...

Read More

Note: Following my recent debate on stock valuations, I thought this discussion about a foodstuffs, the CRB food index and other...

Note: Following my recent debate on stock valuations, I thought this discussion about a foodstuffs, the CRB food index and other...

Read More

With all due respect to the office of the President, I can’t think of many other bigger wastes of my time than watching the State...

Read More

“Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” You likely...

Read More

Succinct Summation of Week’s Events: Positives: 1) Within the payroll data, average hourly earnings rose by .3% m/o/m, in line with...

Read More