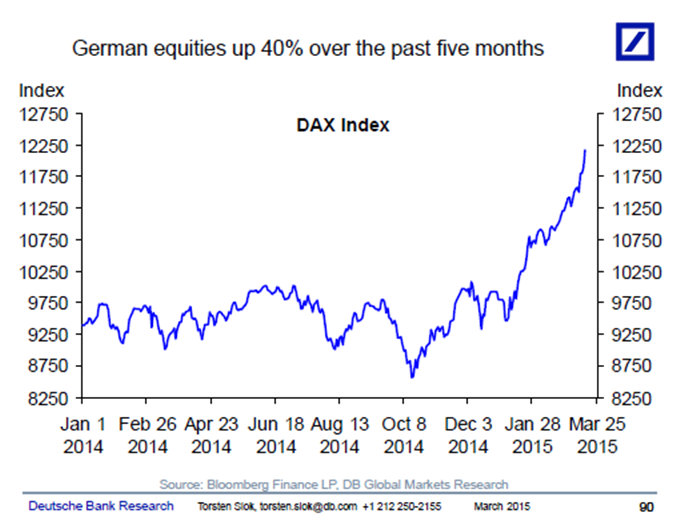

German stocks have increased 40% over the past five months. Combined with the euro depreciation and lower oil prices it all points to more upside risk to the economic outlook for Europe.

Source: Torsten Sløk, Deutsche Bank Research

German stocks have increased 40% over the past five months. Combined with the euro depreciation and lower oil prices it all points to more upside risk to the economic outlook for Europe.

Source: Torsten Sløk, Deutsche Bank Research

1. “Combined with the euro depreciation and lower oil prices it all points to more upside risk to the economic outlook for Europe.” – Doesn’t 25% fall in Euro negate more than half of the price drop in Brent? If oil price drop in this equation is “plus”, then the FX rate should be a “minus”

2. “German stocks have increased 40%…Combined with the euro depreciation and lower oil prices it all points to more upside risk to the economic outlook for Europe.” – Stock prices point to upside of the economic outlook? Stocks drive economy up – this seems to me tail wagging the dog…. Unless, of course, you subscribe to the magic “confidence” theory that approximately states that once the asset prices rise high enough, the people will spend enough to jump start the economy. (I personally will believe this only after a major country – be it USA, Japan, or EU – successfully achieves the “escape velocity”, which none of them have done. I also think that there will be a revolt long before sufficient “wealth” trickles down to the bottom 90%)

Few other “thoughts:”

1. If you superimpose this chart with USD/EUR or inverted EUR/USD, the gain doesn’t look nearly as impressive

2. All the “hot money” and the ECB “liquidity” found a new home.

3. Another proof that this has been a QE-driven world for 6+ years. Both the Japanese experience and more recent US experience (QE2, “Twist:, QE3, QE3.5 and finally the most recent “patient” FED meeting) suggest that once delivered in large quantity, the QE cannot be stopped. Until, of course, a force far greater than the Central Banks comes into play. Trade accordingly.

a pretty impressive chart, but I wonder if the takeoff point coming at about the time that the US economy kicked into a higher gear is indicative of the US economy (and the soaring USD) pulling German export business upward, or if the chart shows widespread global demand for German products.

Given the chaos that would ensue if the Greeks and Germans cannot come to an agreement on what to do about the Greek debt (which the Greeks cannot pay, and most of it is to German banks (who made loans that they ought not to have)), I cannot believe that we are seeing risk-free growth in the German business sector. It could also easily be a flight of capital from negative-rate bonds to stocks, which might propel the German economy forward, or it might not, but it certainly is money that could move out of stocks as rapidly as it has moved into them.

Hard for a foreigner to know the answers to these things, or to have a good idea of how “high” is “high”. Are the UK or Scandinavian stock markets displaying similar growth?

Where are the Germans who sit in cash, buy gold, and rail at Merkel?

http://www.nytimes.com/2015/03/23/world/europe/right-wing-groups-find-a-haven-for-a-day-in-russia.html

Oh, Russia.

Old school Axis markets on the move! Even Italy is finally on the upswing!

“We taught them a lesson in 1914 and they’ve hardly bothered us since then.”