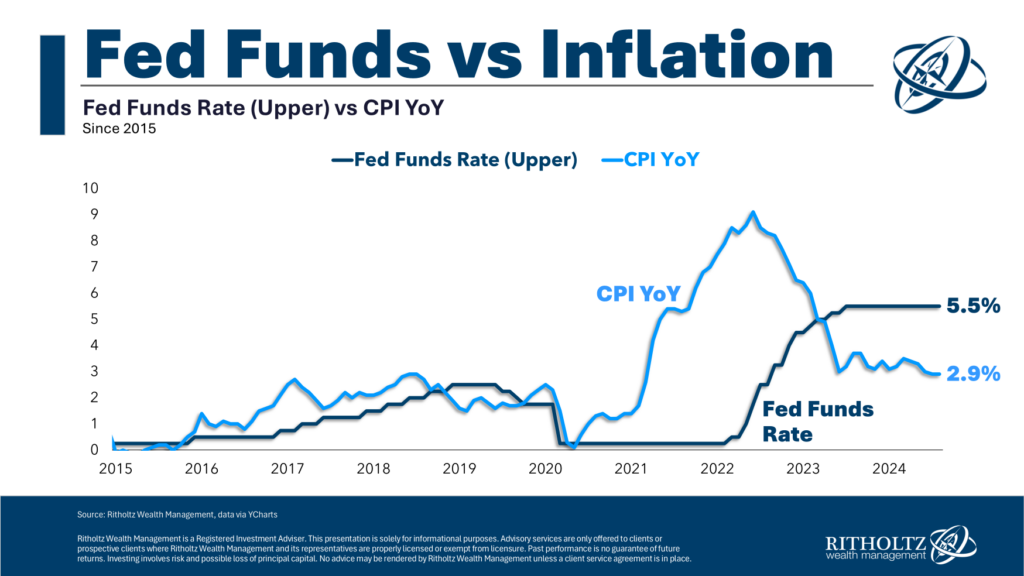

How far behind the curve is the FOMC? I’m in the last month of book leave but I felt compelled to pop out at what...

How far behind the curve is the FOMC? I’m in the last month of book leave but I felt compelled to pop out at what...

Read More

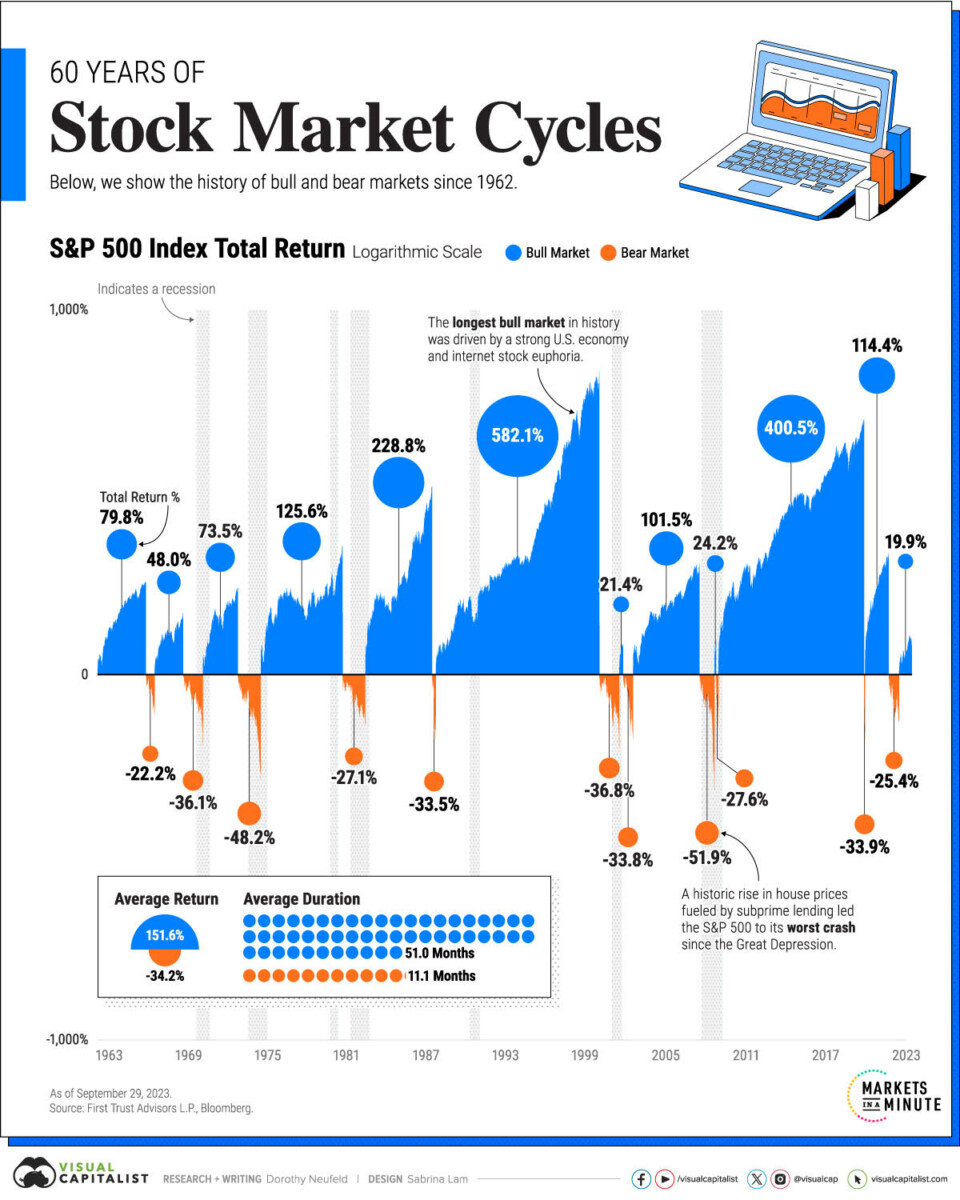

Confused about where we are today? A favorite exercise is to go back to first principles to consider how we got to where we...

Confused about where we are today? A favorite exercise is to go back to first principles to consider how we got to where we...

Read More

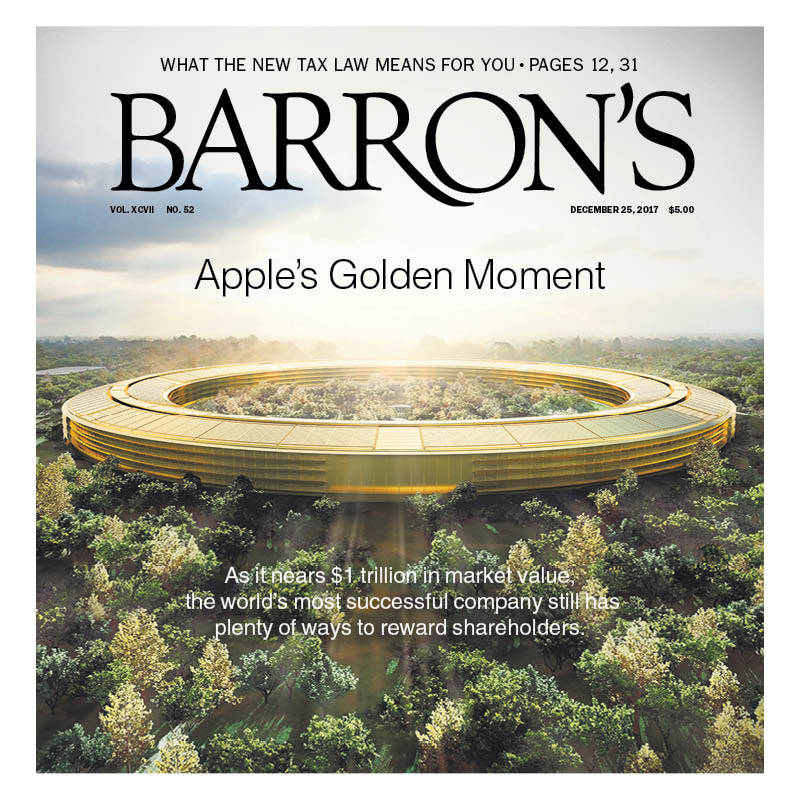

There has been a lot of chatter about magazine covers lately; We can clarify some of that with this post (originally published in...

There has been a lot of chatter about magazine covers lately; We can clarify some of that with this post (originally published in...

Read More

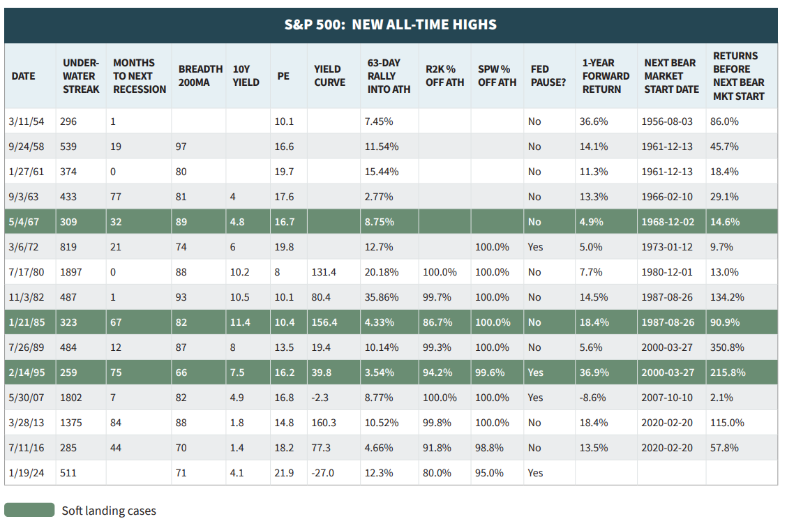

A quick note to answer this question: What happens after markets make a new all-time high (after a year w/o one)? Check out the...

A quick note to answer this question: What happens after markets make a new all-time high (after a year w/o one)? Check out the...

Read More

At the Money: Is War Good for Markets? (February 14, 2024) What does history tell us about how war impacts the stock...

Read More

What are the Bull and Bear cases for 2024? I don’t do annual forecasts1 because the short-term is way too random....

What are the Bull and Bear cases for 2024? I don’t do annual forecasts1 because the short-term is way too random....

Read More

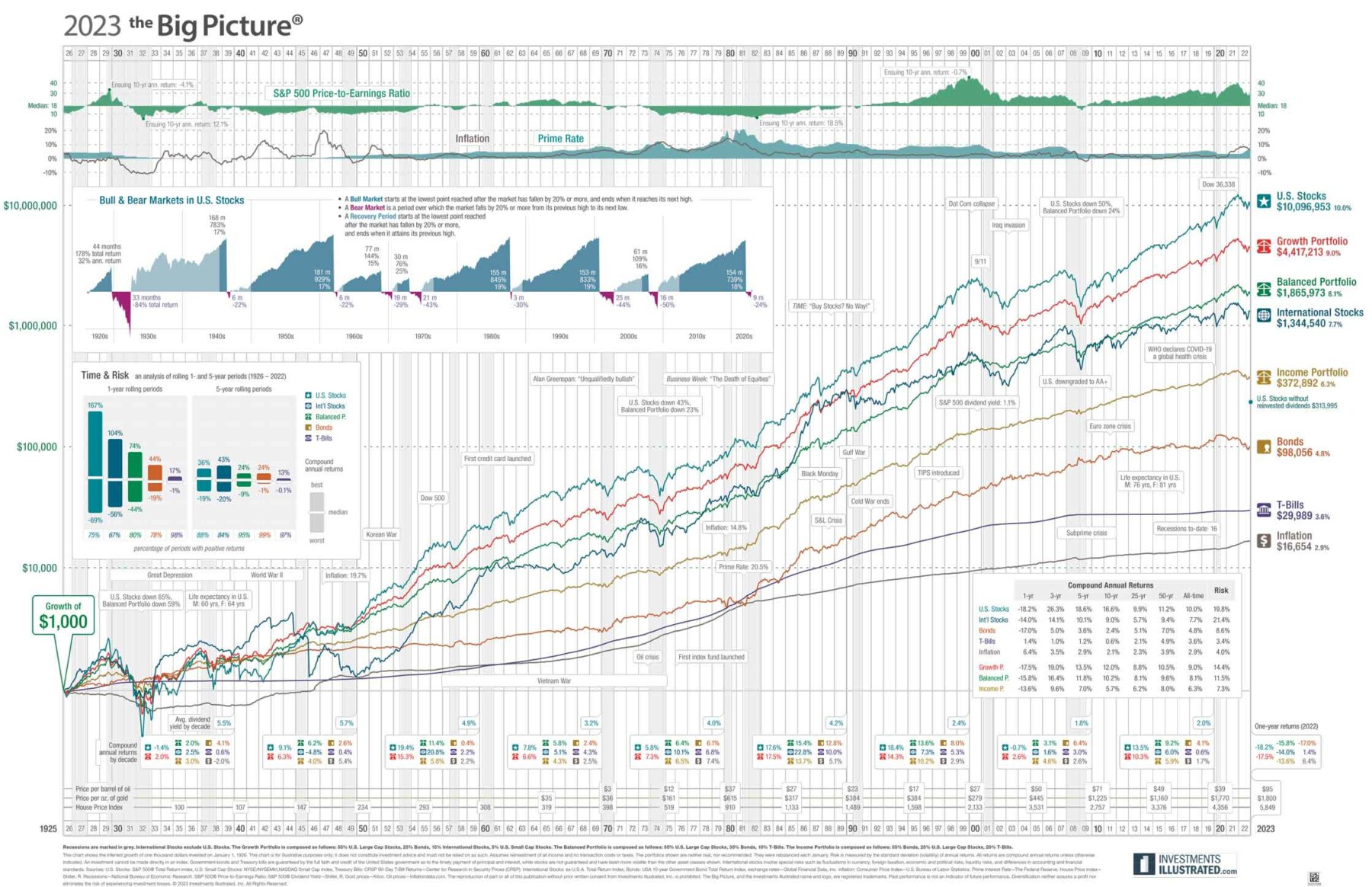

Love this giant chart! You can order one at Investments Illustrated

Love this giant chart! You can order one at Investments Illustrated

Read More

I have a vivid recollection of the period following the Great Financial Crisis: I spent March to September of 2008 writing Bailout...

I have a vivid recollection of the period following the Great Financial Crisis: I spent March to September of 2008 writing Bailout...

Read More

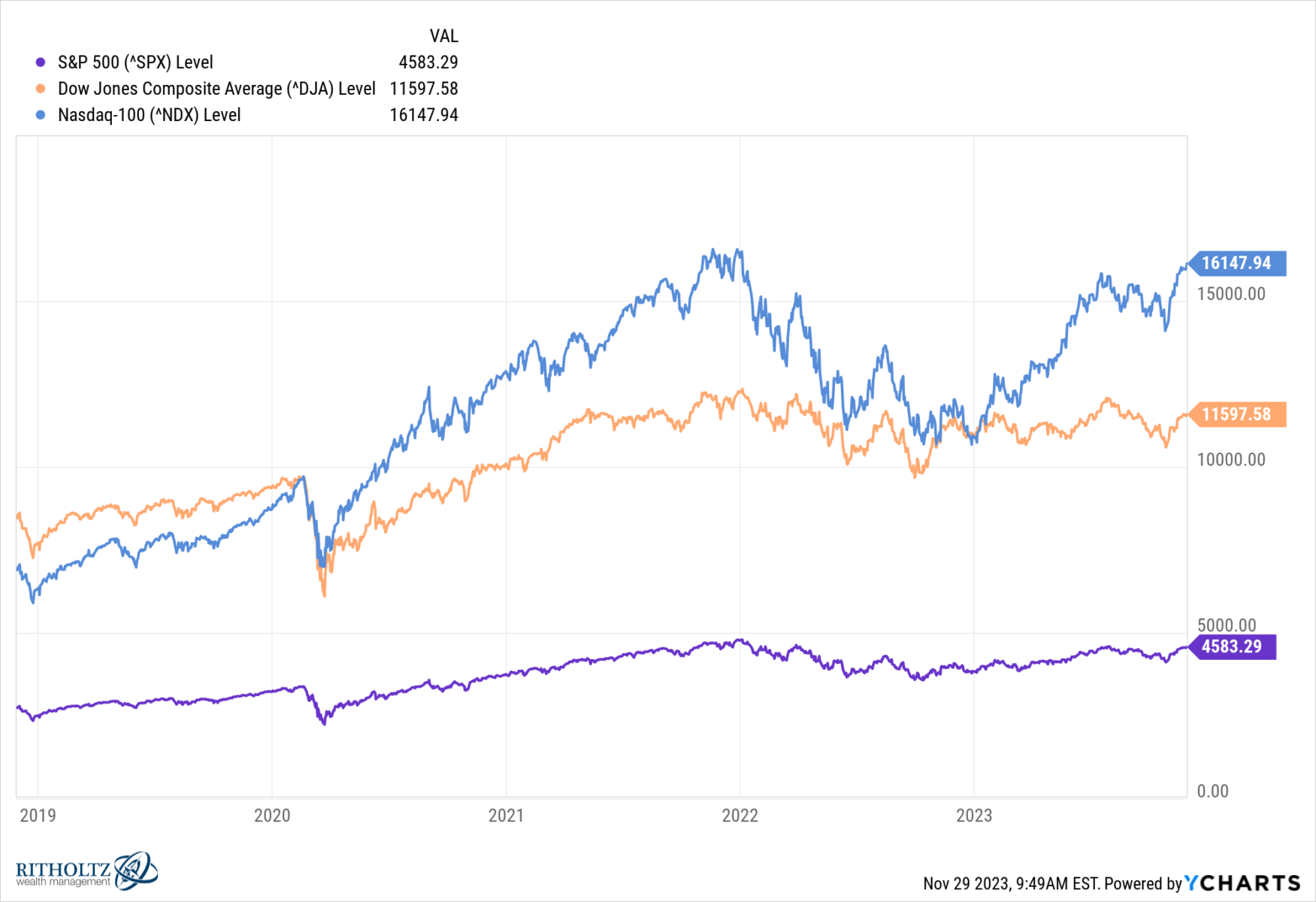

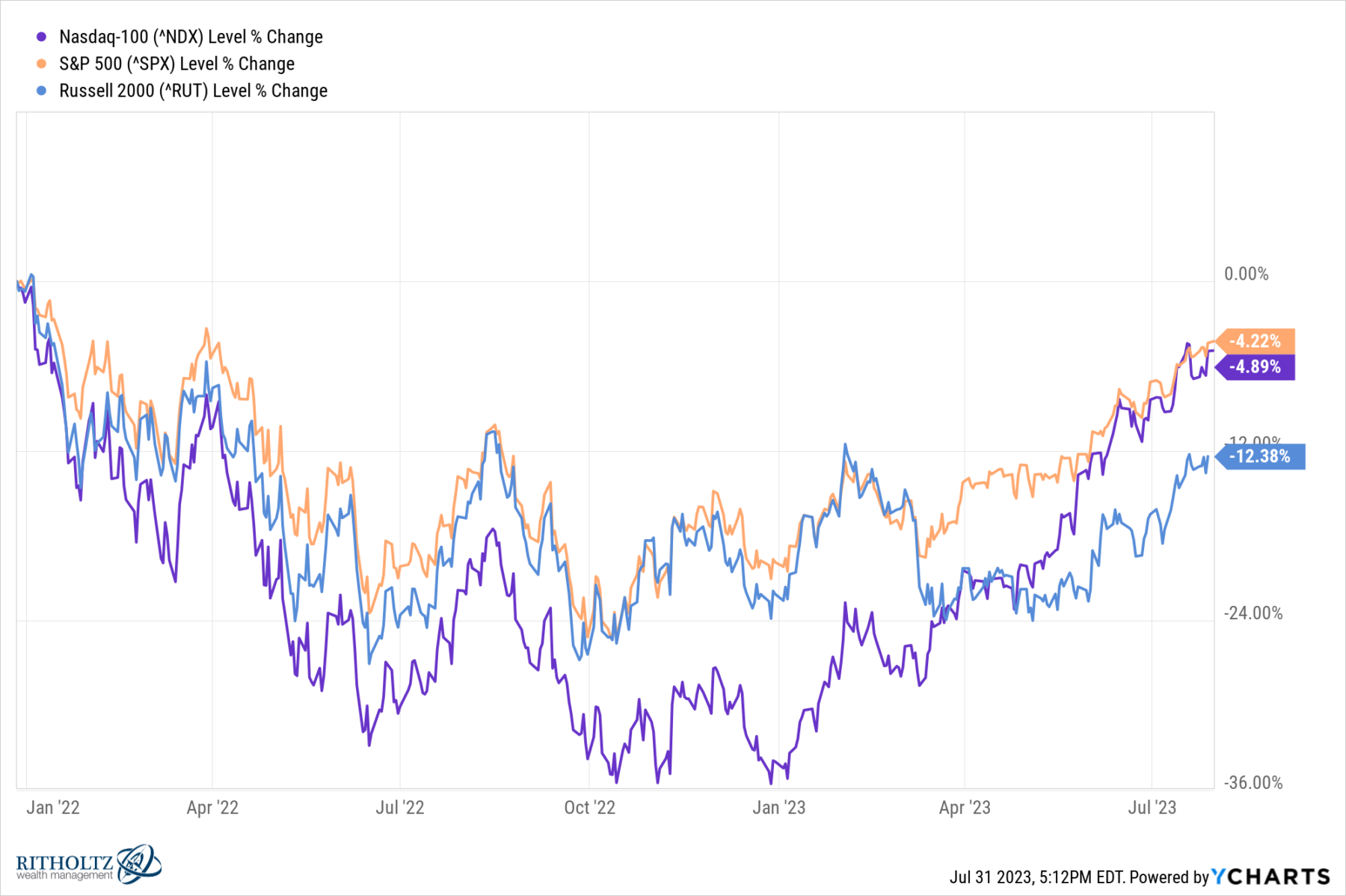

After a monstrous 68% recovery from the March 2020 pandemic low, and another nearly 30% gain in 2021, markets decided to...

After a monstrous 68% recovery from the March 2020 pandemic low, and another nearly 30% gain in 2021, markets decided to...

Read More