Why politics and investing don’t mix

Washington Post, February 6, 2011

Washington, I’m here to tell you, politics and investing don’t mix.

Yep, I thought I’d begin our conversation about investing by rocking your most cherished beliefs. Many of you are active in party politics, work for government or are involved in related fields. Well, I have some bad news: Your politics are killing you in the markets.

In my work, I use behavioral psychology, statistics, cognitive biases, history, data analysis, mathematics, brain physiology, even evolution to make better investing decisions. Indeed, these are all key to learning precisely what not to do. While making good decisions can help your portfolio, avoiding bad ones is even more important.

We humans make all the same mistakes, over and over again. It’s how we are wired, the net result of evolution. That flight-or-fight response might have helped your ancestors deal with hungry saber-toothed tigers and territorial Cro Magnons, but it drives investors to make costly emotional decisions.

And it’s no surprise.

It’s akin to brain damage.

To neurophysiologists, who research cognitive functions, the emotionally driven appear to suffer from cognitive deficits that mimic certain types of brain injuries. Not just partisan political junkies, but ardent sports fans, the devout, even hobbyists. Anyone with an intense emotional interest in a subject loses the ability to observe it objectively: You selectively perceive events. You ignore data and facts that disagree with your main philosophy. Even your memory works to fool you, as you selectively retain what you believe in, and subtly mask any memories that might conflict.

Studies have shown that we are actually biased in our visual perception – literally, how we see the world – because of our belief systems.

This cognitive bias is not an occasional problem – it is a systematic source of errors. It’s not you, it’s just how you are built. And it is the reason most people are terrible investors.

How does this play out in the world of investing? Let me share two examples. I don’t pick favorites: Both Democrats and Republicans are implicated.

Back in 2003, the dot-com crash had about run its course. From the peak of the market in March 2000 to the March 2003 trough, the Nasdaq had gotten crushed, losing 78 percent of its value.

As Federal Reserve chief Alan Greenspan took rates down to 1 percent, the Bush administration passed $1 trillion in tax cuts. As someone else once said about the stock market, “Give me a trillion dollars, and I’ll throw you one hell of a party.”

Yet many of my Democrat friends on Wall Street – fund managers, traders and analysts – were highly critical of the tax cuts. At the time, I heard all the reasons why they were so bad: They were deficit-busters, unlikely to create jobs, giveaways to the wealthy.

While those critiques may have been true, they were also irrelevant to equities. As armchair policy wonks obsessed over these issues, they missed the bigger picture: Liquidity is a major factor in how the economy and stock markets perform. Trillions of dollars in fresh cash was very likely to goose equities higher. (Sound familiar?) Indeed, the impact of the tax cuts did just that. Combined with Greenspan’s ultra-low rates, you had the makings of a cyclical bull market rally. From 2003 to 2007, the Standard & Poor’s 500-stock index – the usual benchmark for equities – gained 100 percent.

And my politically active friends on the left missed most of it.

Fast-forward six years to the recent credit crisis. The S&P 500 had fallen 57.69 percent. By March 2009, op-eds in the Wall Street Journal blamed the crash on President Obama.

But conditions were forming that would hasten the end of the sell-off. Markets were deeply oversold. Once again, the Fed chair was cutting rates – this time, it was Ben Bernanke, and he took rates down to zero. In a panic, Congress forced the accounting rule-making body to be more accommodative to the banking sector. FASB 157, as it is known, ended mark-to-market accounting – essentially allowing banks to hide their bad loans.

All these factors suggested that a substantial rally from the market lows was coming. Historically, average gains in post-crash bouncebacks were 70 percent. The easy money to the downside had been made, and it was time to stop betting that the markets were heading south. If history held true, we were looking at the mother of all bear market rallies.

By that March, I was explaining this to clients, the news media and co-workers. But the greatest pushback this time around came from across the political spectrum. My GOP pals were lamenting the occupant of the White House. I heard things like “Obama is a Kenyan, a Muslim, a Socialist. He is going to kill business.”

What followed was the single most intense two-year rally in Wall Street history. As of Friday, the S&P 500 has gained 93.8 percent.

And my politically active friends on the right missed most of it.

Remember, the cycle of booms and busts are surprisingly regular occurrences. What some people call a “100-year flood” actually happens far more frequently – since 1929, there have been 18 crashes.

It’s just as important that an investor participate in the cyclical bull markets, capturing the rally as well. All things considered, missing the downside and catching the upside makes for a pretty decent investment strategy.

You need not be a mathematical wizard to learn this lesson. When you are in the polling booth, vote however you like; But when you are reviewing your investing options, it is best to do so with a cold, dispassionate eye.

Understanding how your own biases impact your investing process is a key step. If you want to avoid making certain errors, you must at least be aware of them.

And now you are.

~~~

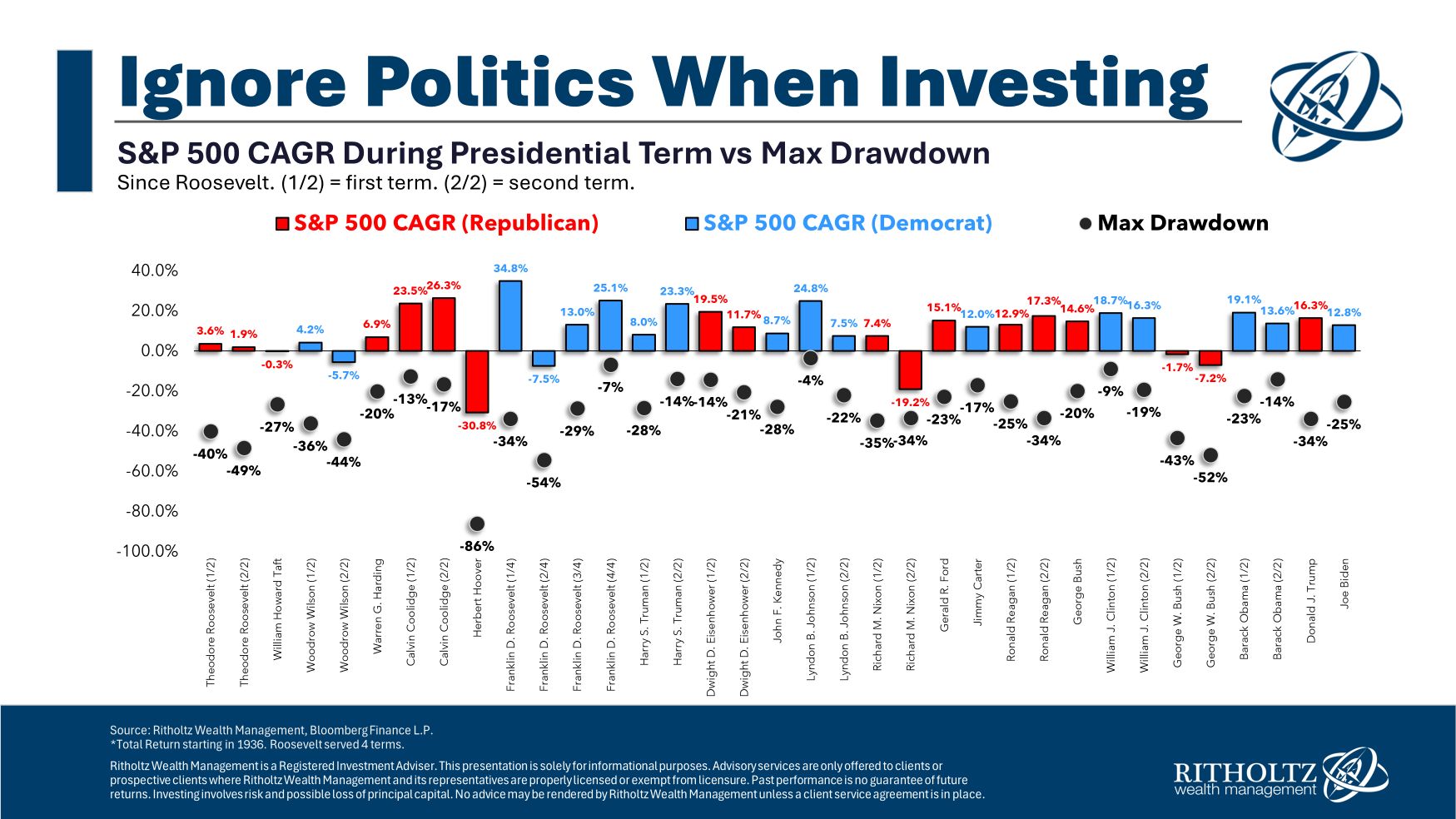

Update July 28, 2024

Sure wish I had the RWM Graphics team when I first began publishing at the Washington Post back on February 6, 2011…