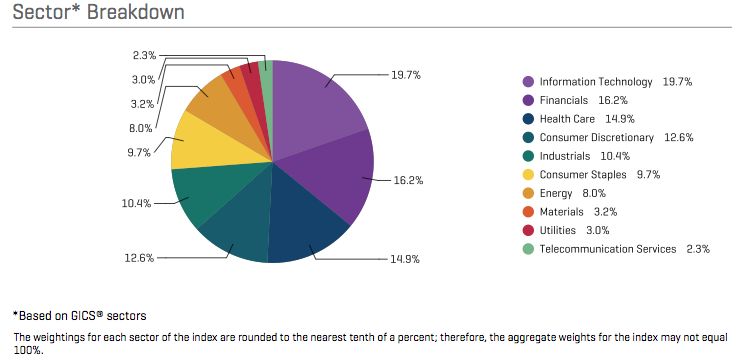

click for larger graphic

The Standard & Poor’s 500 Index is market-capitalization weighted, meaning that companies with higher stock-market valuations have a bigger influence on the index. There has been a cottage industry of criticism about this structure. Recently, it has led to a new world of fundamental indexing and so-called smart beta, or seeking ways of using the components of the index to outperform the index itself.

The S&P 500 wasn’t always set up this way. This is a good time to think about the subject, because today marks the anniversary of the index’s overhaul, giving us the structure we have now.

According to the S&P 500 2001 Directory (hat tip to Jason Zweig’s This Day in Financial History), the benchmark index for large cap U.S. stocks looked very different than it did before this day in 1988.

Back then the index was made up of:

400 industrial stocks

40 utilities

40 financials

20 transportations

This seems like it was an effort to mimic Dow Jones, which had three big indexes — the Industrial Average, the Transportation Average and the Utilities Average. According to the Dow Jones Industrial Average Fact Sheet, the Industrial Average was designed “to represent large and well-known U.S. companies, cover[ing] all industries with the exception of Transportation and Utilities.” Having been around since the late-19th century, it had become the benchmark for measuring the U.S. stock market.

Continues here: The S&P 500’s Dubious Anniversary

Prior to 1988 if you looked at the S&P industries you would know that the historic record for a specific period contained the stocks that were actually in that index in the period you were looking at. Now, the stocks in an industry now may be completely different than it was in an earlier period. The industry where this may have had the biggest impact was the gold industry. It use to be dominated by the South African gold mining firms. Now it only has US firms so the history since 1988 is of a completely different set of companies than it was prior to 1988. Interestingly, my regression of the relative performance of the gold stocks continued to work after the change, even though one of the most important variables was the South African Rand. I guess the pressures on the South African mines from the Rand radiated to the other gold mining companies.

Two different issues are being conflated here. Pre-1988, the S&P had fixed numbers of industrial, utility, financial and transport issues. But my understanding is that the 500 stocks were and always have been market-cap weighted, despite the number of issues in each sector being fixed in earlier years.

David Blitzer, chairman of the index committee at S&P Dow Jones Indexes, could confirm that the S&P 500 (and the S&P 90, before March 4, 1957) always have been value weighted.

http://www.indexologyblog.com/2013/08/13/sp-500-and-dow-jones-industrial-average/