October 19, 2015

Five Bad Reasons For The Fed To Raise Rates Now – And One Good Reason Not To

A couple of days before the September 16-17 FOMC meeting, I happened to be listening to the NPR program, “On Point”, the subject of which was the appropriateness of a Fed policy interest rate increase at that time. Of the guests on the show, the principal advocate of Fed “lift-off” was a William Cohan, who had written an August 28 New York Times op-ed entitled “Show Some Spine, Federal Reserve”. As much as I disagreed with Mr. Cohan’s reasons for why the Fed should have raised its policy interest rates on September 17, reasons that I assume Mr. Cohan still would believe valid now, I was delighted to hear them. I was delighted because Mr. Cohan’s and others’ arguments in favor of immediate Fed interest rate hikes provided me with material for this commentary. I would have written it sooner, but I was otherwise occupied in the waning days of the sailing season up here in Packerland. So, let’s get at countering three of Mr. Cohan’s arguments and two that I have heard from others whose names I cannot recall (because I’m old).

Firstly, the claim by Mr. Cohan is that the Fed’s zero interest rate policy (ZIRP), has hurt household savers because they are earning next to nothing on their deposits and other fixed-income investments. It is true that household interest income relative to household after-tax income fell to its lowest in 2014 since 1968, as shown in Chart 1.

Chart 1

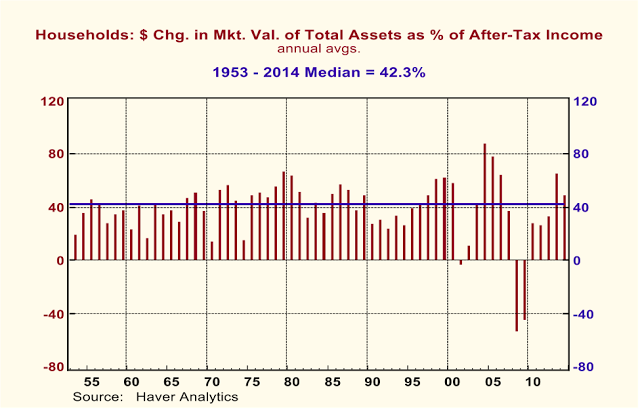

But, while household interest income has been weak since the inception of ZIRP, dollar changes in the market value of total household assets relative to after-tax income have rebounded to levels above their long-run median in the past two years, as shown in Chart 2.

Chart 2

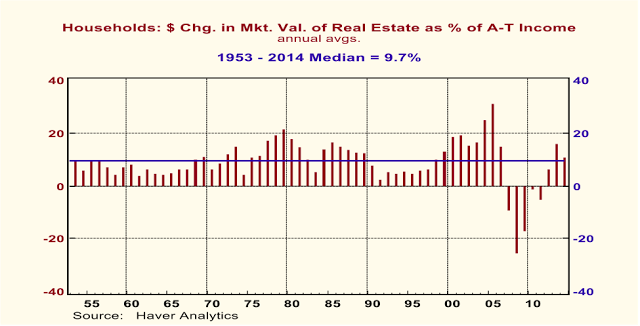

A rebound in residential real estate values has contributed to the rebound in the relative value of total household assets, as shown in Chart 3.

Chart 3

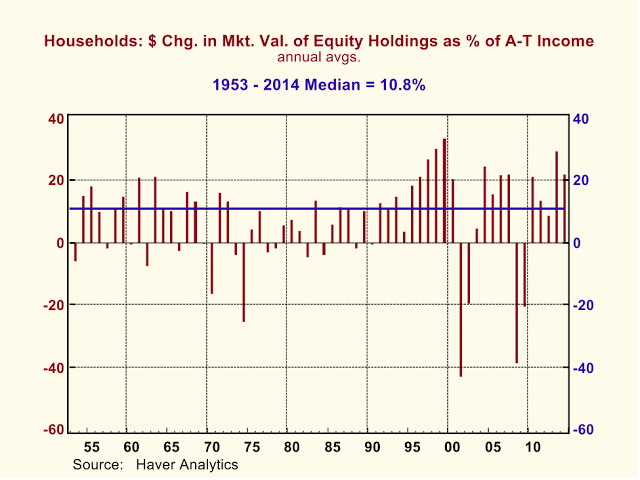

But just as baseball had been berry, berry good to Chico Escuela (episode 5 of SNL season 4 – I told you I was old), ZIRP and QE have been berry, berry good for the value of equities. Chart 4 shows that in four of the past five years, the dollar change in the market value of equities held directly and indirectly by households relative to after-tax income has been above its long-run median value.

Chart 4

The upshot of all this is that despite ZIRP, or perhaps more accurately, because of ZIRP, households have fared rather well in terms of increases in the value of their assets. Nowhere is it mandated that households store their savings in bank deposits or Treasury bills. If ZIRP and QE are good for equities and bad for bank deposits, then allocate more of your assets to equities. There are plenty of equity mutual funds and ETFs that can accommodate “small” savers.

Secondly, the claim by Mr. Cohan is that ZIRP has been a gift to banks inasmuch as they are paying next to nothing in interest to borrow funds. According to this view, the Fed should raise its policy interest rates in order to lessen the alleged subsidy to banks from ZIRP. The fed funds rate is the marginal cost of funds to banks. When the fed funds rate is close to zero, banks’ marginal cost of funds also is near zero. But bank lending is based on interest-rate spreads over their marginal cost of funds. For example, the short-term lending interest rate charged by banks to their most credit-worthy business borrowers, the prime rate, is three percentage points above the fed funds rate, regardless of the level of the fed funds. So, banks net interest income is more a function of the volume of bank loans rather than the level of the fed funds rate.

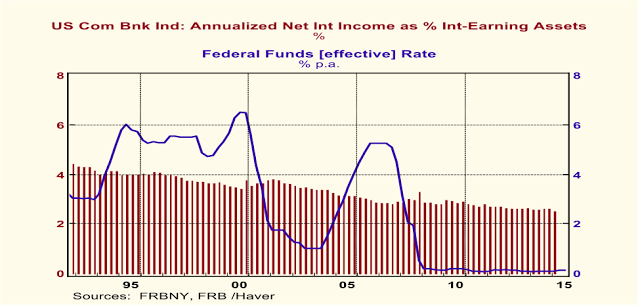

Plotted in Chart 5 are quarterly observations of the U.S. commercial banking sector’s consolidated net interest income (interest revenue earned on loans and securities minus interest costs on deposits and other borrowed funds) as a percent of interest-earning assets. Also included in Chart 5 are quarterly observations of the fed funds rate level. In Q1-2015, the latest data available, banks’ net interest income was 2.52% of their interest-earning assets – the lowest percentage in the history of the data series. ZIRP has not enriched banks in terms of their net interest income. So, ZIRP has been no gift to bank profits in terms of net interest income.

Chart 5

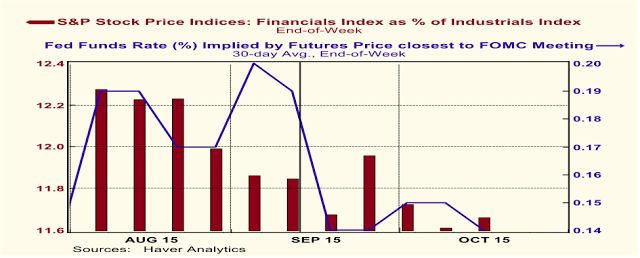

If ZIRP is such a gift to banks, we would have expected the stock prices of financial corporations to rally relative to those of industrial corporations after the Fed failed to raise its policy interest rates on September 17. But just the opposite happened. As shown in Chart 6, in the week ended September 18, the value of the S&P stock price index for financial corporations fell relative to the value of the S&P stock price index for industrial corporations (the first red bar after the solid vertical line in the chart). The expected 30-day average level of the fed funds rate also fell in the week ended September 18 after the Fed “disappointed” market expectations of a hike in its fed funds rate target.

Chart 6

Actually, there is a reason that short-maturity asset-management divisions of banks might loathe ZIRP. Under ZIRP, the yield on short-maturity fixed-income securities is close to zero. But there are fixed costs involved in managing clients’ short-maturity investments. In order to earn a “normal” profit on managing these client portfolios, it might require that asset managers charge their clients fees in excess of the yield on short-maturity investments, implying a negative return on client portfolios when fees are included. It’s a hard sell to get clients to accept a negative return on short-maturity investments. The potential negative goodwill generated by negative returns might cause the bank to lose other profitable business from the client, either currently or in the future. As a result, the asset-management division might choose to forgo some of its fees in order to retain client goodwill. At least in the short run, this would have a negative effect on bank profits.

Thirdly, it is argued by Mr. Cohan that the Fed should lift its policy interest rates above zero because a Fed-administered zero rate of interest results in the mispricing of risk in the economy. In order for risk to be properly priced, interest rates need to reflect the market forces of supply and demand. I would go a step farther. If risk is to be priced properly, the Fed should abandon all direct interest rate targeting – zero or otherwise. This is what Milton Friedman (may he rest in peace) advocated when he prescribed that the Fed target the growth rate of a monetary aggregate, an element of the supply of credit, rather than an interest rate, the price of credit. How do we know that risk will be more appropriately priced at Fed-mandated federal funds rate of 25 basis points rather than at 13 basis points?

Fourthly, it has been argued by others that an important factor accounting for the August and September declines in U.S. stock market indices was the uncertainty as to when the Fed would raise its policy rates. The implication of this argument is that to boost stock prices, the Fed needs to raise its policy interest rates sooner rather than later in order to remove uncertainty. Let me counter this argument with an analogous scenario. Suppose, after a routine physical exam with your doctor, she tells you that you might have a terminal disease, which, at best, would give you only three more months to live. But she isn’t sure about this. Further analysis is needed to validate the diagnosis — analysis that will take three days. If you are similar to me, this uncertainty about the diagnosis will elicit anxiety and depression. Three days later, your physician calls, telling you the uncertainty is over. You, in fact, do have a terminal disease and you had better clean up your desk. (The mess on my desk during my full-employment days was infamous and remains so in my semi-retirement.) Tell me, now that the uncertainty has been lifted, are you elated?

All else the same, a Fed interest rate hike has negative implications for risk assets. A Fed interest rate hike implies a reduction in the supply of Fed-created thin-air credit. (I bet you wondered how long it would take me to get around to thin-air credit.) So, yes, there is uncertainty about when the Fed will raise its policy rates. But the removal of that uncertainty by the Fed actually raising interest rates is akin to your doctor removing the uncertainty about your fatal-disease diagnosis by telling you that you do, indeed, have it.

Fifthly and lastly of the bad reasons, it is argued by others that the Fed needs to raise the level of its policy interest rates now so that it will have some margin to lower their level later if the economy weakens. If there is a high probability of the economy weakening anytime soon, why would it be good policy to raise policy interest rates now. Wouldn’t that just hasten the economic weakening? Moreover, haven’t we just observed in recent years that ZIRP doesn’t preclude QEP (Quantitative Easing Policy)?

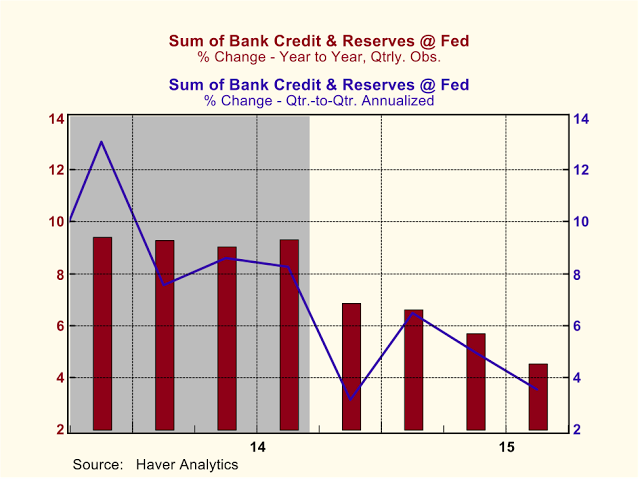

Now, for the good reason that the Fed should not to raise its policy interest rates at this point in time – you guessed it, the current weakness in the growth of thin-air credit. Plotted in Chart 7 are the year-over-year and quarter-to-quarter annualized percent changes in thin-air credit, i.e., the sum of commercial bank credit and depository institution (primarily commercial banks) reserves held at the Fed. The shaded area in Chart 7 represents a period in which Fed QE policy was in effect (through the end of Q3-2014). When QE3 was terminated on a quarterly basis in Q3:2014, thin-air credit was growing year-over-year at 9.4% and quarter-to-quarter at 8.3% annualized. This compares with the long-run median growth in this measure of thin-air credit of about 7-1/4%. So, it was appropriate for the Fed to scale back on its contribution to thin-air credit in order to prevent an asset-price bubble and/or an acceleration in the prices of goods/services. But, in my opinion, the Fed has overdone the slowing of thin-air credit growth. In Q3-2015, year-over-year growth in thin-air credit slowed to 4.5% and quarter-to-quarter annualized growth slowed to 3.5%. This sharp deceleration in the growth of thin-air credit represents a tightening in monetary policy in a Friedman sense.

Chart 7

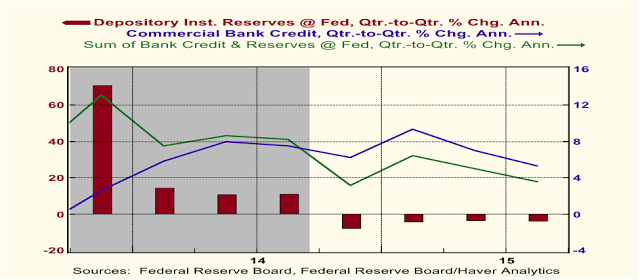

Chart 8 shows who is primarily responsible for the sharp slowing in thin-air credit growth in the post-QE period. It is the Fed. Again in Chart 8 as in Chart 7, the shaded area through Q3-2014 represents a period in which QE was in effect. As the Fed began to taper its purchases of securities at the start of 2014, growth in depository institution reserves at the Fed (the red bars in Chart 8) slowed sharply. At the same time, growth in commercial bank credit (the blue line in Chart 8) accelerated enough to allow the sum of bank credit and reserves at the Fed (the green line in Chart 8) – total thin-air credit – to grow at a robust rate in the range of 7-1/2% to 8-1/2%. But starting in the fourth quarter of 2014 and every quarter thereafter, reserves at the Fed have been contracting. Despite relatively strong growth in bank credit through Q2-2015, growth in total thin-air credit sagged well below its long-run median rate. And in the third quarter of 2015, growth in commercial bank credit slowed appreciably to 5.3% annualized. This, in combination with the contraction in reserves at the Fed, resulted in the very slow growth in total thin-air credit of 3.5% annualized.

Chart 8

The Fed has been engaged in quantitative tightening (QT) for about a year now. Unless depository institution demand for reserves were to fall, an increase in Fed policy interest rates would require a further contraction in the supply of Fed reserves. Barring a sufficient pick up in commercial bank credit, this would imply a further deceleration in total thin-air credit.

The pace of economic activity already appears to have slowed in reaction to the sharp deceleration in thin-air credit growth. Why would the Fed want to raise its policy rates later this month or in December and risk having the pace of economic activity stall out? Rather than dithering over whether it should raise interest rates in December, perhaps the Fed ought to be contemplating another round of quantitative easing!

Source: Paul L. Kasriel

The Econtrarian

It is odd that raising now to have room in the future is mentioned:

Fifthly and lastly of the bad reasons, it is argued by others that the Fed needs to raise the level of its policy interest rates now so that it will have some margin to lower their level later if the economy weakens.

But not the real way to make some margin – target a higher level of inflation. We know zero is different, and 4% not damaging relative to 2%, so why not target a higher level of inflation? I would imagine it would take longer to go from a comfortable, at-target, level to 0 if you were starting at 4% vs 2%. With that extra time, there’d be windows to work to ease conditions.

Everyone is so concerned about the change in rates, but that’s not what matters. What matters is the level of rates. The logic is much simpler than presented here: our economic conditions are no longer extraordinary, so why do we need to continue boosting them with extraordinary monetary policy? Rates could be raised to 2% tomorrow and that would still be very low rates that stimulate the economy. Before the Great Recession, rates had only ever touched those levels 3 times before, for some historical context.

You cannot judge the level of the rates by comparing to averages over x hundreds of years. The economy is dynamic and in constant development. According to the economic parameters there is nothing “extraordinary” about the level of current rates. Indeed chart 7 provides support for the argument that current rates are extraordinarily high.

I don’t necessarily agree that an interest rate environment where there’s basically no return whatsoever in fixed income is normal. Would be more interesting if Chart 7 was way more long-term than it is.

I’m not buying that asset value and stock value rising has anything to do w/ savers and or raising rates. The number of households whom held//had homes no longer have them. The rentier class is the ones whom have benefitted from the rise in household value. The same is true for stock market valuations.