There are five conclusions to draw from this report:

1) We now know that the NAIRU for the US economy is 5.0%

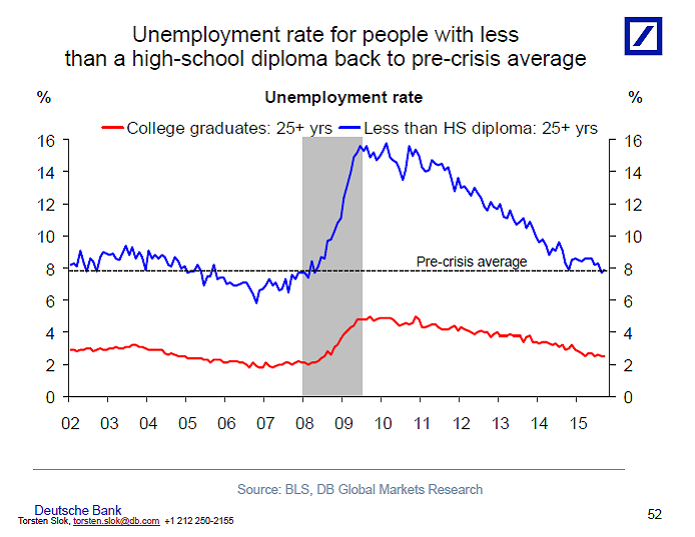

2) The anecdotal evidence we have been hearing throughout the past couple of earnings seasons about a tight labor market can now also be seen in the macro data

3) The modest slowdown in hiring in August and September was driven by the correction in the S&P500 and China worries. That shock is now behind us and slow growth in the rest of the world and dollar appreciation are not pushing the US into a recession.

4) From a Fed perspective, the US labor market is now showing signs of overheating.

5) Secular stagnation was never real, it just took a long time for the economy to recover after the financial crisis.

Source: Torsten Sløk, Ph.D., Deutsche Bank Research

I guess that if you know what you want to conclude then any dataset can be used as support. Not a single one of those “conclusions” are supported by the NFP report.

1. Really?

2. Really?

3. Really?

4. Really?

5. Really?

Numbers 2 and 4. Really? What tight labor market and where is it over heating? I’ve seen tight labor markets and honey this anti one of them!

On the other hand, I can see them queuing the “let’s increase the H1B quota” BS.

There really is a tight labor market in certain sectors like technology. Upward wage pressure is happening while executives still want to cut costs. So, yeah, they want H1B workers to drive ages down. I hope they don’t get them.

Wages that is… well… wages and ages.

Bingo!

This post sounds mad. Was the labor market overheated in late 1996? Late 05? Wages accelerated in the 3rd quarter. Maybe it was just a blip, but you can’t ignore that reality.

So NAIRU is 5% U3 huh?

Given that we are adding 200K jobs per month and therefore will soon dip under 5% we should be seeing some signs of accelerating inflation. But it is dead flat well under 2%.

https://research.stlouisfed.org/fred2/series/PCETRIM12M159SFRBDAL

In fact, the last time we had accelerating inflation on a sustained basis was 12 years ago when U3 dipped under 6%. So if NAIRU is meaningful now, we are waaay behind the curve of our phantom inflation. https://research.stlouisfed.org/fred2/series/UNRATE

Back in the real world, the CPI is LOWER now than in July, 2014. Do economists ever doubt their can openers?

None of Deutsche Bank Research conclusions are adequately justified but elites clearly want interest rates to go up so up they go; just needs a bit more intellectual cover that’s all.

It is difficult to understand how anyone can argue a labor market is overheating when most sectors are still below trend in real wages and labor participation rate or why the Fed would be swayed by this since support for wage-push inflation, particularly in the current structural employment regime, is quite weak; what Fed model is being relied on here I have no idea.

I do have to note WRT #5 that a finding of insufficient evidence supporting a hypothesis does not constitute grounds for rejecting it even when that evidence is adequately analyzed (which it isn’t here); i.e., I do not see any of the stagnation predictions falsified which means this “conclusion” are unwarranted at best and possibly entirely specious.

You could have said that in the last 3 expansions. I won’t argue the labor market isn’t “overheated”. But they have warmed up a bit. 4.0% unemployment is the overheated ouchie.

Bankers flip out once their is a bit of warmth.

“The modest slowdown in hiring in August and September was driven by the correction in the S&P500 and China worries” – Seriously? In what field of science does Herr Torsten Sløk, Ph.D., has his Ph.D. in?

Any “C” student in Econ 101 will tell you that employment is one of the most lagging economic indicators.

There’s simply no possibility that “slowdown in hiring in August and September was driven by the correction in the S&P500 and China worries” that also happened in August and September!!!

It takes MONTHS from the time when companies start evaluating possibilities of increasing staff until the time the actual new employees “punch in” on their 1st day on the job. Herr Sløk seems to be full of “sløk.”

Profits dropped as wages accelerated. Classic mid-cycle belch. Every bit of news freaked out the flock.

There are help wanted signs at a couple of Home Depots here in NJ. Also, I think I saw Solar City needs help.