One of the big concerns for investors is the health of corporate profits, which have declined in the three of the past four quarters (the last quarter with full data ended Sept. 30, 2015, though forecasters have predicted a decline in fourth-quarter profits as well). The natural question is whether falling earnings point to a recession.

I put that question and a few others to James Bianco, president of Bianco Research LLC, an institutional research firm servicing many of the world’s largest mutual funds, hedge funds and sovereign-wealth funds. Below is our exchange:

BR: A recent research report by JPMorgan found that when markets see consecutive quarters of earnings declines, the economy slips into a recession 81 percent of the time. What do you make of this?

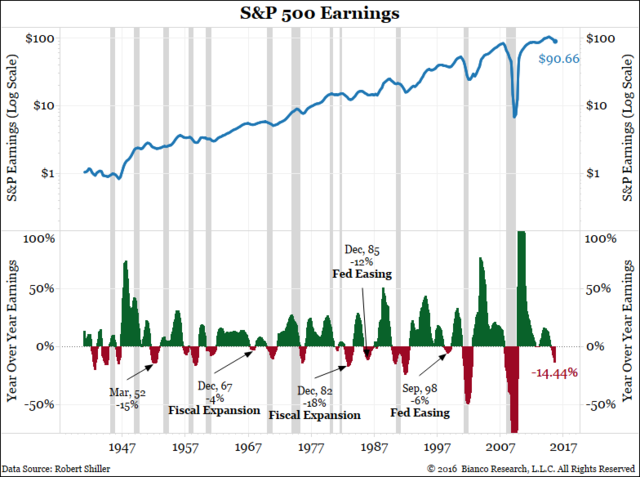

JB: Our chart below starts in 1940 and shows Standard & Poor’s 500 Index earnings in the top panel and their year-over-year change in the bottom panel. The shaded areas highlight the 12 recessions over this period.

Earnings turned negative either during or just after all 12 of these recessions. This should come as no surprise. Also noted on the chart are the five instances when earnings turned lower (at least two consecutive quarters) without a recession.

The last time earnings went negative without a recession was September 1998. The Federal Reserve was easing in the wake of the Long-Term Capital Management collapse and the Asian financial crisis. Earnings also turned lower in the absence of a recession in December 1985. The Volcker Fed was aggressively easing at the time. Earnings turned down in December 1982 after the “twin recessions” between 1979 and 1981. During this period the budget deficit was exploding, a phase of rapid fiscal expansion. Earnings turned down in December 1967 with no recession in sight. Again, fiscal expansion, the “guns-and-butter” idea promoted by President Lyndon Johnson, was the order of the day.

Hence, the last time earnings turned lower without a recession, Fed easing or fiscal expansion was in 1952. So if we are going to be in a period of negative earnings in the absence of any of these, it would be the first time in more than 63 years.

BR: How important are earnings to forecasting economic cycles? Everyone else seems to be looking at the yield curve.

JB: Company reports (aka earnings) are the raw material of economic reports. Where do retail sales, prices, jobs, durables and other data come from? Company reports. The same ones that earnings come from.

BR: What about earnings excluding energy? Can we sequester a part of the market?

JB: No. I include it because so many ask about it. It’s like saying you’re healthy if you ignore that your foot has gangrene! There is always a reason for slumping earnings (2008, housing; 2001, tech) so this isn’t new or different. It is a rationalization for bulls.

Also, I believe the measure is flawed. It takes out energy companies that are hurt by falling crude prices. But it doesn’t take out retailers, industrials or basic materials that are helped by falling crude prices. Why not?

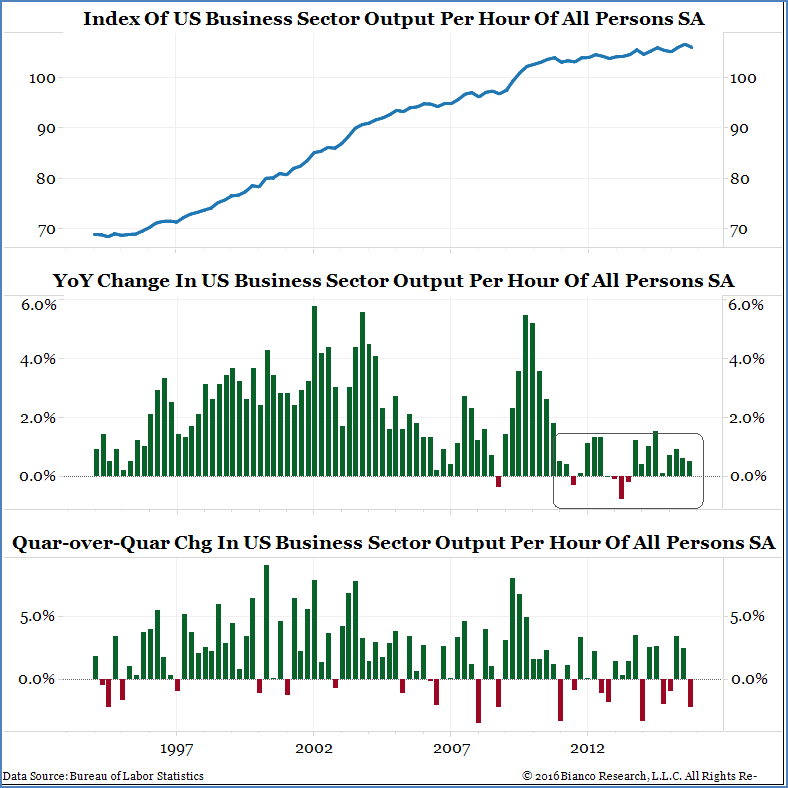

BR: What does all this mean in the context of strong payrolls data?

JB: I think you’re asking why hiring is so strong, yet earnings so weak. The answer is productivity. See the chart below. We add workers but it’s not increasing gross domestic product, so productivity wanes.

Originally: Falling Earnings, Recession Warning