Many traders and investors acts as if markets are efficient, meaning that asset prices fully reflect all available information. We see this manifest itself in numerous ways — how prices rapidly adjust to new information and how few investors manage to beat the broader indexes by picking stocks or trying to time the market.

At least that’s the gist of the efficient market hypothesis, which won University of Chicago economist Eugene Fama a Nobel Prize. The problem is that in practice, there are lots of information asymmetries and frictions that make markets somewhat less than perfectly efficient. To reflect this, I started referring to Fama’s thesis as thekinda-eventually-sorta-mostly-almost efficient market theory.

That description leads us to today’s discussion about high-priced index funds.

If that sounds sort of contradictory, that’s because it is. One of the key ideas behind index funds is that they have low costs, turnover and taxes. Since most investors can’t beat the markets, why not just match the market in a fund that tracks a major index and keep investment and management expenses to a bare minimum.

But that isn’t always the case. While many index funds have fees that are almost 100 basis points less than actively managed funds, according to the Wall Street Journal, there still are quite a few expensive index funds out there. Michael Johnston of Fund Referencelists 94 funds that track the Standard & Poor’s 500 Index, sorted by expense ratio and minimum investment. Johnston concludes that only three of the funds are worth bothering with.

The most egregious example cited in his list: the $275 million Rydex S&P 500 fund, with annual expenses for the C class shares at a whopping 2.32 percent. Compare that with the Fidelity Spartan 500 Index Advantage fund and Vanguard 500 Index Admiral fund, both of which charge 0.05 percent. The other fund that gets Johnston’s thumbs up is the Schwab S&P 500 Index, with annual charges of 0.09 percent, and a minimum opening investment of just $100.

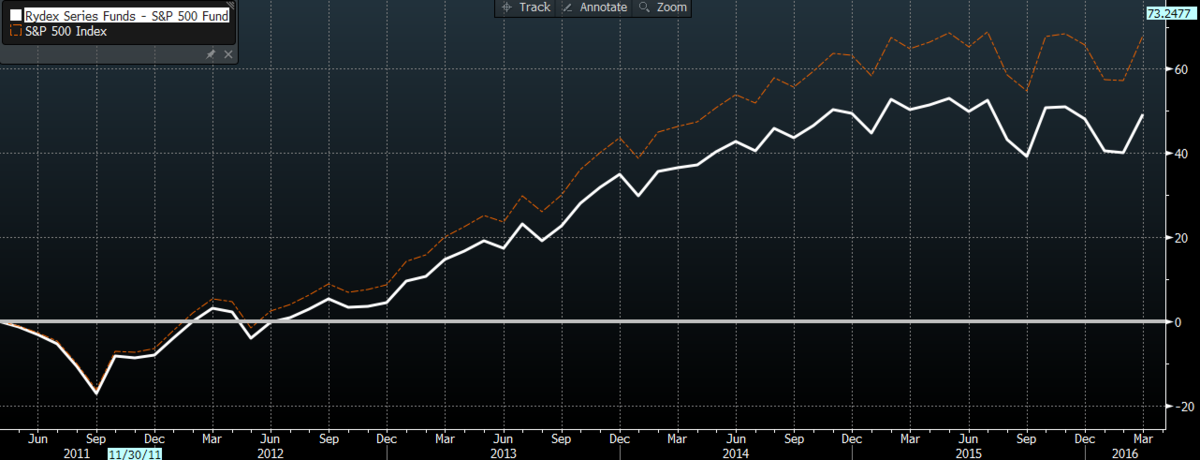

More to the point, the real test of an investment is what you get for your money. As the chart below shows, the Rydex S&P 500 fund’s high fees lead to underperformance.

Since 2011, the fund has returned an annual 8.5 percent, while the S&P 500 itself has gained 11 percent a year, according to data compiled by Bloomberg.

So how can we explain why people waste so much money on a simple index fund? Shouldn’t the market correct this?

Eventually, the efficient market hypothesis goes, it should. But it seems to take a whole lot longer than the theory would imply. Keep in mind, there are number of significant factors working against the average retail investor: Investing itself can be complex and time-consuming, and many people find it confusing. Note that this is a feature of the industry, not a bug. If everything was simple and understandable and free from jargon, high-fee index funds wouldn’t exist.

Despite this being the age of Google search, individual investors confront a tremendous information asymmetry. The industry knows much more than the consumer; brokers are aware of what things should cost and how much they can get away with charging investors. Let’s be honest: Sales people understand and make money off of impulses and irrational behavior. This goes a long way toward answering why theories that count on rational market actors often fail.

In turn, this might help to explain why expensive index funds stay in business.

Another Nobel Prize winner, Paul Krugman, tried to explain market inefficiencies in a 1997 Fortune article. He identified seven bad habits or attitudes of investors that make markets less efficient:

• Think short term.

• Be greedy.

• Believe in the greater fool.

• Run with the herd.

• Overgeneralize.

• Be trendy.

• Play with other people’s money.

All of this introduces huge amounts of inefficiency to markets. None of these behavioral patterns show any sign of disappearing soon.

As noted before, markets eventually get it more or less correct, but along the way, they can deviate from the true path of efficiency. We just need to wait a decade or three for that efficiency to sort itself out.

Originally: Overpriced Index Funds Won’t Go Away