Inflation isn’t dead; it just might not be where you think it is.

To find significant price increases, you need only look in the right places. There are many goods and services with rising prices, as well as those without. Together, they tell a fascinating tale about the modern global economy. Understanding the forces driving prices higher — or not — is crucial to investors and policy makers alike.

Given that the Federal Reserve has been trying to generate inflation for much of the past decade, the significance of the distribution is both important and telling. Why some prices are rising at twice the median rate of general inflation is worth delving into.

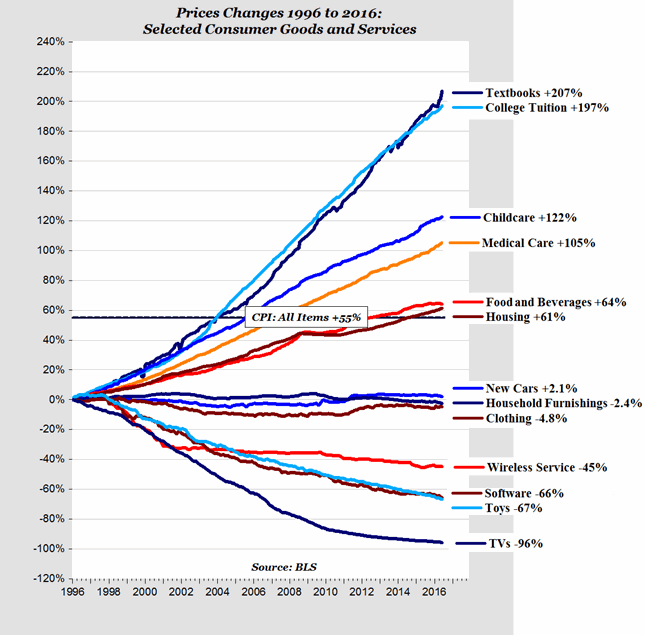

Look at the chart below: it show specific categories of goods and services versus the entire basket of goods and services that makes up the consumer price index.

Source: American Enterprise Institute

Let’s look a little more deeply at each category.

Textbooks: The industry operates as a quasi-monopoly. A student assigned a given text book doesn’t have much choice. The rise of used-book exchanges provided some competition, but the publishers merely issue revised editions that are neither new nor improved. Inflation here is a function of rentier capitalism. Note that other kinds of books have fallen in price during the same period.

College Tuition: Blame demographics, guaranteed student loans and administrative bloat. The baby boomers’ kids created many more potential college students than there were seats, leading to an imbalance in demand and supply. Responses varied from adding more professors to expanding class sizes to opening new schools.

But most schools responded by raising tuition.

And students paid. The Federal Reserve Bank of New York and theNational Bureau of Economic Research looked at increases in student borrowing, funded largely through federal student-loan programs. There is a good argument to be made that this is what has drivenmuch of the increase in college tuition.

Medical Care: The bottom line in the relentless rise in health-care costs is that market forces don’t work very well in this industry. This is why every modern industrialized country, except the U.S., has a single-payer government option or something like it. Even worse, the drug industry has persuaded Congress to bar government-run health programs from negotiating lower prices.

Food and Beverages: Prices for milk, beef and most other foodstuffs soared in the 2000s, as the U.S. dollar lost 41 percent of its value (many commodities are priced in dollars) and commodity prices soared.

Housing: During the 2000s housing boom, when lending standards evaporated, home prices went up two and three times their normal rates. But the Bureau of Labor Statistics had the cost of housing as falling. Why? The BLS uses something called owner’s equivalent rent, and it tends to give false reads on housing prices.

When more people are buying and driving up home prices, it means less demand for rental units, leading to lower prices. During the housing bust circa 2006-2011, they showed the opposite. Fewer buyers meant more renters, and so rental price gains were robust. I don’t know the best way to gauge real estate prices, but tracking owners’ equivalent rent creates a distortion.

Toys: Manufacturing has been outsourced to lowest cost parts of world, hence prices have plummeted.

Wireless Services, Software, TVs: Technology prices benefit from two key factors: the technology adoption lifecycle and manufacturing economies of scale. The long and short of it is that as new products enter the mass market they move down the unit-cost scale, from quirky one-off devices to cheap commodity goods. Think about the first flat screen televisions at more than $10,000 plus; versions that are as good or better than those now cost $500.

So what might we conclude from looking at the chart’s component parts? Maybe only that it’s a little easier to see why the Fed has been having a hard time getting inflation to rise. While some prices are indeed up, many powerful forces have driven other prices lower — and these are forces that the Fed can’t easily influence. Until there is a substantial and sustained increase in wages (or a huge drop in the dollar), inflation may very well remain below the Fed’s 2 percent target for a long time to come.

Originally: Why Gauging Inflation Is So Hard

What's been said:

Discussions found on the web: