Last week, we compared monetary vs fiscal stimulus. Understanding the differences in how each manifests in the economy is crucial to understanding so many other issues. The biggest one lately concerns rising prices and how the FOMC might act to reduce inflation.

This complicated subject should not be oversimplified.

The Fed has been contemplating two distinct policy goals: 1) Getting off of the emergency footing they have been on for so long — arguably, long after the Great Financial Crisis (GFC) ended and now after the pandemic emergency 1 is over; and 2) Reducing inflation.

Fighting inflation during the past decade was pretty easy — the Fed was more concerned with disinflation or outright deflation. But getting off of the emergency footing has proved to be more difficult, in large part because of the lack of a robust fiscal response post-GFC. It was as if the Fed was working towards full employment with one hand tied behind their back.

The “Mostly Monetary Response” can be rightly blamed for widening the wealth gap between the rich and everyone else. But do not ignore the impact this had on the Fed’s subsequent actions. A fiscal-free alternative made raising rates into the weak recovery 2009-2015 undesirable, possibly risking a recession. This is not a case of hindsight bias but something I have been kvetching about since 2009.

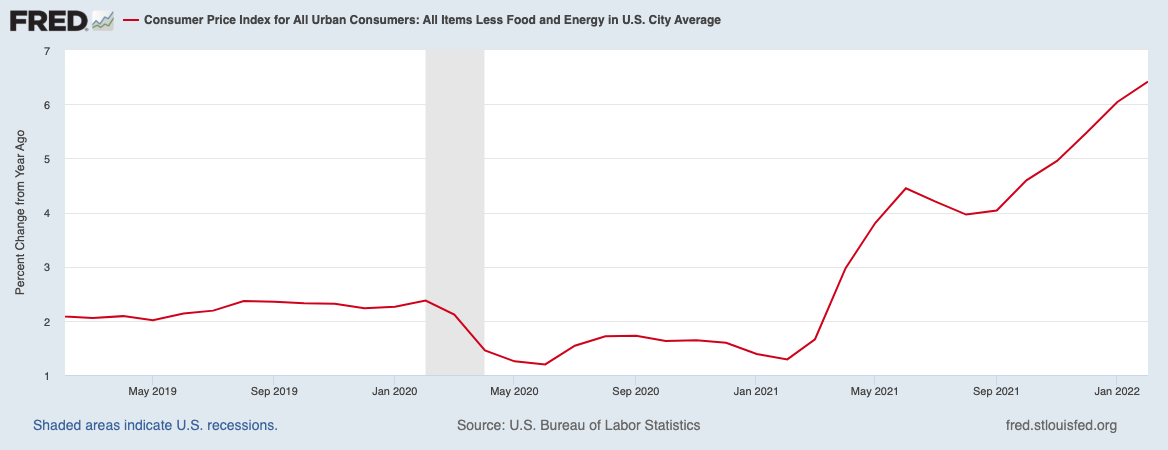

This long-term, macro framework explains in part why the FOMC was stuck — unable to normalize Fed Fund rates or at least get over 2% on a sustained basis. It also explains why the Fed views inflation as transitory — it’s caused by a unique set of pandemic circumstances that are likely to pass, albeit over a longer than expected period of time.

When we consider what were the key drivers of inflation before the war began, we see mostly one-off issues related to the pandemic: huge fiscal stimulus via the CARES Acts; consumer behavior during lock-down; the release of pent-up demand upon re-opening. Before Russia’s invasion of Ukraine, inflation was rising and most of the aspects of the price increases were due to factors beyond the Fed’s interest rates:

-Sudden increase in demand for goods over services caused by lockdown;

-Supply chain logistical issues;

-Too few cargo ships, not enough physical shipping containers;

-Not enough dock workers for major ports;

-Too few truck drivers;

-Massive fiscal stimulus; 2

Now we have a war raging, crude oil, natural gas, and energy supplies have surged, nickels and other metals have skyrocketed. Are any of these responsive to Fed rates in the present environment?

Alex Gurevich’s most recent book, “The Trades of March 2020: A Shield against Uncertainty” points out that while the Fed might occasionally surprise the market with rate cuts, they never surprise the market with unexpected increases,3 preferring to telegraph those to prevent increase market turmoil and volatility. The pundits calling for bigger and more increases seem to be missing this point.

The Fed wants to get off of its emergency footing. They are jawboning against inflation, but they understand exactly how ineffectual increases are in the current environment.

I would like to see the FOMC return to a more normal footing — eventually — but those expecting fast, fat, and frequent rate hikes might be setting themselves up for disappointment.

Update: March 15, 2022

For a counterpoint to my sanguine view of inflation, see Jeanna Smialek in today’s New York Times:

Powell Admires Paul Volcker. He May Have to Act Like Him. The Federal Reserve is facing the fastest inflation most Americans have ever seen. Its chair says policymakers will do what it takes to tame prices.

Previously:

Comparing Stimulus: Monetary vs Fiscal (GFC vs C19) (March 11, 2022)

Transitory Is Taking Longer than Expected (February 10, 2022)

Long Time ‘Coming (November 17, 2021)

Deflation, Punctuated by Spasms of Inflation (June 11, 2021)

Stimulus, More Stimulus and Taxes (January 25, 2021)

Go Big: The U.S. Needs Way More Than a Bailout to Recover From Covid-19 (April 30, 2020)

________

1. Not the pandemic itself but the economic emergency it caused.

2. As to the fiscal stimulus, most of that pig is through the python, as Net Saving have fallen back to near pre-pandemic levels.

2. At least not since 1994.