Around the world, markets lost 5% or worse just last week. Year to date, the S&P 500 is down more than 23%; the Russell 2000 small caps are off more than 26%; Emerging markets are down almost 28%; and the Nasdaq Tech index is off more than 31%.

All jokes aside, September has lived up to its reputation as a challenging month for equities. After the brutal sell-off, a relief rally was due, hence the green on your screen this morning.

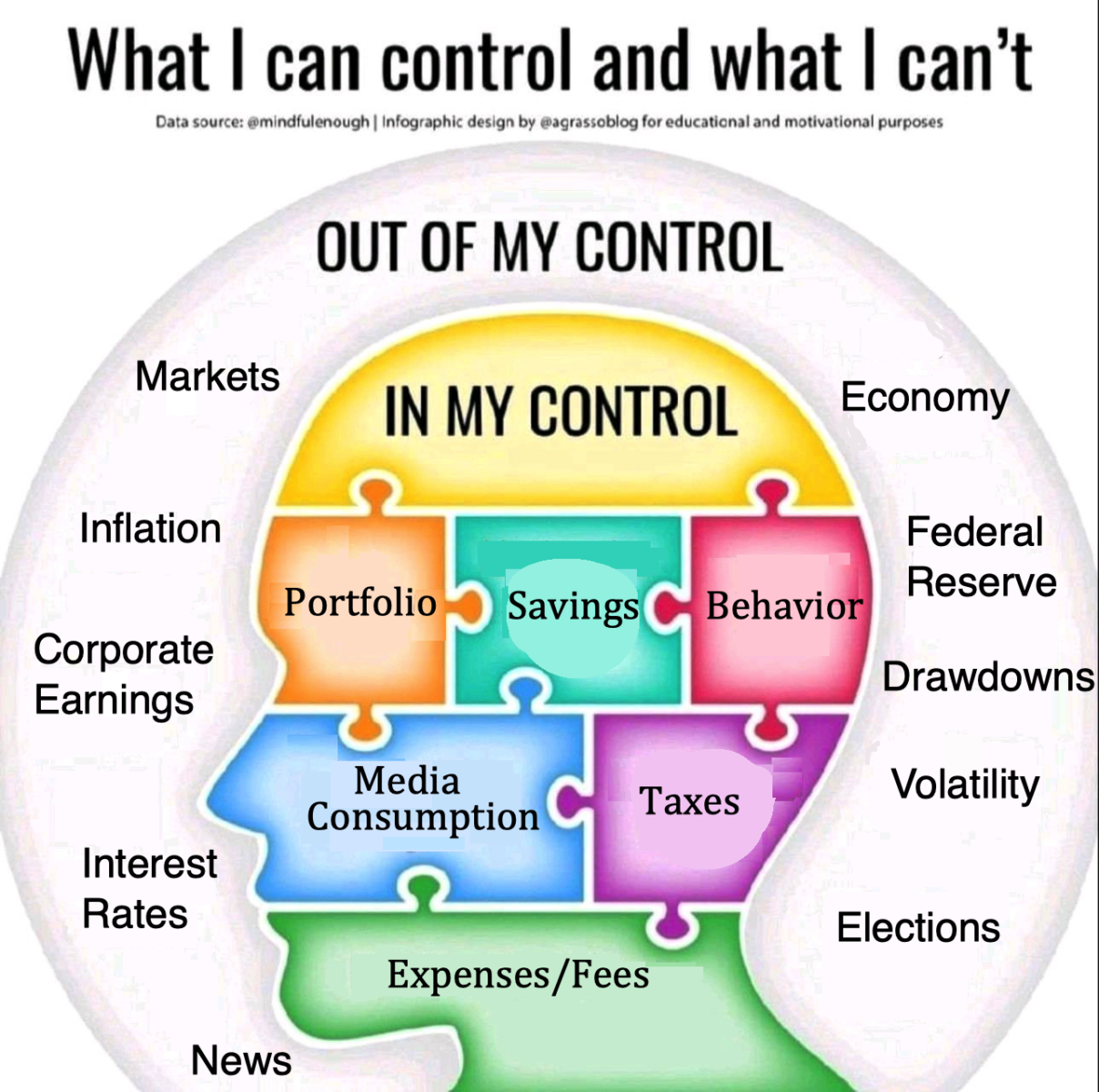

I am often asked about how market action affects me — my psyche, emotions, and behavior. The short answer is very Zen: I understand what I can and cannot control, and then adjust accordingly.

Consider this tweet I bookmarked back in August; This updated version, via Mindfulenough, gave me the idea to turn it into something investment-related.1 Hence, the infographic you see above is my attempt to create a visual of my usual writing (hence, why I am a scribe and not an artist).

Let’s discuss that Zen-like approach of recognizing what is actually within your control and what things you have absolutely no say over their outcomes. It is noteworthy that most of what we talk about, read, listen to and watch on video are those things out of our control.

What is NOT in your control:

Markets: First and foremost, you have zero control over the markets. None whatsoever. Your buying and selling is a few thousand or even a few million dollars worths of stocks do not impact the trillion dollar capital markets, They will do what they do regardless of your puny existence.

Economy: GDP, Hiring & Wages, Consumer Spending, Industrial production, Home building, and on and on goes the list. As one of 330 million people, your spending is not even a rounding error.

Do I need to continue? You might contribute to Inflation, but its infintesimel; you surely have zero influence with the Federal Reserve or Interest Rates. The iPhone you just bought? It’s not going to impact Corporate Earnings one bit. Similarly, you have de minimus effect on Volatility or Drawdowns,; surely, you have zero impact on what gets reported in the News, nor will you determine the outcome of National or Local Elections.

What is in your control:

Your Portfolio: You want to create something robust enough to withstand drawdowns and recessions; not necessarily the best possible set of assets but the ones you can live with day in and day out. This means it must be suitable for the amount of Risk you are comfortable with. This includes a broad Asset Allocation including full Diversification of asset classes, geographies, etc. You must have a Financial Plan, so it is clear what you are investing for, and so you can see how you are progressing towards those goals.

You must Save enough money relative to your income by living within your means. You can control your Taxes, by planning your stock selling using a variety of methods that minimize what you pay (the guidelines the IRS has established is very helpful with this but you should consult a professional to do this properly). You can minimize what you pay in Fees and Expenses (It doesn’t take much to swap out expensive funds for cheaper ones);

What news media you consume is also within your control – are you reading too much uber bearishness? The Cult of Fed Haters? ZH? These are likely affecting your outlook in a negative way.

It all comes down to the single most important thing that is within your control: your own Behavior. If you can master that, it is almost impossible not to succeed as a long-term investor.

_____________

1. via the site (and Etsy shop and Instagram account) Mindfulenough.

What is NOT in your control:

1. Markets

2. Asset Economy

3. Inflation

4. Federal Reserve

5. Corporate Earnings

6. Volatility

7. Interest Rates

8. Elections

9. News

10. Drawdowns

What is in your control:

1. Portfolio

2. Asset Allocation

(Diversification)

3. Savings

4. Financial Plan

5. Taxes

6. Behavior

7. Expenses/Fees

8. Risk

9. Rebalancing

10. Media Consumption