My colleague Ben Carlson asked the question “Why Isn’t Inflation Falling?” There are some technical explanations, but before we get there, a quick reminder as to how we got here:

The global pandemic forced governments around the world to shut their economies down; everything was closed, from schools to businesses, restaurants, entertainment venues, retail stores, and offices. It was a desperate way to stay ahead of a deadly disease we had little understanding of at the time. Eventually, we figured out that vaccines and masking could help us manage the worst of this.

We fast-tracked vaccine approval and passed the largest fiscal stimulus in US history – 10% of GDP for CARES Act I. We rode out the pandemic at home, doing our best via Zoom and Teledoc, Pelotons and Netflix. We shifted our consumption habits from services to goods; quite a few of us bought homes and moved out of dense cities. Global manufacturing systems and supply chains proved inadequate to handle the surge in demand.

Hence, a spike in inflation in 2021, accelerating into 2022.

Once herd immunity was achieved, the world began to slowly re-open, dare I say normalize? Many prices began to come back down to earth: Lumber, Copper, USed Cars, Gasoline, Oil, Nat Gas, Sugar, Beef, Avocados, even Chicken Wings fell substantially from their peaks. Some commodities, like Lumber, returned to pre-pandemic levels.

Yet as Ben pointed out, the past 7 monthly inflation prints (annualized) have ranged from 8.2% to 9.1%. There is no sign Consumer Price Indices prices are rolling over. (Claudia Sahm points out PPI has peaked but it still remains elevated). “Transitory” still looks more like wishful thinking — and I am on team transitory.

What gives?

As it turns out, a technical aspect of how CPI is assembled is a large part of the reason. It is an oddity of how BLS assembles its CPI model, trying to figure out how to measure shelter which is both a cost and for millions of homeowners, an asset. Understanding this will help you understand why inflation appears to be so sticky, despite a huge swath of falling prices.

The data suggests that many Goods prices, while greatly elevated over pre-pandemic levels, are no longer rising; indeed, many have fallen dramatically. Inflation does seem to have peaked, as far as Goods are concerned.

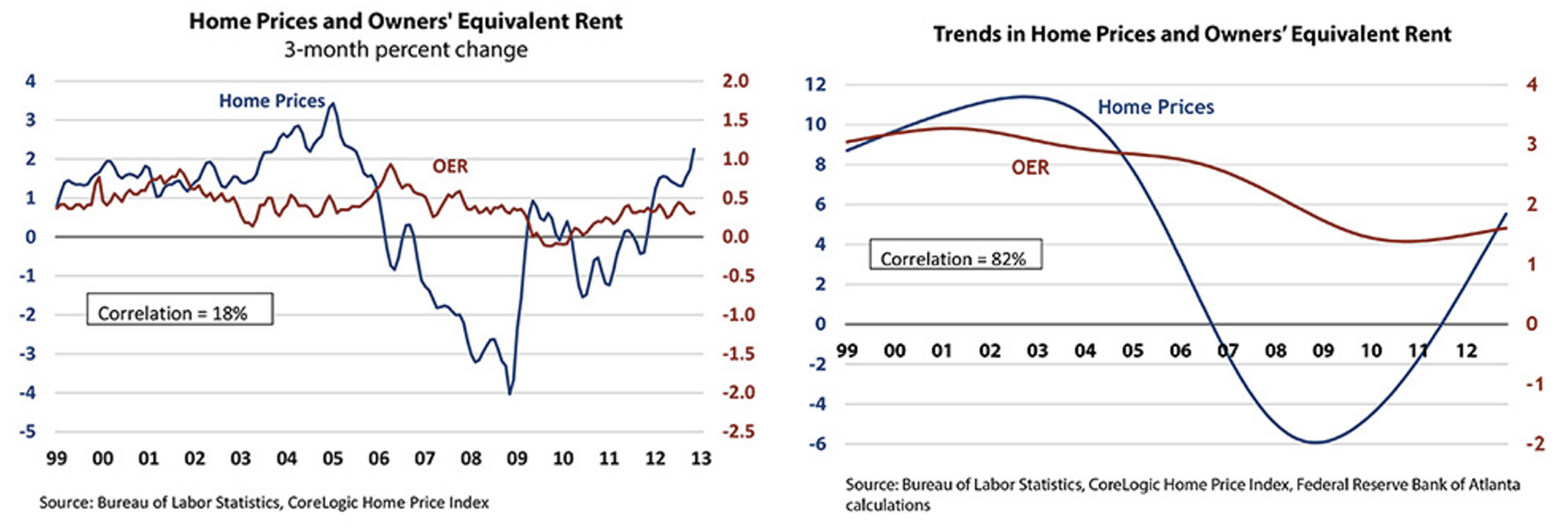

That leaves Services. The largest part of Services is Shelter (by far). Indeed, it is the largest component of CPI, accounting for 32% of the index and ~40% of Core CPI. It is calculated via a complex model called Owners’ Equivalent Rent (OER).

It does not operate the way you might imagine:

“Home prices do not directly enter into the computation of the CPI (or the personal consumption expenditures [PCE] price index, for that matter). This is because a home is an asset, and an increase in its value does not impose a “cost” on the homeowner. But there is a cost that homeowners face in addition to home maintenance and utilities, and that’s the implied rent they incur by living in their home rather than renting it out. In effect, every homeowner is his or her own tenant, and the rent they forgo each month is called the “owners’ equivalent rent” (or OER) in the CPI.”

-Mike Bryan and Nick Parker, MacroBlog, Atlanta Federal Reserve

This model oddity has had huge effects on inflation over time. Note the issue with OER is not a new phenomenon, and the research note1 above was from 2013.

I first began discussing the impact of rental costs on CPI during the run-up to the financial crisis in the mid-2000s. As more people bought homes, real estate prices skyrocketed, and fewer renters meant rental prices fell. In the pre-GFC 2000s, rapidly rising home prices — driven largely by reckless lending practices and rapidly falling mortgage rates.– led to CPI appearing lower than inflation actually was.

It seems perverse, but that is what happened.

Today, we are dealing with a bizarre inverse variation of that situation. Home prices are rising, in part due to a lack of inventory but exacerbated a great deal by rapidly rising mortgage rates. Those rates are driven primarily by the FOMC action. The combination operates to price many potential buyers out of the market. But you gotta live somewhere, and so these buyers are forced to stay (or become) renters.

There is a simple truism at the heart of sticky CPI inflation readings:

Higher Fed Funds Rates & Mortgage Rates = Rising OER & CPI

At least, that is how it seems to be operating this cycle.

This leads us to the very perverse conclusion that as the Federal Reserve attempts to fight inflation by raising interest rates, it has led to higher CPI inflation each month, even as prices of goods have come down.

Even worse, the FOMC seems to be relying on the CPI to determine when to stop raising rates, even as they themselves drive those monthly CPI prints higher.

Rental prices are complex to model, and their calculations are not as simple as surveying a variety of landlords. Instead, it is tied to home prices, along with other factors in OER sub-model. The Bureau of Labor Statistics and the Cleveland Fed are aware of this anomaly. A recent research paper notes:

“Prominent rent growth indices often give strikingly different measurements of rent inflation. We create new indices from Bureau of Labor Statistics (BLS) rent microdata using a repeat rent index methodology and show that this discrepancy is almost entirely explained by differences in rent growth for new tenants relative to the average rent growth for all tenants. Rent inflation for new tenants leads the official BLS rent inflation by 4 quarters. As rent is the largest component of the consumer price index, this has implications for our understanding of aggregate inflation dynamics and guiding monetary policy.”

-Brian Adams, Lara Loewenstein, Hugh Montag, and Randal Verbrugge

The good news is the research arms of the Fed and the BLS are aware of this modeling problem and seem to be taking steps to address it. The bad news is, I see no evidence that the Federal Reserve itself has recognized its own role in this inflation complexity.

In the wonderful world of economic modeling, despite falling prices, CPI has remained persistently higher, and we must consider the role of the Federal Reserve as part of the reason why.

Would you have ever guessed that Jerome Powell would turn out to be one of the biggest agents of Inflation?

See also:

Why Isn’t Inflation Falling? (Ben Carlson, October 21, 2022)

Why the government took home prices out of its main inflation index (Timothy B. Lee and Aden Barton, May 11, 2022)

You Say You’re a Homeowner and Not a Renter? Think Again. (Mike Bryan and Nick Parker, Atlanta, Fed, March 11, 2013)

Previously:

Why Is the Fed Always Late to the Party? (October 7, 2022)

How Everybody Miscalculated Housing Demand (July 29, 2021)

Farewell, TINA (September 28, 2022)

Who Is to Blame for Inflation, 1-15 (June 28, 2022)

Bloomberg: CPI Inflation Data is a “Lie” (September 26, 2007)

Source:

Disentangling Rent Index Differences: Data, Methods, and Scope

Brian Adams, Lara Loewenstein, Hugh Montag, and Randal Verbrugge

US Bureau of Labor Statistics + Federal Reserve Bank of Cleveland, October 6, 2022

https://www.bls.gov/osmr/research-papers/2022/pdf/ec220100.pdf

_________

1. I thought that was important enough when I saw it in 2013 to have mirrored it at The Big Picture