ATM: Using Volatility to Rebalance Portfolios

At The Money: with Liz Ann Sonders, CIO Schwab (March 27, 2024) The past few years have seen market swings wreak...

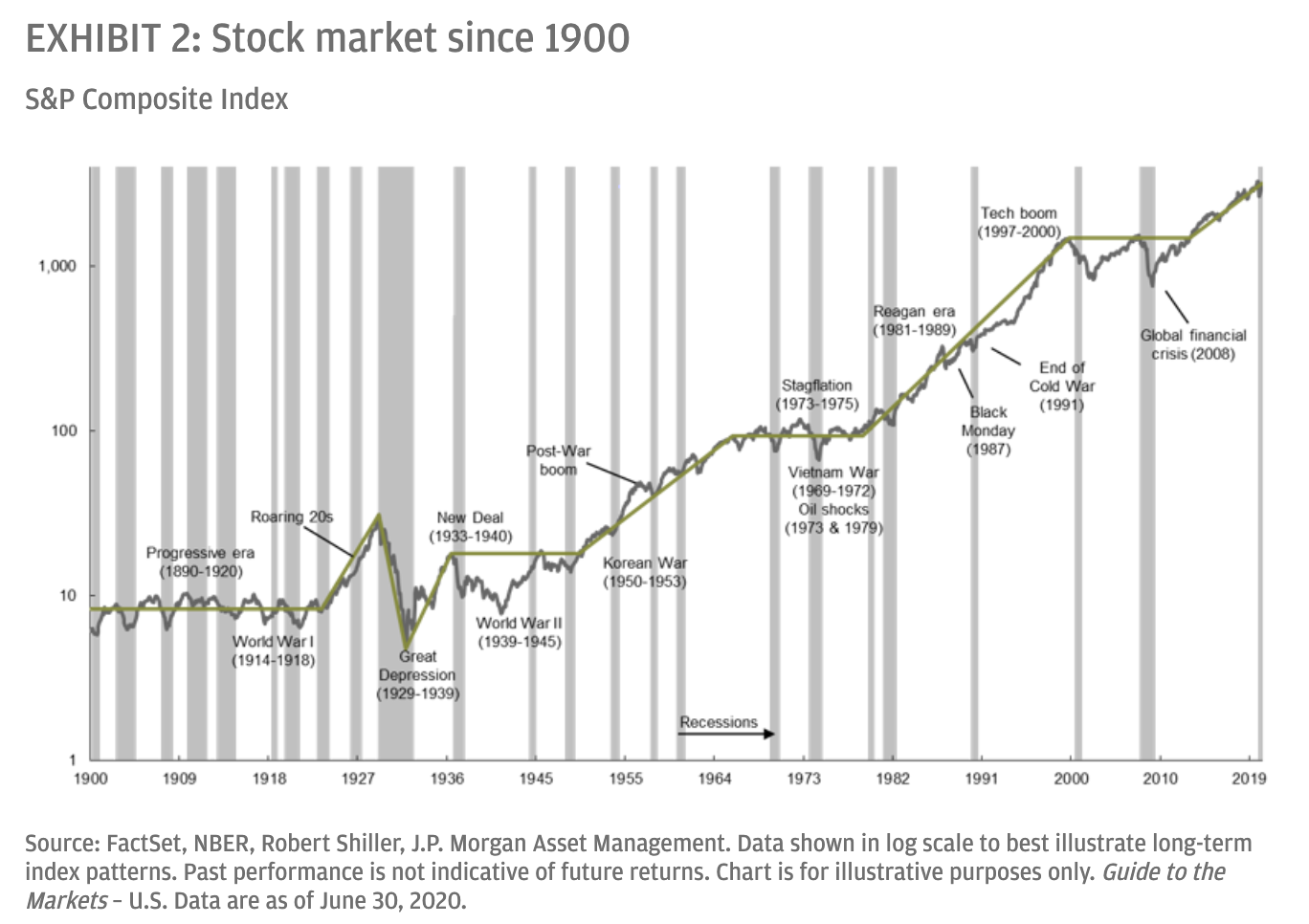

Source: JP Morgan Asset Management The above is one of my favorite charts. This version comes from a JPM discussion on...

Source: JP Morgan Asset Management The above is one of my favorite charts. This version comes from a JPM discussion on...

Can an esteemed professor of finance ever escape his reputation as a “perma-bull?” That was the question running through my mind...

Can an esteemed professor of finance ever escape his reputation as a “perma-bull?” That was the question running through my mind...

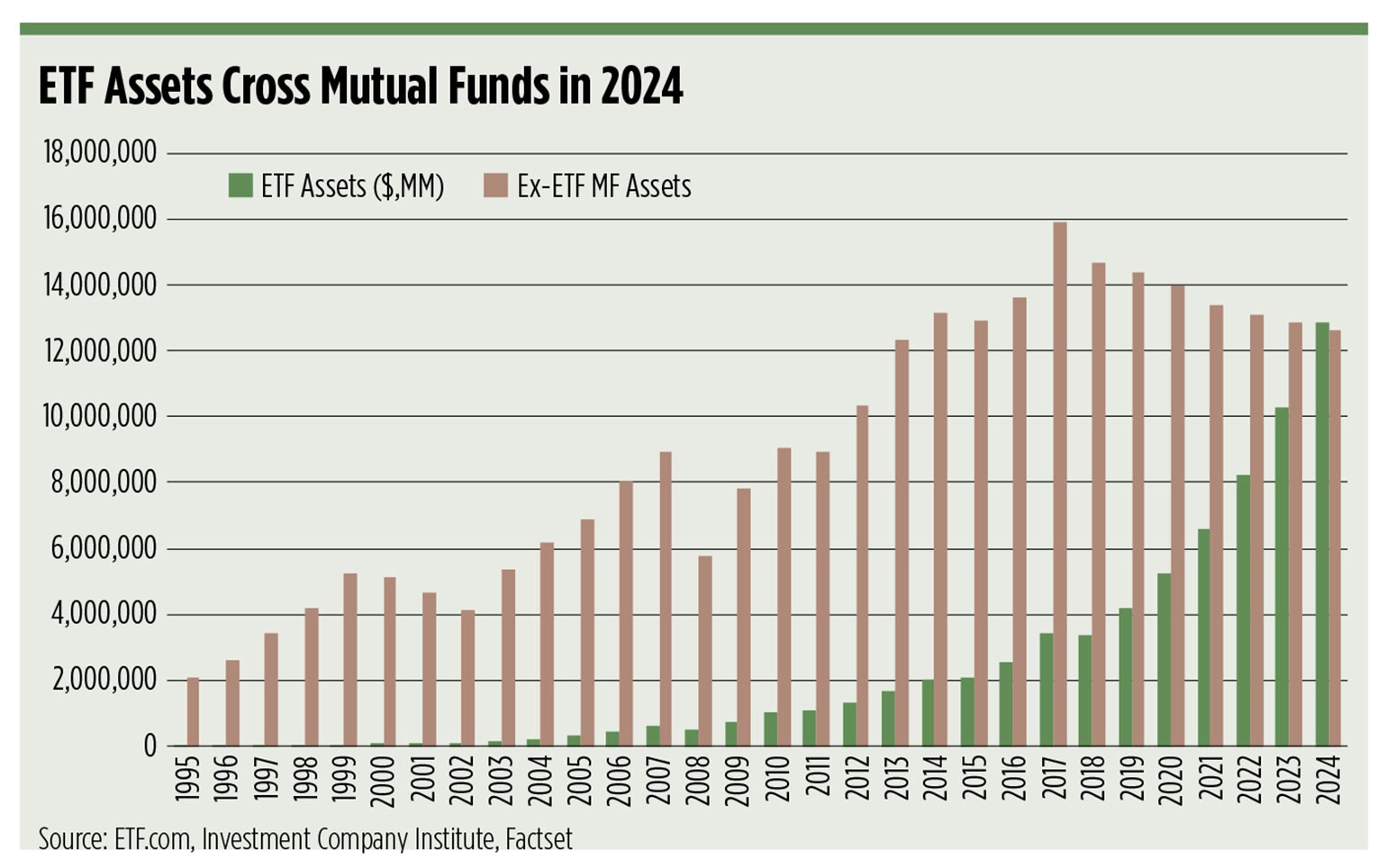

Source: Wealth Management I referenced this Wealth Management column this AM — but it is worth further exploring the...

Source: Wealth Management I referenced this Wealth Management column this AM — but it is worth further exploring the...

Get subscriber-only insights and news delivered by Barry every two weeks.