Smart Beta Performance Isn’t Worth the Cost

The higher fees offset sporadically better returns.

Bloomberg, June 8, 2018

Last summer, we looked at fundamental indexing, which is perhaps better known by the catchy marketing phrase “smart beta.” 1 The practice uses metrics such as book value, earnings and dividend yield to assemble investment portfolios, rather than the traditional indexing methodology based on market capitalization. The goal is to achieve above-market performance.

Before we go any further, a few qualifiers: I agree that passive investing is less passive than many people believe, since the construction of an index does rely on someone, somewhere making a decision about which stocks belong and which don’t. Furthermore, reasonable people can look at the data and amicably disagree.

As fundamental indexing has grown — it has tripled from 2012 to 2017 — it has also drawn closer scrutiny and criticism. I am a soft skeptic of fundamental indexing based on issues of performance, cost and investor behavior.

Costs are easy enough to analyze: according to Morningstar, the expense ratio on the universe of fundamental indexing costs investors about 39 basis points. But there are signs that expenses are coming down. Competition and the embrace by fund companies of loss leaders has exerted downward pressure on expenses. As I noted last year, Vanguard rolled out its version of actively managed factor exchange-traded funds (aka fundamental indexing), with a fee of 13 basis points. Some competitors such as Goldman Sachs’ have upped the ante (or is that lowered?) with funds like the ActiveBeta U.S. Large Cap Equity ETF, which charges just 9 basis points.

Outliers aside, fundamental indexing is still more expensive than old fashioned capitalization-weighted indexing. Costs may be trending in the investors’ favor, but these are still more expensive strategies to manage. The reasons for this are simple: fundamental indexing has more asset turnover and will thus have higher trading costs. One recent AAII study showed a range of turnover from 14 percent to almost 50 percent. 2

Let’s generously ball park the turnovers at 10 percent to 20 percent annually for fundamental indexing versus 1 percent to 2 percent for funds tied to the Standard & Poor’s 500 Index. Over longer holding periods, I expect that cost differential will persist. Keep in mind that expenses are a persistent drag on returns.

Speaking of performance: the lure of fundamental indexing is that it outperforms traditional benchmarks, such as the S&P 500. There is a robust debate as to whether fundamental indexing is capturing anything more than classic Fama-French factors. The classic model looks at factors such as value, size, beta (market-beating returns), quality and momentum as sources of outperformance. We can debate where those gains come from — such as increased risk or reduced liquidity — but the actual performance of factors is understood.

The question for investors is twofold: are the potential gains captured by fundamental indexers worth the extra cost versus factor-flavored products offered by firms such as Dimensional Fund Advisors, Vanguard, Black Rock, State Street and others? And second, once you move from truly passive indexing, do you have the self-discipline to stick with it through both good and bad times? My experience has led me toward the traditional factor investments over smart beta. 3

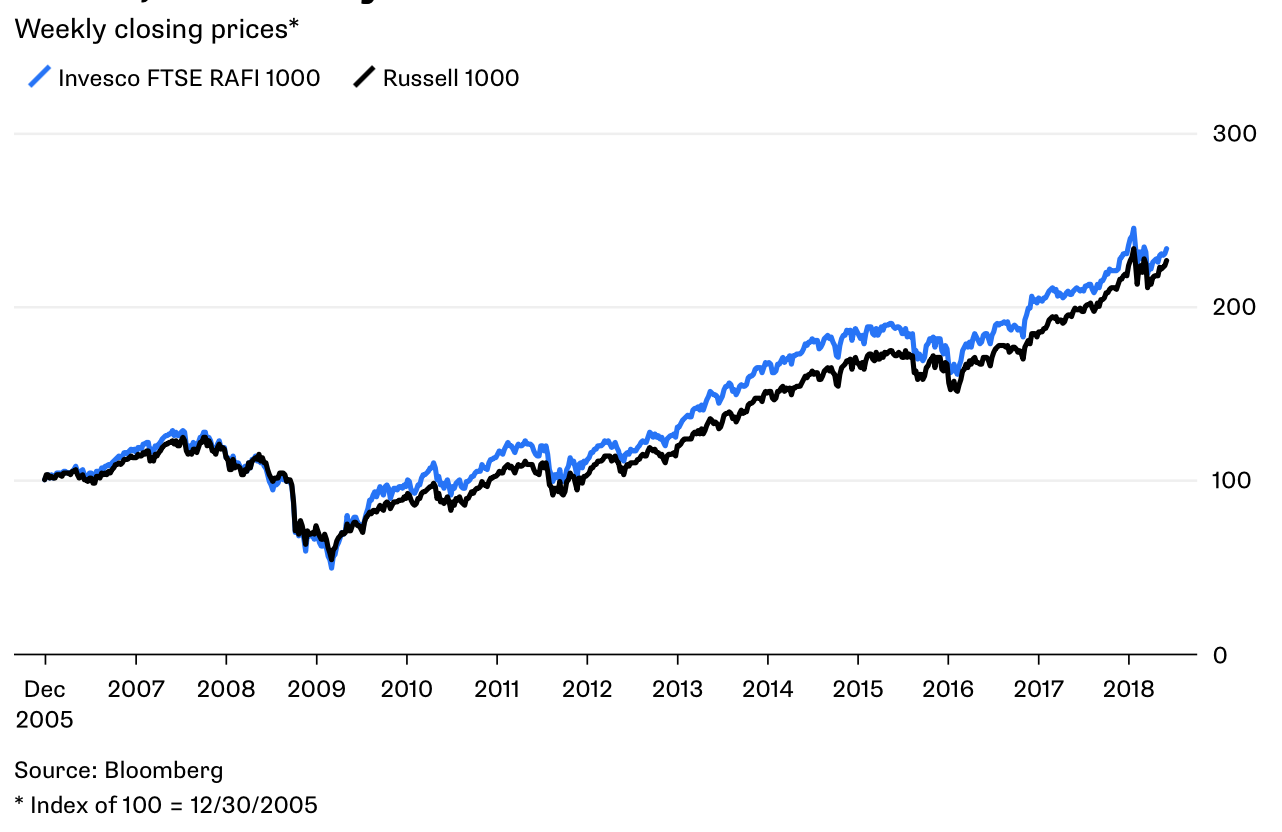

So as an experiment, let’s compare a fundamental index versus its benchmark. This is an exercise fraught with selection bias, so without explaining why, I asked Michael Batnick, the research director for my firm, to choose a typical smart-beta product and its benchmark. He selected the Invesco FTSE RAFI US 1000 Portfolio, which tracks companies based on book value, cash flow, sales and dividends, versus the Russell 1000 Index, which is made up of large capitalization stocks.

From the end of 2005 to the present the FTSE RAFI beat the Russell 1000, but not by very much — and at a cost of 39 basis points. Based on price alone, the FTSE RAFI was ahead by a little more than 6 percent, while the Russell 1000 trailed by just 1 percent based on total return. My best guess is the reason for this is that the companies as a group in the Russell 1000 were slower to recover from the financial crisis and the Great Recession.

Ahead, But Not By Much

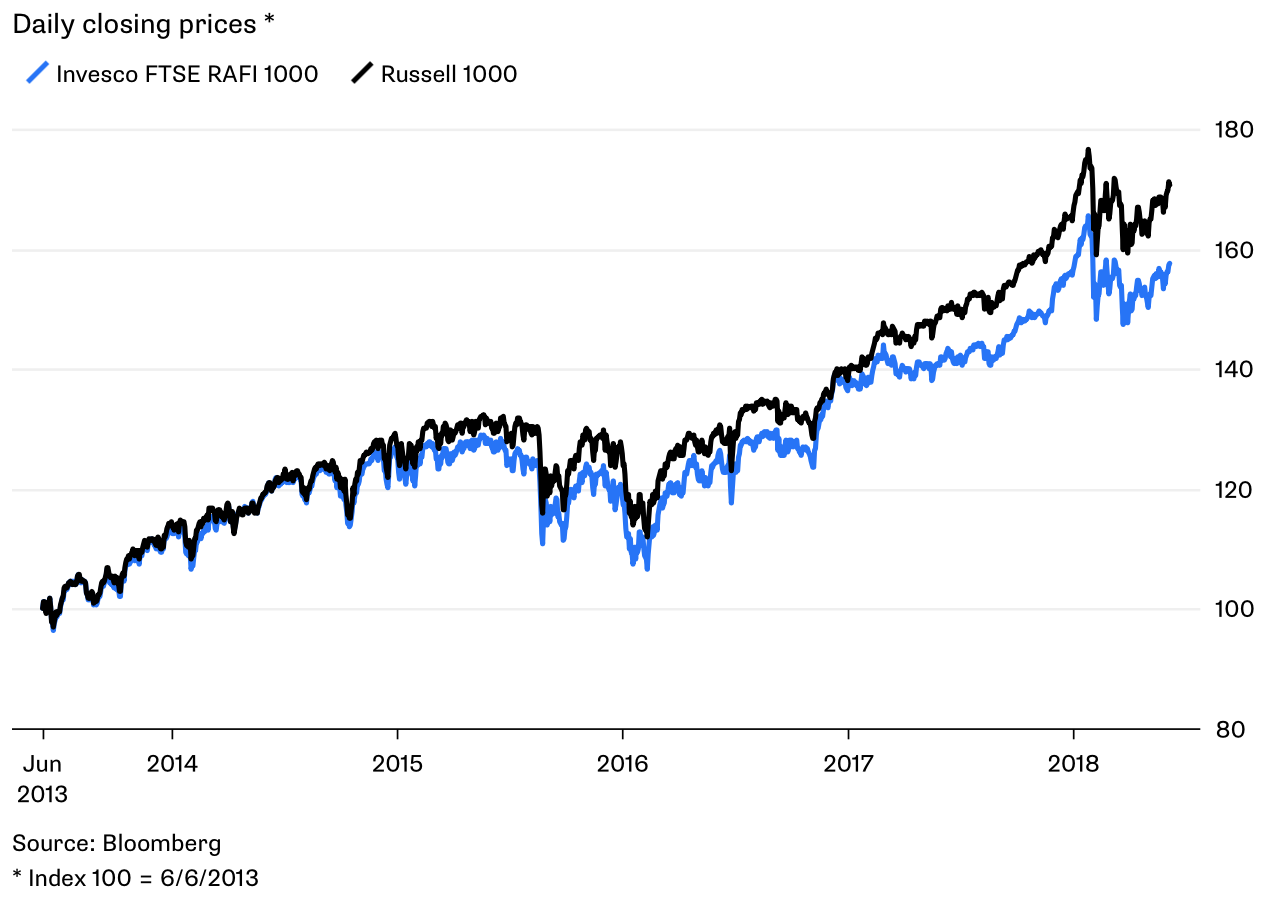

But more recently the Russell 1000 has pulled ahead, and during the past five years it had a total return of 89 percent versus 73 percent for the FTSE RAFI.

Underperformance Anyone?

This gets into another issue, one of behavior, since investors tend to get bored and restless, especially when their holdings lag. Having decided to invest based on a quasi-active strategy, they tend to use underperformance as an excuse to sell current holdings in search of higher returns. Almost always, that is when they make decisions they later regret.

Looking at fund flows during the past decade, we can see how the marketplace is voting. High-cost, actively managed funds have seen trillions of dollars in outflows headed toward low-cost, passively indexed funds. Some of this money has moved toward factor-based investing, and some toward fundamental indexing. I have my preferences, but each is an improvement over paying up for market-beating alpha that never seems to arrive.

_______

1. The quote from Andreas Utermann, global chief investment officer for Allianz Global Investors, which has reached legendary cliché status, is “smart beta is neither smart nor beta.”

2. To be fair, some of the more technical strategies are outliers, with a much higher turnover rate than the rest of the fundamental indexing universe. The Financial Times noted “smart beta indices can be even more active. Indices based on buying the stocks with the greatest momentum can have total turnover of over 350 per cent, whereas another popular variety called “equal weight” has annualized turnover of nearly 50 percent.”

3. I personally own portfolios made up of funds from Vanguard, Dimensional Fund, BlackRock, as do clients of Ritholtz Wealth Management.

Originally: Smart Beta Performance Isn’t Worth the Cost