@TBPInvictus here: Back in December 2022, I hypothesized that Elon Musk’s antics and his newfound desire to own the...

@TBPInvictus here: Back in December 2022, I hypothesized that Elon Musk’s antics and his newfound desire to own the...

Read More

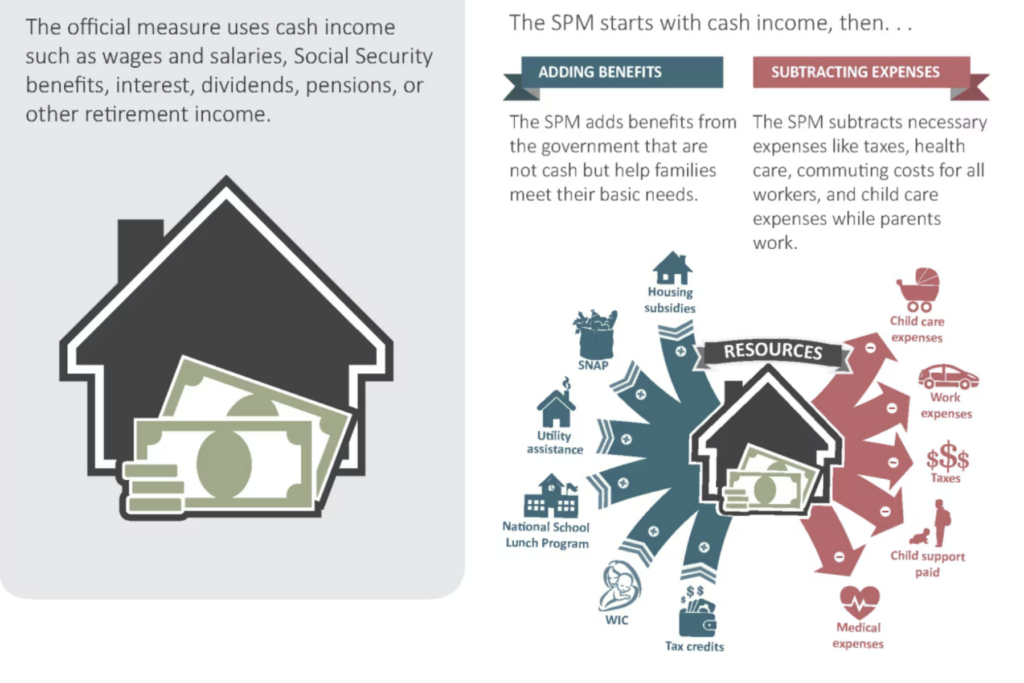

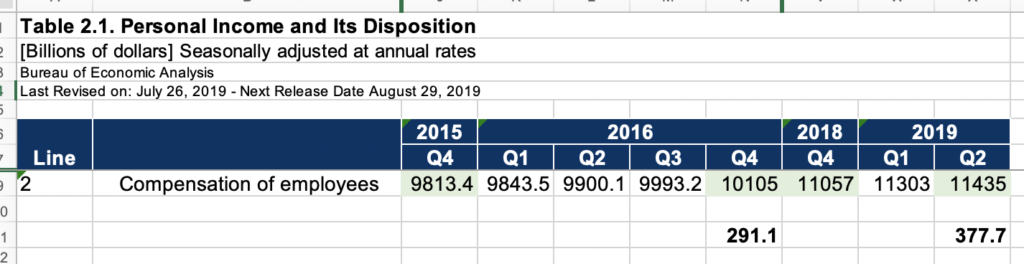

@TBPInvictus here; Let’s cut to the chase: “America’s Enormous Math Mistake” is a popular video on YouTube...

@TBPInvictus here; Let’s cut to the chase: “America’s Enormous Math Mistake” is a popular video on YouTube...

Read More

@TBPInvictus here: Contrary to 40+ years and counting of “trickle down” narrative, the reality is that the gap between...

Read More

@TBPInvictus here. (Also on Post and Mastodon). Happy holidays to all, and the best for 2023. It’s been a hot minute since...

@TBPInvictus here. (Also on Post and Mastodon). Happy holidays to all, and the best for 2023. It’s been a hot minute since...

Read More

@TBPInvictus here: On Presidents Day, it is noteworthy that the current President feels compelled to cap the salaries of those employees...

Read More

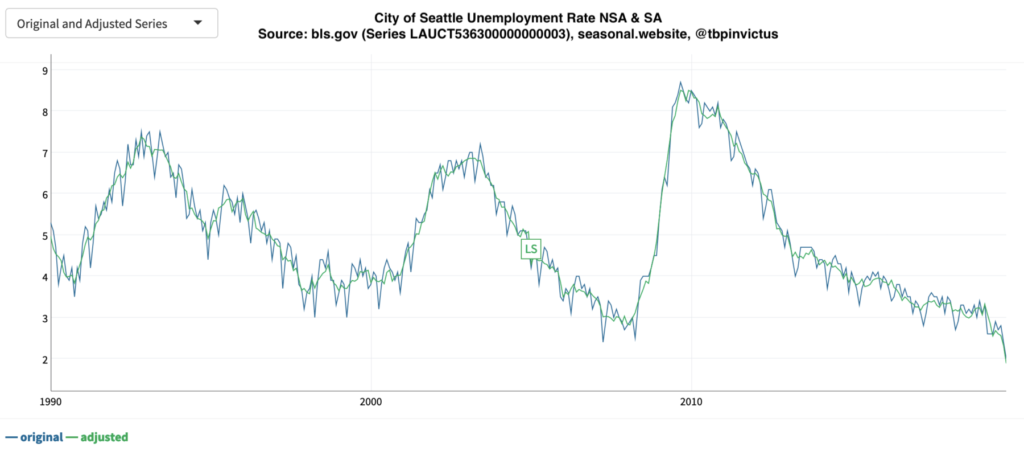

@TBPInvictus here: City of Seattle Unemployment Rate: 1.89% City of Seattle Unemployment Rate, 1.89% (Seasonally Adjusted basis)....

@TBPInvictus here: City of Seattle Unemployment Rate: 1.89% City of Seattle Unemployment Rate, 1.89% (Seasonally Adjusted basis)....

Read More

@TBPInvictus here: Long overdue: My pal David Rosenberg has finally decided to hang his own shingle: Please say hello to Rosenberg...

@TBPInvictus here: Long overdue: My pal David Rosenberg has finally decided to hang his own shingle: Please say hello to Rosenberg...

Read More

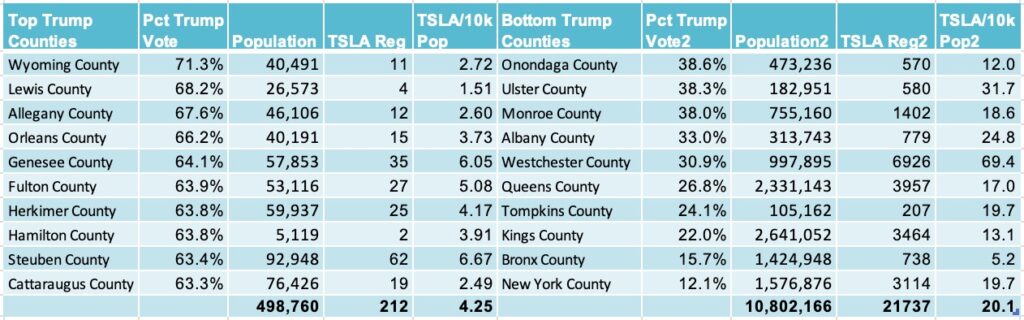

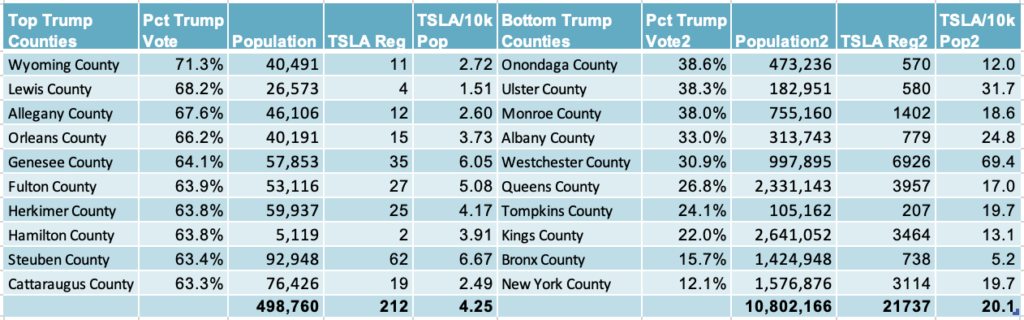

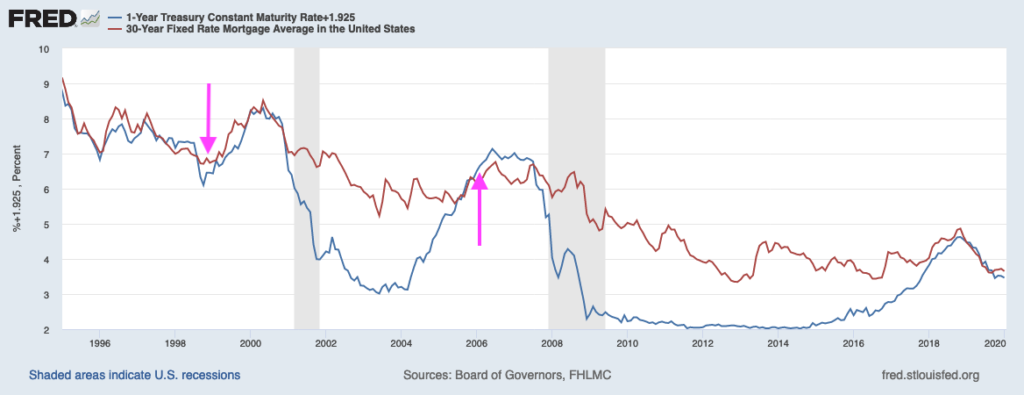

@TBPInvictus here: I want to avoid the usual “false equivalencies” and “both sides do it” approach, and ask a...

@TBPInvictus here: I want to avoid the usual “false equivalencies” and “both sides do it” approach, and ask a...

Read More

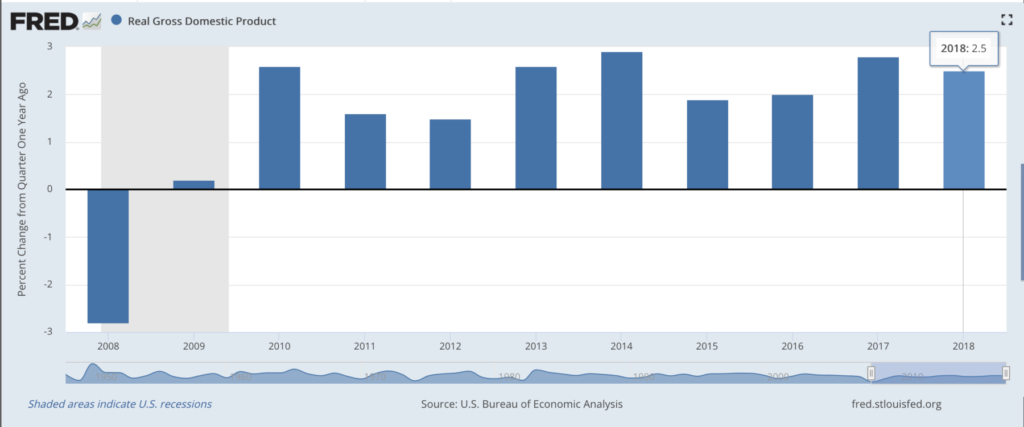

@TBPInvictus here. Real GDP Percent Change from Quarter One Year Ago, Annually, End of Period Source: FRED The Bureau of...

@TBPInvictus here. Real GDP Percent Change from Quarter One Year Ago, Annually, End of Period Source: FRED The Bureau of...

Read More

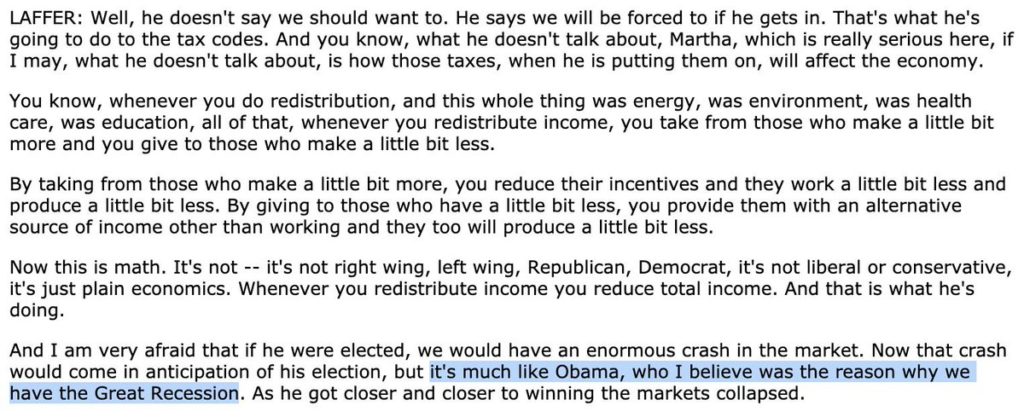

@TBPInvictus here. With Herman Cain and Stephen Moore apparently on life support for Fed slots, looks like Art Laffer is stepping up his...

@TBPInvictus here. With Herman Cain and Stephen Moore apparently on life support for Fed slots, looks like Art Laffer is stepping up his...

Read More