Monetary Policy Renormalization

Narayana Kocherlakota | President

Federal Reserve Bank of Minneapolis

Philadelphia Fed Policy Forum – The New Normal for the U.S. Economy

December 4, 2015

Note*

There has been a great deal of public conversation about the onset of what is called “monetary policy normalization.” The website of the Board of Governors of the Federal Reserve System defines “monetary policy normalization” as the process of raising the fed funds rate and other interest rates to more normal levels and reducing the size of the Federal Reserve’s securities holdings.1 This definition leaves unstated what kind of strategic framework will guide the Federal Open Market Committee’s (FOMC’s) decisions about the target range for the fed funds rate and the size of the balance sheet. However, at least to my ears, the term “normalization” connotes that the FOMC is aiming to return to a strategic framework that closely resembles the one used prior to the financial crisis. In this talk, I argue that the FOMC would be better served by instead turning to a different strategic framework. My argument unfolds with three points.

First, I provide a characterization of the FOMC’s pre-2008 policy framework. Many observers have noted that this framework was largely grounded in the Taylor Rule.2 I argue that the Taylor Rule requires the central bank to tolerate persistent inflation and employment shortfalls in order to limit deviations of the fed funds rate from historically normal levels.

Second, I use the public record to document that, as of late 2009, the FOMC felt that it would be appropriate to use its monetary policy tools to foster a relatively slow recovery in both prices and employment. (The recovery that actually unfolded was slower than the FOMC intended in terms of employment, but close to the FOMC’s intentions in terms of inflation.) I argue that the FOMC’s guarded response can be traced back to its pre-2008 policy framework—that is, to the Taylor Rule. Indeed, because of this baseline “normal” policy framework, the FOMC and many outside observers actually saw the Committee as pursuing a highly accommodative policy.

Third, motivated by these observations, I suggest that the FOMC should change its “normal” policy framework. I recommend that the Committee adopt a more goal-oriented approach, in which the level of accommodation is highly responsive to the FOMC’s medium-term forecasts of inflation and output gaps. This change would engender better economic outcomes, especially in response to severe adverse shocks.

The views that I express today are my own and are not necessarily those of others in the Federal Reserve System. I note too that I intend to recuse myself from the December FOMC meeting, given that it takes place so close in time to my last date as president (December 31, 2015).

Point 1: An Aversion to Large Policy Responses

I begin by examining the FOMC’s pre-2008 framework. Many observers have argued that this framework is well-modeled by versions of the Taylor Rule. My first point is that such a framework requires the FOMC to tolerate inflation and output gaps in order to limit deviations of the fed funds rate from its historical average.

To understand my point, consider the following scenario. Suppose that inflation is currently 1 percent and the output gap is currently -2 percent. Inflation is expected to rise back to 1.5 percent over the next two years, and the output gap is expected to rise back to -1 percent over the same time frame. In this scenario, the Taylor Rule—as originally parameterized by Taylor (1993)—would imply that the FOMC should target a fed funds rate of 2.5 percent.3

But such a policy choice does not deliver an optimal outcome when judged through the lens of the FOMC’s dual mandate. The FOMC can reduce both anticipated inflation and output gaps by lowering the fed funds rate still further. Implicitly, the Taylor Rule requires the FOMC to tolerate anticipated inflation and output gaps in order to keep the fed funds rate from falling too far low below its historical norms.

The tolerance of projected output and inflation gaps embedded in the Taylor Rule can be justified by appealing to a central bank’s desire to limit the variability of the short-term interest rate around its long-run level. For example, Taylor and Williams’ (2010) elegant theoretical analysis of simple interest rate rules evaluates those rules using an objective function that penalizes interest rate variability.4 Without such a penalty, an optimal interest rate rule would mandate a considerably larger response to the FOMC’s best available forecasts of the twin shortfalls in inflation and employment. (In a simple New Keynesian model, the response is literally infinite—see Boehm and House 2014.5)

So, that’s my first point: The FOMC’s pre-2008 framework is generally thought to be well-described by the Taylor Rule. The Taylor Rule systematically requires the FOMC to tolerate inflation and output gaps to constrain deviations in interest rates from their long-run level.

Point 2: The Pre-2008 Framework Mandated a Slow Recovery

My second point is that, in late 2009, the FOMC felt that it was appropriate to use monetary policy so as to foster a slow recovery in both prices and employment. I argue that the FOMC’s cautious approach was grounded in the “gap tolerance” that was embedded in its pre-2008 policy framework.

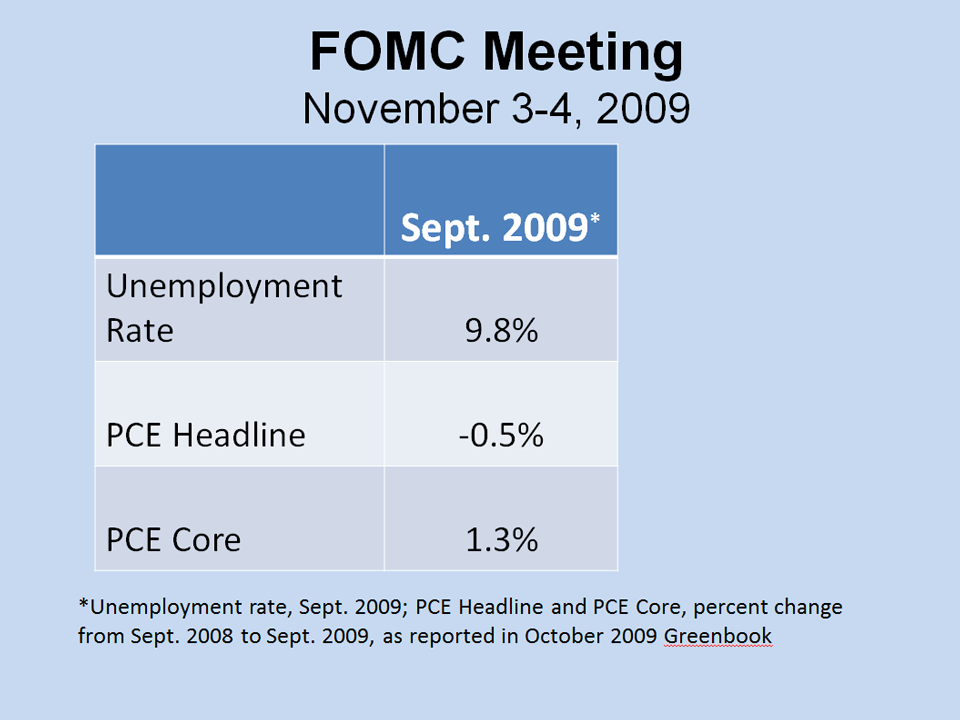

To make this point, I go back to the November 2009 FOMC meeting. This was the third meeting after the Great Recession ended in June 2009. But it was the first meeting during the recovery at which the FOMC submitted projections for the evolution of key macroeconomic variables. With the release of the complete meeting transcript earlier in 2015, the public was able to see the details of these projections.

I should note too that November 2009 was also my first FOMC meeting, so I certainly bear my share of responsibility for any Committee actions or inactions.

It is useful to recall the state of the macroeconomy according to the data available to the FOMC at its November 2009 meeting. Thanks in no little part to the efforts of the Federal Reserve, financial markets had stabilized considerably from the turmoil of the preceding year. As well, the Committee knew that the economy had returned to growth in the second half of the year. However, the unemployment rate was still rising—it hit 9.8 percent in September 2009 (the last reading available before the November meeting). The latest 12-month trailing measure of core PCE inflation was 1.3 percent; the same measure of headline PCE inflation was negative.

In late 2009, both prices and employment were clearly too low relative to desirable levels. What kind of recovery did the Committee seek to achieve so as to fulfill its congressional dual mandate?

We can find the answer to this question in the economic projections for inflation and unemployment submitted by FOMC participants. It is important to understand what these so-called projections actually are. The future evolution of inflation and unemployment of course depends on the future evolution of monetary policy. Each participant’s forecast is based on what that participant sees as being appropriate monetary policy. There is no reason that a participant’s particular view of appropriate monetary policy should line up with his or her forecast of what the Committee will actually do. Hence, these so-called projections should not be seen as a participant’s forecast for the actual course of the economy. Rather, a participant’s projection is best viewed as a description of his or her goals for the evolution of inflation and unemployment.

Seventeen FOMC participants submitted projections in November 2009. The median projection for the unemployment rate in the fourth quarter of 2012—three years later—was 7 percent. Obviously, this is well below 9.8 percent. But it is also well above the participants’ median estimate of the long-run unemployment rate of 5 percent. Participants perceived a relatively slow recovery in the unemployment rate as being appropriate.

Why wasn’t the FOMC willing to do more to help the labor market? One natural answer to this question is that the Committee was concerned about creating unduly high inflation. But the median projection for the PCE inflation rate (core or headline) over the course of 2012 was only 1.5 percent—still well short of the FOMC’s then informal6 inflation target of 2 percent. Only three participants saw an inflation rate of 2 percent or higher in 2012 as being appropriate. Only one participant saw it as appropriate for PCE inflation to slightly overshoot 2 percent in order to help speed the rate of recovery in the labor market.7

I should note that the actual labor market recovery ended up being considerably worse than what the FOMC desired. The unemployment rate was 7.8 percent at the end of 2012, not 7 percent. And the labor force participation rate fell by a lot more from 2009 to 2012 than the FOMC’s staff (or anyone else) expected. In contrast, the FOMC’s choices did achieve a path of inflation close to (and arguably better than) its November 2009 objectives.

Why was the FOMC aiming for such a slow recovery toward its dual mandate goals? One possibility is that the FOMC saw itself as being unable to provide additional accommodation in November 2009. But the evidence from the November 2009 meeting does not support this hypothesis. The staff’s baseline projection at the meeting was that the Committee would choose to initiate liftoff when the unemployment rate was above 8 percent and the one-to-two-year-ahead outlook for the inflation rate was 1.4 percent. It was certainly possible for the FOMC to adopt a policy stance that would defer liftoff until economic conditions had improved more. (Indeed, the FOMC did adopt exactly such a policy stance later in the recovery.) Yet, in the participants’ discussions of their projections, only one person8 suggested that it might be appropriate for monetary policy to be easier than in the staff baseline.

So the FOMC was not forced to pursue a slow recovery because of constraints on its tools. Rather, the FOMC chose to pursue a slow recovery. In my view, this choice can be traced back to the Committee’s reliance on the Taylor Rule as a key baseline in its thinking. As we have seen, the Taylor Rule is specifically designed to constrain the response of the central bank’s target interest rate to inflation gaps and output gaps. Qualitatively, a desire for low interest rate variability would have important consequences for the FOMC’s perspectives on appropriate monetary policy in late 2009. To achieve a faster recovery, the FOMC would need to add more accommodation and/or slow the pace of its eventual removal of accommodation. Either option would increase the deviation between the time path of accommodation and its eventual long-run level.

The October 2009 Greenbook provides a more quantitative sense of how the Taylor Rule restricts the pace of economic recovery. In formulating its outlook, the staff assumed that, after (a delayed) liftoff in early 2012, the Committee’s future fed funds rate target choices would follow a rule that was close to that originally proposed by Taylor (1993).9 Given this model of Committee behavior, the staff’s outlook was that the unemployment rate would remain above its long-run level for nearly four years. The projected recovery was even slower with respect to inflation: It was expected to remain at or below 1.6 percent for at least the next five years.

To summarize: In the wake of the Great Recession, the FOMC and its staff treated the pre-2008 policy framework—that is, the Taylor Rule—as an important baseline. As we have seen, the Taylor Rule is grounded in an implicit penalty on deviations of short-term interest rates from their long-run levels. Because of that penalty, the rule required the Committee to seek a slow recovery in its dual mandate variables in order to return the short-term interest rate closer to its long-run level more rapidly. Put more bluntly, the Taylor Rule required the Committee to forgo the timely creation of hundreds of thousands—perhaps millions—of jobs in order to get interest rates back up to normal more rapidly.

Point 3: Toward a Better Reaction Function

I’ve argued that, in November 2009, the FOMC was aiming for a slow recovery in both prices and employment. I’ve argued too that the Committee’s desire for a slow recovery was consistent with its pre-2008 reaction function, which sought to constrain the variability of short-term interest rates. I now turn to the question of how the FOMC could change its “normal” policy reaction function so as to engender a better response to severe adverse shocks.

To be clear, there have been many prior suggestions about how to arrive at a better framework. Some observers have suggested that the FOMC should increase the inflation target, so as to have more policy space to deal with adverse demand shocks. Some observers have suggested that the FOMC should target the price level rather than the inflation rate. Still others have suggested that the FOMC should target the level of nominal income.

I see merit in all of these suggestions, and I welcome explorations of their consequences. But they represent large changes in the FOMC’s long-run goals. I will instead recommend a more minimal change in terms of the FOMC’s strategy—that is, how it seeks to pursue its current long-run goals. My recommendation is that the FOMC should adopt a policy framework that puts considerably more emphasis on returning the economy to its dual mandate objectives over the medium term. Such a framework would immediately imply that the FOMC should use a monetary policy reaction function that is a lot more responsive to the Committee’s best medium-term projections of inflation and output gaps.

What would be the benefits of this change in the FOMC’s strategic framework? I see two clear benefits. First, the FOMC’s choices would systematically return both inflation and output to desired levels more rapidly. There would be less persistence and less volatility in both inflation and output gaps. Second, the credibility of the FOMC’s inflation target would be enhanced. As noted earlier, in November 2009, the staff projected that, if the FOMC used the Taylor Rule after liftoff, inflation would remain at 1.6 percent or below for the next five years. This kind of outcome creates large downside risk to the credibility of the inflation target.

Those are the benefits: less variance in macroeconomic variables and enhanced credibility of the FOMC’s long-run inflation target. What would be the costs? The key cost is that, of course, the fed funds rate would be more variable around its long-run level. I have two comments about this putative cost. First, I don’t know of models in which such a cost is grounded in traditional welfare economics.10 The real interest rate is a key intertemporal price, and it may need to vary a lot to effect a desirable allocation of resources. According to models that are currently available, it would be welfare-reducing to smooth the fluctuations of this important price.

Second, and perhaps relatedly, my reading of the Federal Reserve Act is that Congress has not mandated that the FOMC seek to constrain the variability of its policy instruments. Congress has mandated that the Committee adjust its policy instruments as needed so as to achieve its macroeconomic objectives.11

To summarize my third and final point: The FOMC should strongly consider lowering its implicit penalty on interest rate variability relative to what was being imposed before the crisis. Doing so would lead the Committee to use a monetary policy reaction function that puts more weight on its forecasts of inflation and output gaps. Such a reaction function would automatically engender a more appropriate monetary policy response to severe downturns in inflation and employment such as those experienced during the Great Recession.

Conclusions

The theme of this speech is that the FOMC’s thinking about appropriate monetary policy in extraordinary times like late 2009 is heavily influenced by its policy framework during normal times. It should choose its new “normal” policy framework with this in mind. I have argued that the pre-2008 framework led the Committee to aim for a relatively slow recovery in inflation and employment in the wake of the Great Recession. I’ve recommended that, going forward, the Committee should use a reaction function that would be considerably more responsive to its best available forecasts of inflation and output gaps.

The U.S. House recently passed a measure, the Fed Oversight Reform and Modernization Act, that would enshrine the Taylor Rule as a key benchmark for monetary policy. Federal Reserve Chair Janet Yellen recently wrote in a letter12 to House leaders that the bill “would severely impair the Federal Reserve’s ability to carry out its congressional mandate to foster maximum employment and stable prices and would undermine ability to implement policies that are in the best interest of American businesses and consumers.”

My argument today gives a concrete example of Chair Yellen’s criticism. The FOMC did treat the Taylor Rule as a key benchmark for monetary policy during the early part of the recovery from the Great Recession. By doing so, we were systematically led to make choices that were designed to keep both employment and prices needlessly low for years.

Ultimately, if this legislation were to become law, it would force the Federal Reserve into the same kinds of choices in the wake of future adverse shocks.

Thank you.

Note

* I thank Terry Fitzgerald, Rob Grunewald, Jenni Schoppers, Samuel Schulhofer-Wohl and David Wargin for helpful comments.

Endnotes

1 See the definition here: federalreserve.gov/faqs/what-does-the-fomc-mean-by-monetary-policy-normalization.htm.

2 See Taylor (1993).

3 That is, the fed funds rate equals 2 + 2 + 0.5*(inflation – 2) + 0.5*output gap, which is 2.5.

4 See Taylor and Williams (2010).

5 More mathematically, we can derive the Taylor Rule as the first-order condition of a central bank optimization problem when the central bank is averse to interest rate gaps. Thus, suppose that the central bank has a quadratic loss function with weight on both inflation gaps and interest rate gaps. Suppose as well that the current inflation rate is (well-approximated by) an affine function of the current interest rate. Then the bank’s optimal interest rate choice would set the interest rate equal to an affine function of the inflation gap. It is readily shown that the slope in this relationship converges to infinity as the weight in the objective on interest rate gaps converges to zero.

6 The FOMC had not yet formally adopted a 2 percent long-run inflation target, and five participants specifically said that they saw a long-run inflation rate of less than 2 percent as being appropriate. The median unemployment projection for the fourth quarter of 2012 is unchanged if I exclude these participants, while the inflation projections are slightly lower.

7 As I noted earlier, I was a participant in the November 2009 meeting. According to FOMC security protocols, I am not allowed to inform the public of my submitted projections at that meeting for another five years. I am allowed to say that, as of November 2009, my economic outlook was that, under appropriate monetary policy, the unemployment rate would fall to 7.5 percent and that the PCE inflation rate would rise to 2.3 percent by the fourth quarter of 2012. I also had concerns about upside risk to longer-term inflation expectations because of what seemed at the time to be a large Fed balance sheet. Because of my concerns about inflation, my perspective at that time was that appropriate monetary policy would require a more rapid withdrawal of accommodation than preferred by most of my colleagues. My concerns about inflation proved to be misplaced.

8 I refer to participant number 14.

9 More specifically, the staff used a version of Taylor’s (1993) rule that incorporates a reformulation of the output gap into an unemployment gap using Okun’s Law.

10 Woodford (2003) assumes, without formal justification, that the central bank’s objective includes a penalty on interest rate variability. Under this assumption, he proves in the context of a New Keynesian model that it is optimal for the central bank to seek to minimize interest rate changes. Stein and Sundaram (2015) show that aversion to bond market volatility can also motivate the central bank to adjust interest rates slowly, but that these preferences on the part of the central bank actually lead to socially suboptimal policy; welfare would be higher if the central bank put less weight on preventing bond market volatility.

11 The Federal Reserve Act does have a third mandate that the FOMC should promote moderate long-term interest rates. I continue to believe that this mandate is best fulfilled by the Committee’s keeping long-run inflation expectations well-anchored.

12 See the letter here: federalreserve.gov/foia/files/ryan-pelosi-letter-20151116.pdf

References

Boehm, Christoph, and Christopher L. House. 2014. “Optimal Taylor Rules in New Keynesian Models.” Working Paper 20237. National Bureau of Economic Research.

Stein, Jeremy C., and Adi Sunderam. 2015. “Gradualism in Monetary Policy: A Time-Consistency Problem?” Working paper. Harvard University and National Bureau of Economic Research.

Taylor, John B. 1993. “Discretion Versus Policy Rules in Practice.” Carnegie-Rochester

Conference Series on Public Policy 39: 195-214.

Taylor, John B., and John C. Williams. 2010. “Simple and Robust Rules for Monetary Policy.” Chap. 15 in Benjamin M. Friedman and Michael Woodford (eds.), Handbook of Monetary Economics 3 (1): 829-59.

Woodford, Michael. 2003. “Optimal Interest-Rate Smoothing.” Revised excerpt from “Optimal Monetary Policy Inertia,” Review of Economic Studies70: 861-86.

Of all FOMC members in recent memory Kocherlakota impressed me the most: His early commentary and voting record were rather unequivocally fresh-water inspired, viewing QE and the expansion of the Fed balance sheet as likely ineffective while risking hyperinflation, but he was persuaded by the evidence that a broadly Hicksian framework was the best way to make sense of what was happening (demand slack w/ deflationary and dis-employment pressures) and increasingly supported Bernanke in efforts to improve liquidity and reduce unemployment.

In short he not only showed respect for evidence and logic — IIRC he eventually fired his chief economist, some U of Chicago big shot, for failing to do the same — he respected his oath of office and the dual mandate of the Fed.

“When my information changes, I alter my conclusions. What do you do, sir?” ― John Maynard Keynes