Yes, Q4-20015 real GDP growth likely slowed to a crawl. Yes, the stock market has taken it on the chin in recent weeks. Yes, credit-quality yield spreads have been trending higher since mid-year 2015. Yes, commodity prices have cratered. Is it time to panic about an impending U.S. economic recession? Investors would be wise to heed the advice given to anxious Green Bay Packers’ football fans after the Pack’s 1-2 start to the 2014 regular season by future NFL Hall of Fame quarterback, Aaron Rodgers, “R-E-L-A-X.” (Rodgers’ advice was prescient. The Pack went on to post a 12-4 regular season record, losing a heartbreaker in overtime to the Seattle Seahawks in the NFC championship playoff game.) After a shaky start in 2016, U.S. risk assets may not perform as well as the Packers did in 2014 after their shaky start. But, I believe that the U.S. economy and risk assets can still post a “winning season” in 2016. Just as the performance of Aaron Rodgers helped turnaround the Pack’s 2014 season, the likely performance of thin-air credit will help turnaround U.S. economy’s 2016 season.

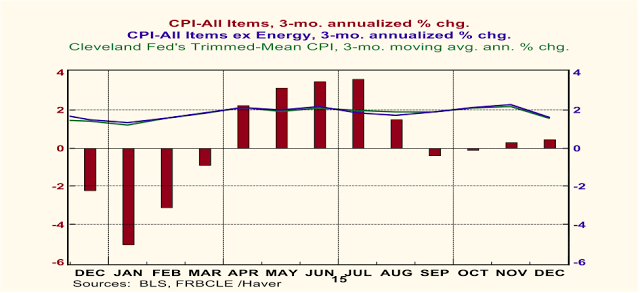

Back on December 1, 2015, I penned a piece entitled “The December 16th Fed Tightening – Preemptive to a Fault” in which I argued that the Fed’s imminent December 16 rate hike would come in the face of a significant slowing in the growth of U.S. economic activity, low and declining inflation, save for house prices, and low inflation expectations based on market indicators (rather than Fed economists’ forecasts). I stand by my December 1 commentary. On Friday, January 29, the Bureau of Economic Analysis is scheduled to release its advance (first of many) estimate of Q4:2015 real GDP annualized growth. The Federal Reserve Bank of Atlanta’s GDPNow estimate of it as of January 20 was 0.7%. The consensus estimate of it from economists participating in the Bloomberg survey is 0.9%. To refresh your memory, real GDP grew at an annualized pace of only 2.0% in Q3:2015. So, the pace of U.S. economic activity likely slowed further in Q4:2015 from an already tepid pace in the previous quarter. No matter how you slice it or dice it, neither is current goods/services price inflation above the Fed’s 2% target nor do market-based expectations suggest it is likely to rise above the Fed’s target anytime soon (see Charts 1 and 2).

Chart 1

Chart 2

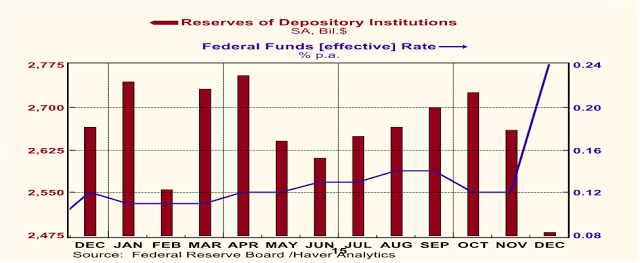

In my December 1, 2015 commentary, not only did I argue that the Fed’s imminent interest rate increase was ill advised, but that it would necessitate a reduction in Fed-created depository institution reserves, which would adversely affect the growth of total thin-air credit, i.e., the sum of credit created by depository institutions and the credit created by the Fed (depository institution reserves). Chart 3 shows that the monthly average of total depository institution reserves fell (by $179 billion) in December 2015 as the Fed implemented a 25 b.p. increase in its target federal funds rate mid month.

Chart 3

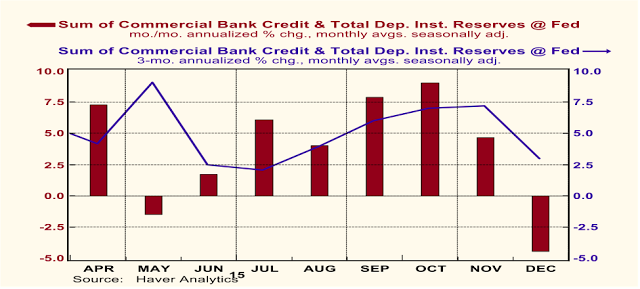

And sure enough, growth in total thin-air credit was adversely affected. As shown in Chart 4, total thin-air credit contracted at an annualized rate of about 4-1/2% in December 2015 compared to the previous month’s annualized growth of 4.7%. On a three-month annualized basis, total thin-air credit growth slowed to 3.0% in December 2015 vs. 7.2% in November 2015. The long-run median growth in total thin-air credit is around 7-1/4%.

Chart 4

With this contraction or slowing in the growth of total thin-air credit, depending on the time period considered, why am I confident that a U.S. recession is not imminent and that the pace of economic activity will pick up in 2016 from its Q4:2015 slowing? There are two reasons for my relatively optimistic outlook. First, although the Fed’s contribution to thin-air credit took a nosedive in December 2015, the commercial banking system’s contribution to thin-air credit has been robust in recent months and weeks. Second, after its December 16, 2015 interest rate increase faux pas, the Fed will be slow to increase its policy interest rates again in 2016. In turn, this implies that the Fed will not need to reduce again soon its contribution to thin-air credit, i.e., reserves.

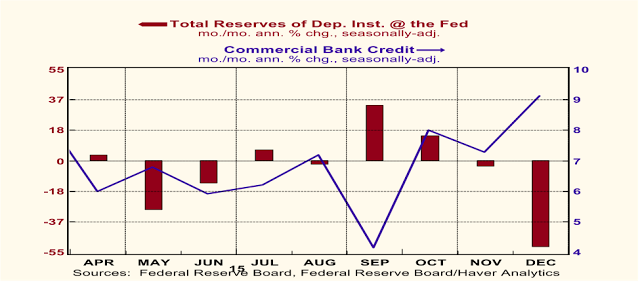

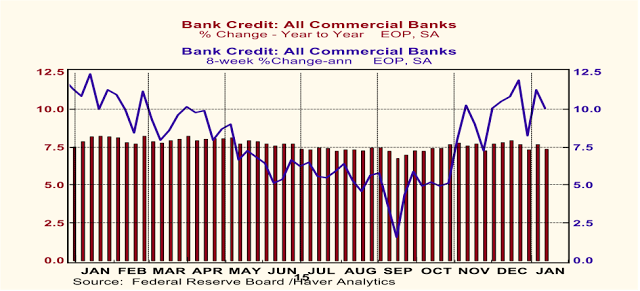

Chart 5 shows clearly why total thin-air credit contracted month-to-month in December 2015. It was because of the contraction in depository institution reserves at the Fed. Reserves contracted at an annualized rate of 51.4% in December 2015 vs. the month prior, while commercial bank credit grew at an annualized rate of 9.1%.

Chart 5

Weekly observations of commercial bank credit show that this component of thin-air credit continues to grow robustly on a year-over-year basis as well as an 8-week basis (see Chart 6). So, if the Fed’s contribution to thin-air credit, bank reserves, would stop contracting, total thin-air credit growth would likely re-accelerate.

Chart 6

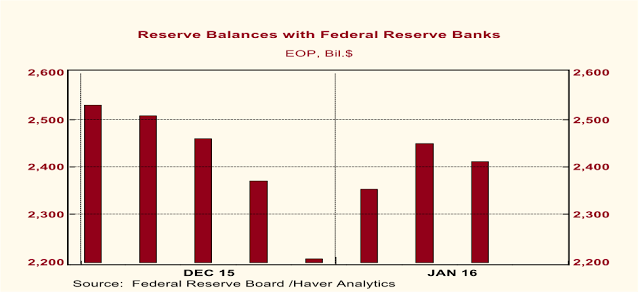

And that’s exactly what has happened. Chart 7 shows that on a weekly basis bank reserves fell throughout the month of December 2015 in order to effect the rise in the Fed’s federal funds rate target. But the level of bank reserves has moved higher in the first three weeks of January 2016. Keep in mind, the Fed would need to lower the supply of reserves relative to the demand for reserves if the federal funds rate is to be increased. But once that higher federal funds rate level has been achieved, the Fed does not have to continue reducing the supply of reserves to maintain the higher federal funds rate level, all else the same. So, if the Fed’s December 2015 interest rate hike will not be repeated for some time, the level of bank reserves would not be expected to decline further other than for temporary seasonal reasons.

Chart 7

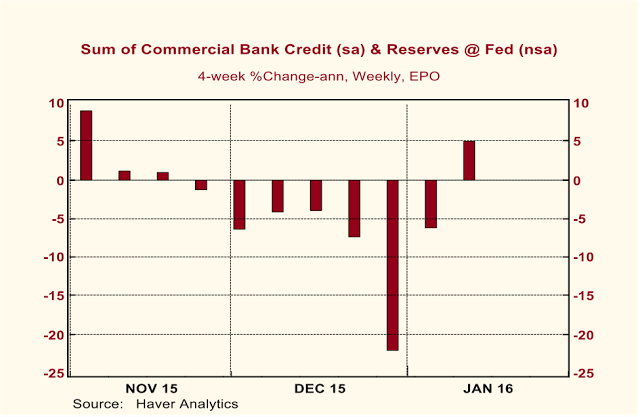

Again, if bank credit growth were to continue at its recent robust pace and bank reserves were to just stop contracting, which appears to be the case, then total thin-air credit would be expected to re-accelerate going forward. Although four weeks do not exactly a trend make and using weekly reserves data that are not seasonally adjusted is not best practice, growth in total thin-air credit has begun to re-accelerate in January 2016, as shown in Chart 8.

Chart 8

In sum, despite U.S. economic growth slowing to almost stall speed in Q4:2015, the U.S. economy is unlikely to crash anytime soon. Although the Fed is unlikely to reverse its ill-advised December 2015 interest rate increase, it also is unlikely to again raise interest rates and contract reserves until it is sure U.S. real economic growth is back on a sustained 2-1/2%+ trajectory and there are at least some faint signs of inflationary pressures. In my view, the earliest these conditions would be met and known is mid 2016. Bear in mind, the Fed has stated that its monetary policy is data dependent. If the economic data don’t spike, the FOMC won’t hike. So, my advice to U.S. investors is what was Aaron Rodgers’ advice to Packers’ fans early in the 2014 NFL regular season – R-E-L-A-X. The U.S. economy and the prices of U.S. risk assets are likely to turn up later in 2016 as thin-air credit growth re-accelerates.

On a sad note, Robert G. Dederick, retired chief economist of The Northern Trust Company, passed away on January 19, 2016. Bob invited me to join his economic research staff in August 1986 and was my boss until his retirement in November 1994. No one could glean the nuances of an economic report better than Bob. Although Bob and I had our theoretical differences, I am indebted to him for giving me the opportunity to join his staff and grow professionally. May you rest in peace, Bob. You have earned it.

Source: Paul L. Kasriel (The Econtrarian)