Is There a Liquidity Problem Post-Crisis?

Vice-Chairman Stanley Fischer

Federal Reserve Board of Governors, November 15, 2016

At “Do We Have a Liquidity Problem Post-Crisis?”, a conference sponsored by the Initiative on Business and Public Policy at the Brookings Institution, Washington, D.C.

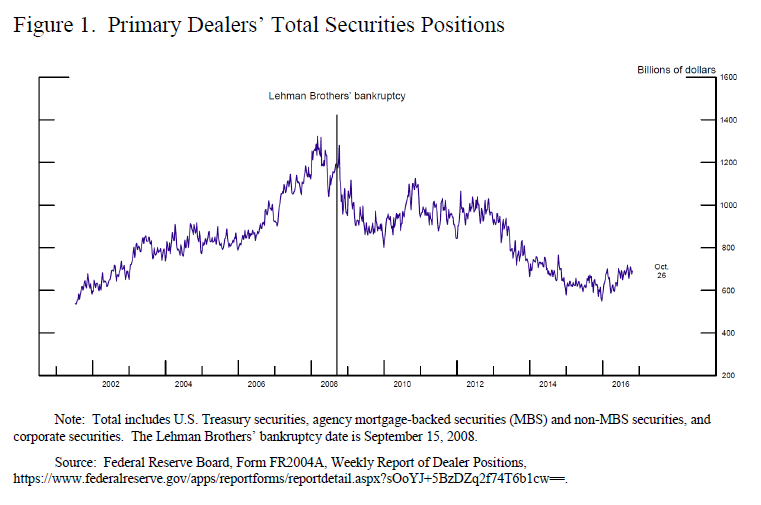

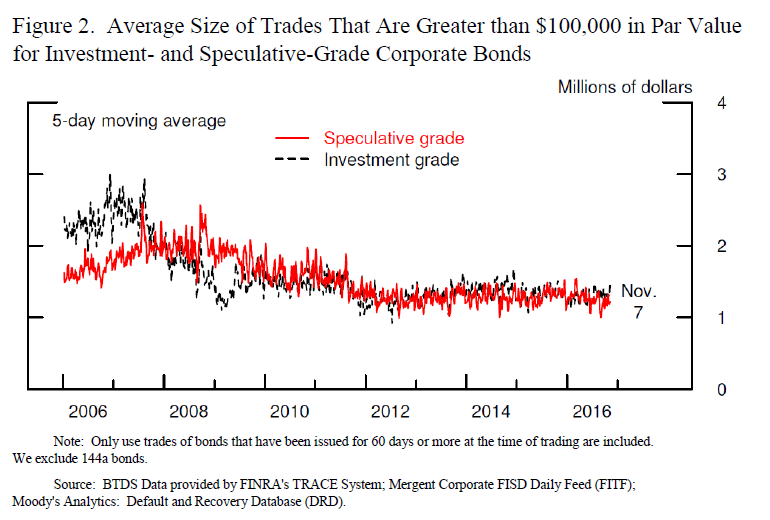

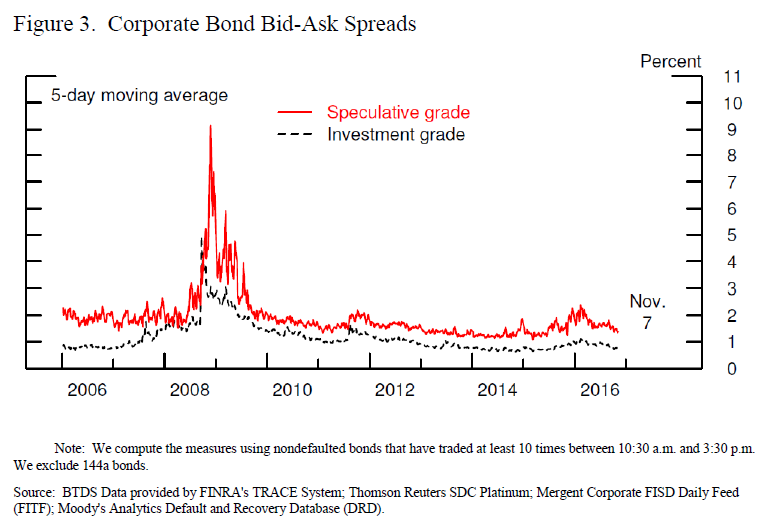

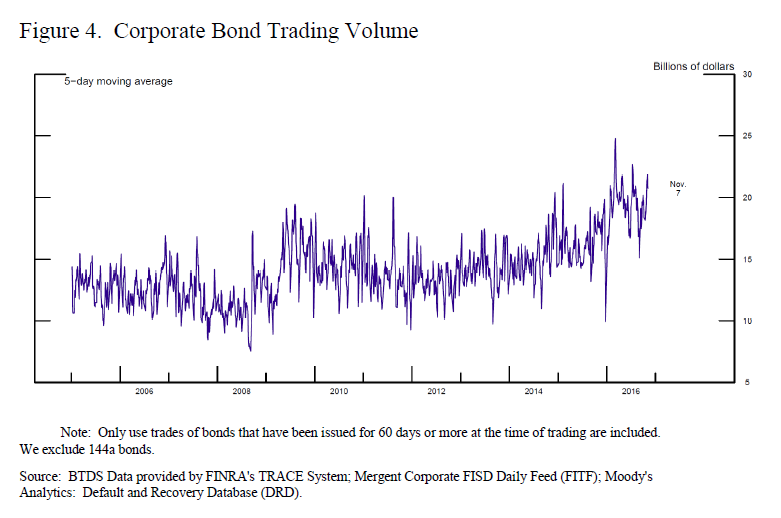

Market liquidity is the ability to rapidly execute sizable securities transactions at a low cost and with a limited price impact. The high degree of liquidity in U.S. capital markets historically has contributed to the efficient allocation of capital through lower costs and a mix of bank- and market-based finance that supports the flexibility of these markets. Regulatory changes may have altered financial institutions’ incentive to provide liquidity, raising concerns brought into sharp relief by several “flash events” over the past few years. At the same time, any changes in observed liquidity are also likely accompanied by other related changes–such as in technology–and a more complete assessment of these shifts is important when we think about the effects on liquidity of changes in financial regulations that were induced by the global financial crisis.

This afternoon, I will first review some of the concerns raised by market participants and others about market liquidity as well as highlight the challenges associated with finding clear evidence that substantiates these concerns. I will then discuss whether potential impairment of liquidity might exacerbate problems related to fire sales and leverage. Finally, I will make the case that any changes in market liquidity resulting from regulatory changes should be analyzed in the broader context of the overall safety of the financial system. This perspective naturally emphasizes potential tradeoffs between the possibly adverse effect regulations may have on market liquidity and their positive effect on the stability of the financial system.

Source: Federal Reserve