The Greatest Challenge Facing Mankind: Remarks to the Commonwealth Club by Michael Crichton San Francisco, September 15, 2003...

The Greatest Challenge Facing Mankind: Remarks to the Commonwealth Club by Michael Crichton San Francisco, September 15, 2003...

Read More

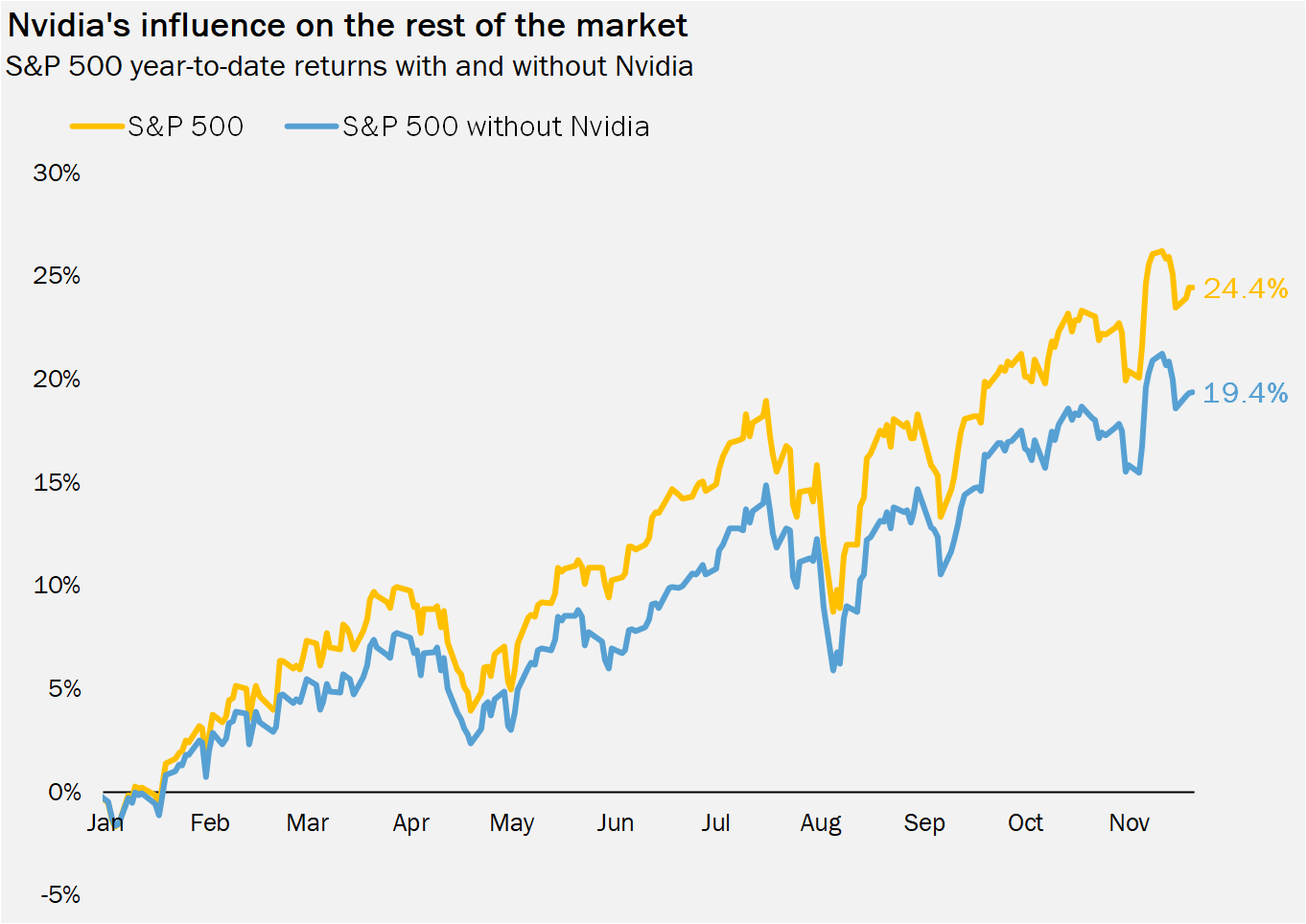

Callie Cox is the Chief Market Strategist at RWM. She regularly posts at Optimistic Callie. (Subscribe, its great...

Callie Cox is the Chief Market Strategist at RWM. She regularly posts at Optimistic Callie. (Subscribe, its great...

Read More

Jonathan V. Last is the editor of The Bulwark, and previously was senior writer and digital editor at The Weekly Standard...

Jonathan V. Last is the editor of The Bulwark, and previously was senior writer and digital editor at The Weekly Standard...

Read More

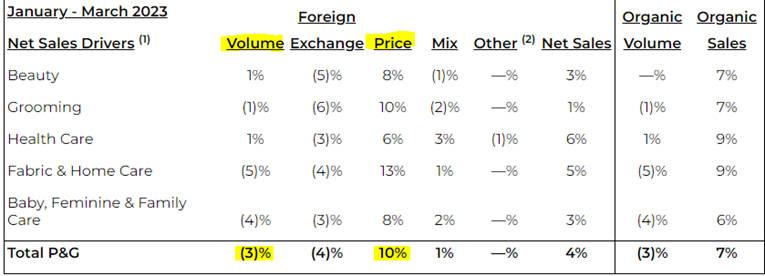

My fishing pal Sam Rines has spent much of this year pushing a thesis of “Price over Volume”; I found it a compelling...

My fishing pal Sam Rines has spent much of this year pushing a thesis of “Price over Volume”; I found it a compelling...

Read More

Elon’s Out Musk lost interest in pretending to buy Twitter. Bloomberg, July 9, 2022 I have occasionally spotlighted the...

Elon’s Out Musk lost interest in pretending to buy Twitter. Bloomberg, July 9, 2022 I have occasionally spotlighted the...

Read More

My guest this coming week on Masters in Business is William Bernstein, someone whose work I have long admired. Our...

My guest this coming week on Masters in Business is William Bernstein, someone whose work I have long admired. Our...

Read More

Philippa Dunne is one of the editors of The Liscio Report, an independent research newsletter focusing on the U.S. labor market,...

Philippa Dunne is one of the editors of The Liscio Report, an independent research newsletter focusing on the U.S. labor market,...

Read More

Art Cashin is Director of Floor Operations for UBS, where he also serves as a managing director of UBS Financial Services Inc. He...

Art Cashin is Director of Floor Operations for UBS, where he also serves as a managing director of UBS Financial Services Inc. He...

Read More

They’re All Friends in the Index Matt Levine Bloomberg, July 20, 2020 Matt Levine is a Bloomberg Opinion columnist covering...

They’re All Friends in the Index Matt Levine Bloomberg, July 20, 2020 Matt Levine is a Bloomberg Opinion columnist covering...

Read More

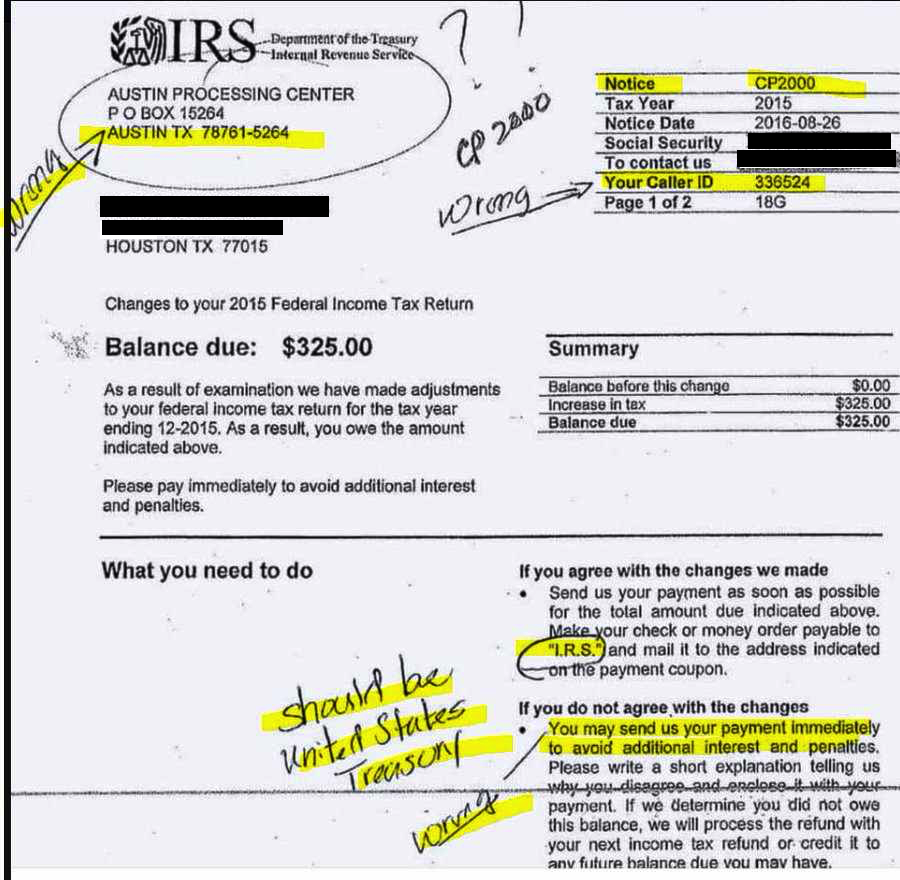

Before we get into the specifics of this fraud, some reminders: (1) The IRS will never call you to initiate an...

Before we get into the specifics of this fraud, some reminders: (1) The IRS will never call you to initiate an...

Read More