The Financial Crisis Killed Hedge-Fund Performance

The industry never came back from the “Great Reset,” the huge sell-off during the first quarter of 2009.

Bloomberg, September 17, 2018

I have long been interested in hedge funds and their managers. We have regularly looked at issues such as changing fee structures, higher-than-rational expected returns, general cost and performance issues, and why investors keep shoveling money to the funds.

My Bloomberg News colleagues Katherine Burton, Melissa Karsh and Sam Dodge published an article last week, “The Incredible Shrinking Hedge Fund,” that is chock-full of charts and details about the sliding assets under management at funds, and the free fall in new funds even as total industry assets have hit all-time highs.

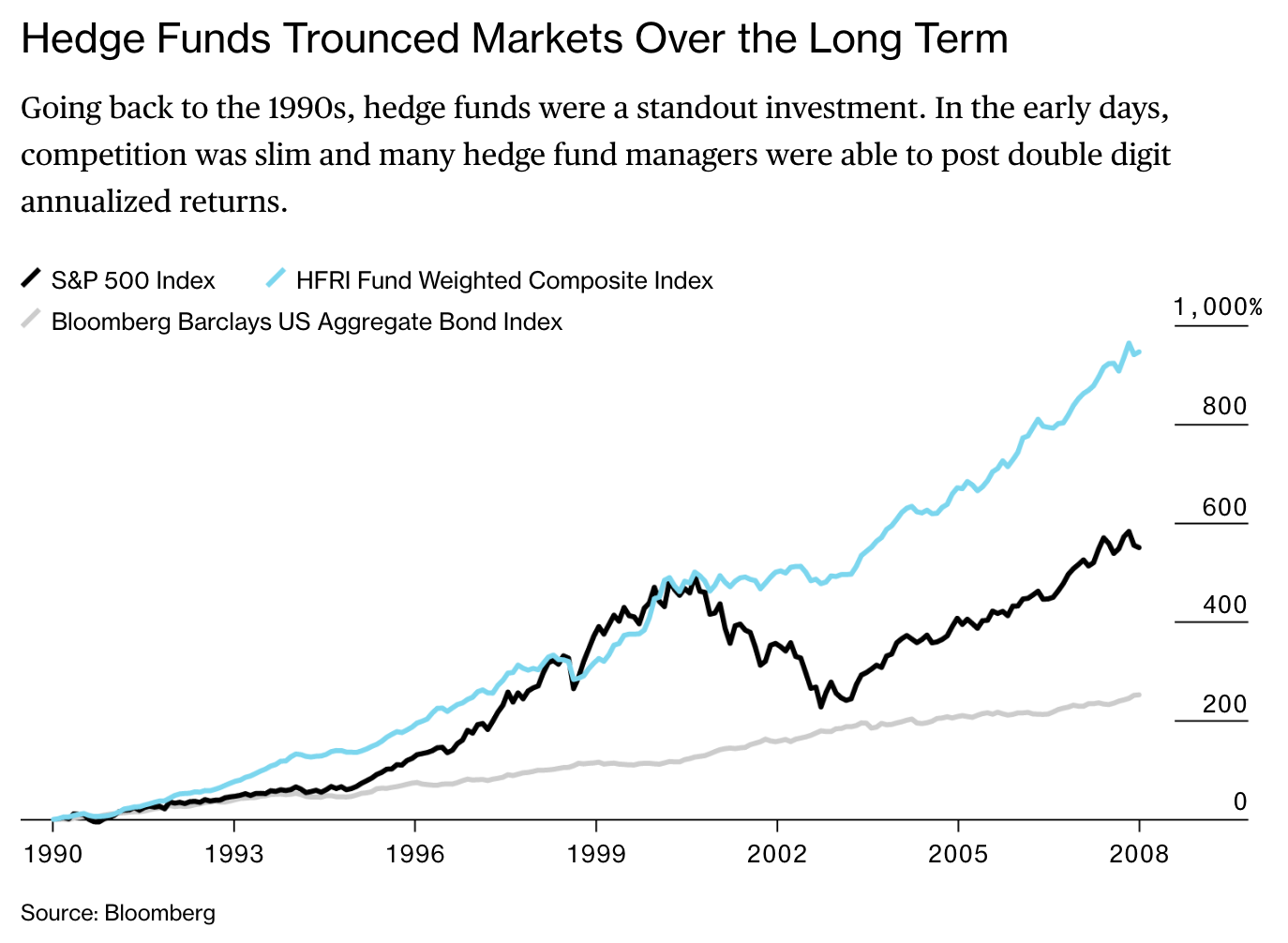

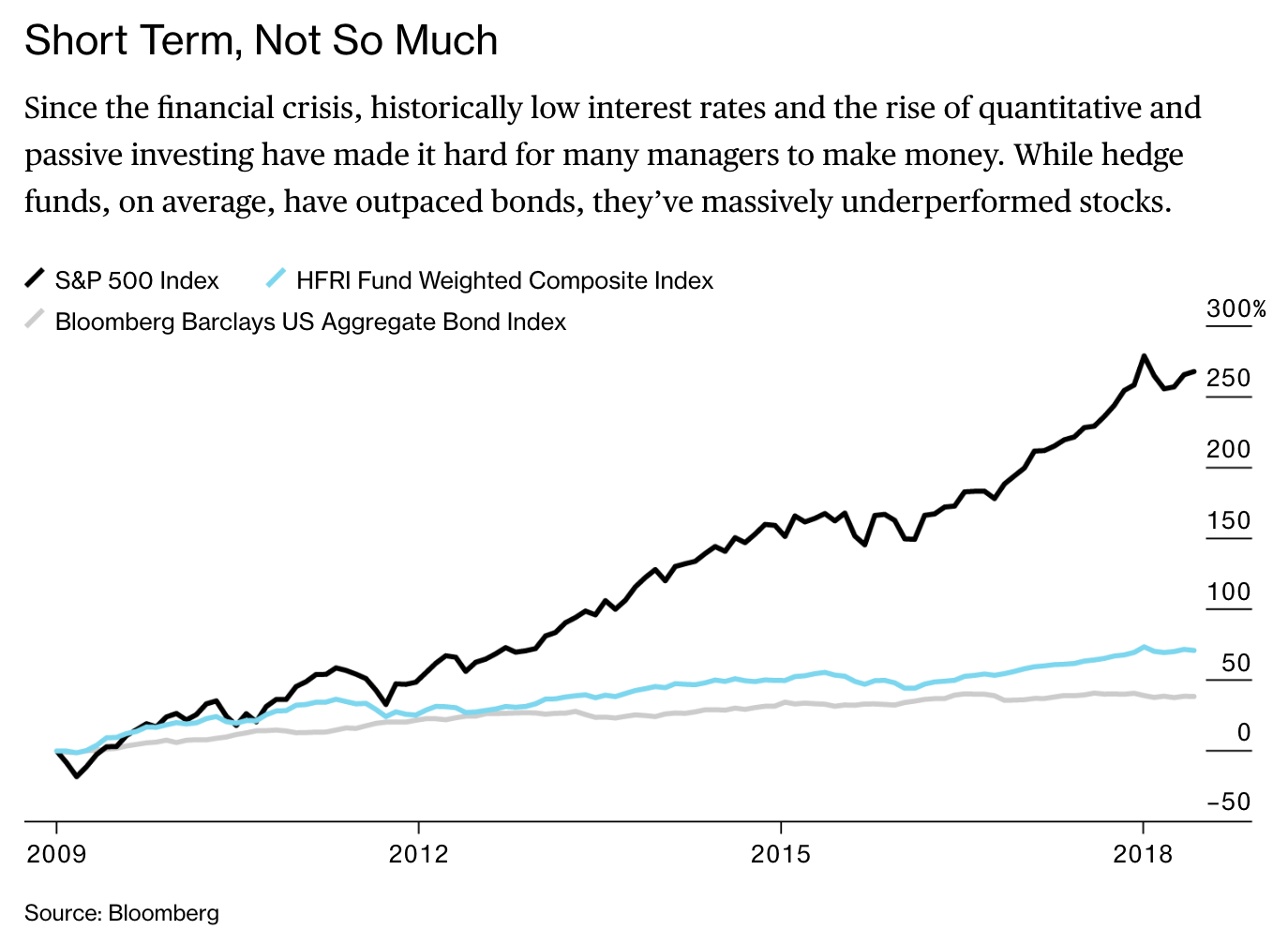

The article contains two fascinating charts showing hedge fund performance, pre- and post-crisis. The explanation given for the drop after the crisis is adequate, but still unsatisfying:

“Since the financial crisis, historically low interest rates and the rise of quantitative and passive investing have made it hard for many managers to make money.”

So why did the hedge fund industry’s long history of outperformance suddenly go away post-crisis? There have been five credible theories; my own, the Great Reset, follows.

1. Dilution: There are more than 11,000 hedge funds today, up from 5,000 in 2004 and fewer than 1,000 30 years ago. The proliferation might simply have caused too much dilution of a limited talent pool. As Howard Marks once said “The performance of the greatest hedge funds, run by geniuses, created a huge umbrella over this industry, which permitted the other 9,990 hedge fund managers to start hedge funds and command hedge fund fees.” He was even more blunt in a 2004 chairman’s memo, noting there were 5,000 hedge funds, and “I don’t think they’re run by 5,000 geniuses.”

1b. Fat head, long tail: A variation of this is the distribution of alpha among managers; it may still be with the handful of those few geniuses. Jim Chanos of Kynikos Associates has suggested that in the 1970s and 1980s, only 20 to 30 managers were creating alpha out of the hundreds of hedge funds; today, there might still be 20 to 30 reliable alpha generators, but out of 11,000. 1

2. Size is an issue: When it comes to performance, bigger may not be better. It’s long been established that small, emerging managers are where most of the alpha is found. But institutions prefer size and longevity rather than actual innovative alpha generation. Thus, size is great for institutional asset gathering, but gets in the way of returns. Scale can turn a rock-star fund into a professionally managed business, but does not necessarily translate into performance. Indeed, post-crisis, a few star funds that had capitalized on the downturn grew tremendously, then ran into the wall.

3. Size removes incentives: My colleague Josh Brown has a theory that the incentive system — also known as fees — changes as these funds have scaled up. “Two and 20,” as the 2 percent management fee and 20 percent of gains is known, creates different motivations for different-sized funds. For a fund with a few hundred million dollars, the upside comes from the performance fees (the 20 percent), but once these funds scale up to $20 billion, $30 billion or $40 billion, the 2 percent fee is a huge revenue generator. That’s $500 million a year for a $25 billion fund. Somewhat perversely, big assets under management make managers more conservative.

4. Groupthink: I have suggested (in jest) that the uber-bearish website ZeroHedge, which has missed the entire rally off of the 2009 lows to the present, explains hedge fund underperformance.2 But the truth behind that joke is that groupthink in the era of social media has even infected fund management.

5. Recency effect/bad timing: The famed investor Charlie Ellis pointed out that:

Data from over 35 years of behavioral research on individual managers at institutional funds show that large numbers of new accounts go to managers who have produced superior recent results – mostly after their best-performance years – and away from underperforming managers after their worst-performance years.

Mean reversion may have been a huge factor. As Donald Steinbrugge, of Agecroft Partners, explained, there have been nine years of increasing flows to funds, with most coming from redemptions to other funds.

Finally, my theory: the Great Reset. The combination of the financial crisis, the bailouts, zero-interest-rate policies and quantitative easing were all factors, for sure. But I suspect many have overlooked the cathartic impact of a once-in-a-generation, full-blown capitulation during the first quarter of 2009.

The effect of that huge sell-off was a full reset — a reboot and brand new game. All of the misallocated capital was wiped out, all of the investor leverage gone. And what changed completely was the cycle — whatever the prior gestalt was it was replaced by something new and entirely different.

People were very slow to recognize this.

Post-crisis, a new world emerged. What worked before just stopped working. That moment of capitulation was when all of the old playbooks should have been tossed aside for something new.

Every era is different. It might have been a lesson few learned. Hedge funds are no different.

1. The fat head, long tail thesis somewhat negates the pre-crisis claims of alpha generation. If the same 100 funds are the ones outperforming, then the huge rise in number of funds post-crisis is a valid statistical explanation of the post-crisis underperformance.

2. For that witticism, I was blocked by ZH on Twitter.

~~~

I originally published this at Bloomberg, September 17, 2018. All of my Bloomberg columns can be found here and here.

Source: Bloomberg