Total Return Major Global Assets from February 21, 2020 to February 23, 2021

Source: Deutsche Bank

Before this pullback began, the market had experienced an epic 12 months. It dates back to late February 2020, when the markets began to roll over as they sniffed out the potential downside of the looming pandemic.

After a 34% move down — the fastest 30% in market history — markets began to recover. This started way before any economic recovery was to be seen, long before vaccines were viable, and a good deal sooner than anyone’s sense of optimism about the future was in vogue.

Personally, I get annoyed when people declare the end of a bull market prematurely. So I will be giving this market the benefit of the doubt. To me, this feels more like profit taking than the end of the bull run (not that we manage money based on my gut feel, but you know what I mean). I could very well be wrong, but it simply seems to premature: There are still no signs of actual inflation (mostly inflation expectations), earnings remain decent, and spending is trending higher.

If you want to blame something for the sell off, you have lots of targets: The Inflationistas (To hell with Larry Summers!), the Faux Defict Chicken Hawks, reducing the size of the Covid relief plan; the bond market for its belated temper tantrum sending rates higher, or just the plain old unknown of WTF will happen next.

For the record, I date this bull market’s start to March 2013, and (as I observed last April) do not believe the March 2020 pullback ended the bull; it was more akin to an externality, a Pearl Harbor of sorts, then the usual was secular bull markets meet their ends.

If you have been long over the past year, if you did not get scared out of the markets last March, if you are trying to figure out what comes next, ask yourself this: Would 6 months of sideways action really be so terrible?

~~~

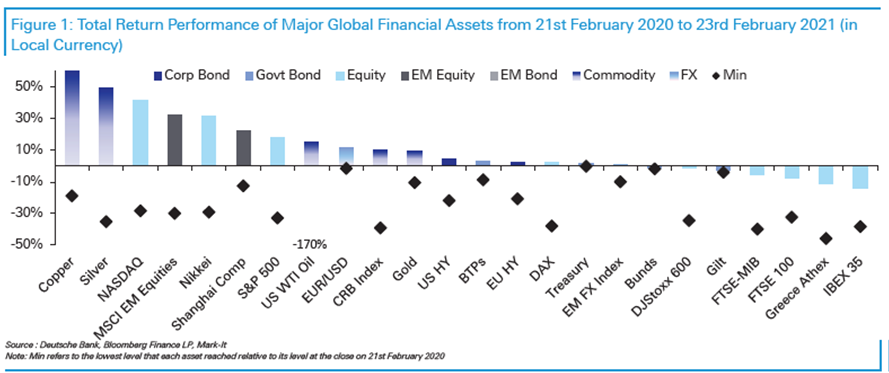

The chart above is from Jim Reid of Deutsche Bank; Here is his take from last week:

Today is the one year anniversary of the first big Covid sell-off as the virus started to hit Western nations. Monday February 24th 2020 saw a major global correction as Italian case numbers had rocketed over the weekend from single figures to 220! In today’s CoTD we show the performance of selected global assets since this date (local currency) and also include the low point seen over the last 12 months.

Assets we didn’t include in this high level list that have seen even larger moves include Bitcoin (+395.8% over the 12 months) and the NYSE FANG+ Index (+85.8%).

Had you been told 12 months ago that we would now have around 113 million recorded cases and 2.5 million recorded deaths (both likely understated) with much of the world under lockdown conditions for most of the year, I suspect you would have found it tough to comprehend the course of markets. However, the Fed and the ECB alone have added around $6 trillion to their balance sheet over this past year alongside trillions of fiscal injections. On this topic our US economists yesterday upgraded their US 2021 GDP forecast to +7.5% (Q4/Q4) on the expectation of a $1.6-1.7tn stimulus package soon. See

Another major story brewing after a truly remarkable 12 months.

Indeed.

Previously:

End of the Secular Bull? Not So Fast (April 3, 2020)

How Externalities Affect Systems (August 14, 2020)

Maybe Mr. Market Is Rational After All… (August 7, 2020)

FAANMG Stock Prices Reflect Global, Not US Recovery (July 17, 2020)

Happy Anniversary, Bear Market Lows! (March 18, 2019)

Invest in stocks? FORGET ABOUT IT (May 8, 2012)