A proposal from the current administration is working its way through the U.S. Securities and Exchange Commission to end quarterly corporate earnings.

This is a good idea.

Unfortunately, the frequency is in the wrong direction. Instead of replacing quarterly earnings releases with annual or semiannual ones, the SEC should be moving toward monthly, weekly, or even real-time earnings releases.

It’s counterintuitive until you experience it: more frequent reporting makes the data less significant.

Shifting from quarterly to annual doesn’t reduce the focus on short-term earnings management – it intensifies it. Think Christmas: If earnings come out only once a year, it becomes a huge event filled with hoopla and volatility. Even twice a year becomes a hyper-focused earnings-management festival.

The last time I addressed this was in 2018, during President Trump’s first term. As I exhorted the SEC:

“Report earnings monthly, with the goal of eventually moving to a near real-time, daily, fundamental update. Technology is improving to the point where business intelligence software and big data analyses will make this automated. Indeed, some companies already do much of this internally.” (emphasis added)

My frame of reference was the asset management shop I worked at in the late 2000s and early 2010s. I saw firsthand what the pressure of quarterly reporting does to a company that only issues its performance report four times a year. Regardless of whether we led or lagged the benchmark S&P 500 Index, the phones and emails would light up with questions.

That focus on the numbers every three months was an unhealthy obsession among clients and employees alike.

When we launched our firm in 2013, we worked with several partners (Custodians, Analytics, Reporting, etc.) to give every client real-time access to see exactly how they were doing, whenever they wanted. The only caveat we gave them: “You now have 24/7 access to see your returns, tick-by-tick — but please don’t, it will make you crazy.”

For the most part, this completely defused the hoopla around performance reporting.

The state of Artificial Intelligence today can do the same thing for the heightened focus on quarterly earnings reports for Corporate America. Back in the 2010s, Artificial Intelligence was in its “IBM Watson playing Jeopardy” era. We were pre-Claude, pre-Gemini, pre-ChatGPT, pre-Grok, and pre-Perplexity. Today, AI is something everyone carries around in their pockets.

This is not unknown territory. In 2014, the United Kingdom dropped its reporting requirements from quarterly to semi-annual; it saw no benefit. There was no increase in long-term investments after mandatory quarterly reports were dropped.1

Less frequent disclosure only widens the information asymmetry between insiders and investors; we will see even more insider trading as non-public information becomes more valuable. Price discovery will deteriorate even further than it already has. Instead of unpredictability, markets will experience regular tsunamis of volatility.

If we really want to end this sort of short-termism, companies should unilaterally stop giving guidance. The entire gamesmanship of beating last quarter’s company earnings guidance would come screeching to a halt.

The owners of corporate America, aka public shareholders, have the right to know how well the companies they own are doing. This includes basic information such as sales, revenue, and profits. The goal shouldn’t be to make public companies look like private ones. If anything, we should aim to generate more information about private and public companies so that investors can make informed decisions about risk.

This can be implemented gradually: the first companies that volunteer to move to monthly, then weekly, and then real-time are given safe harbor protection from the SEC (for a short period) against shareholder litigation. Eventually, over a 5-ish-year period, all companies move earnings reports to real time.

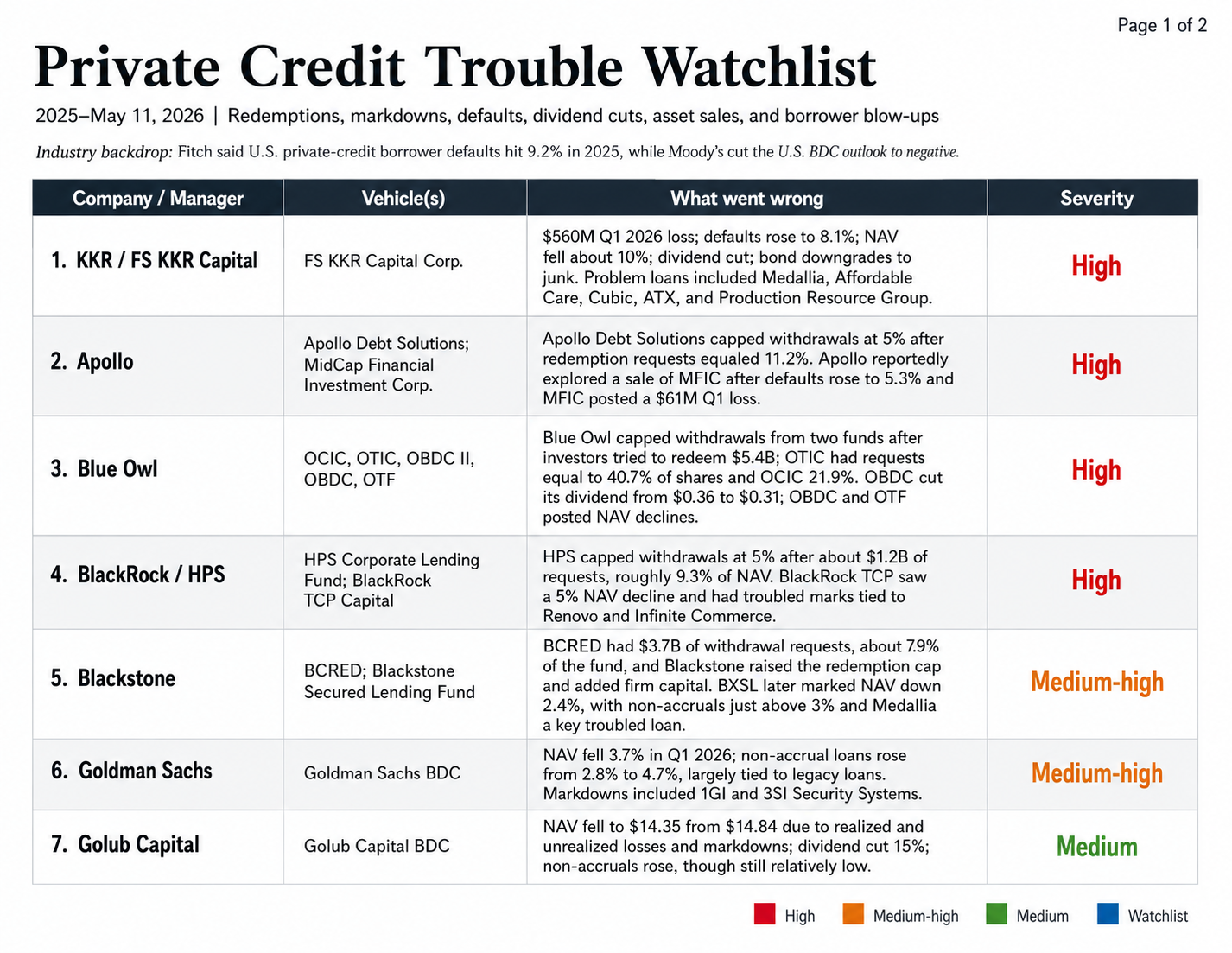

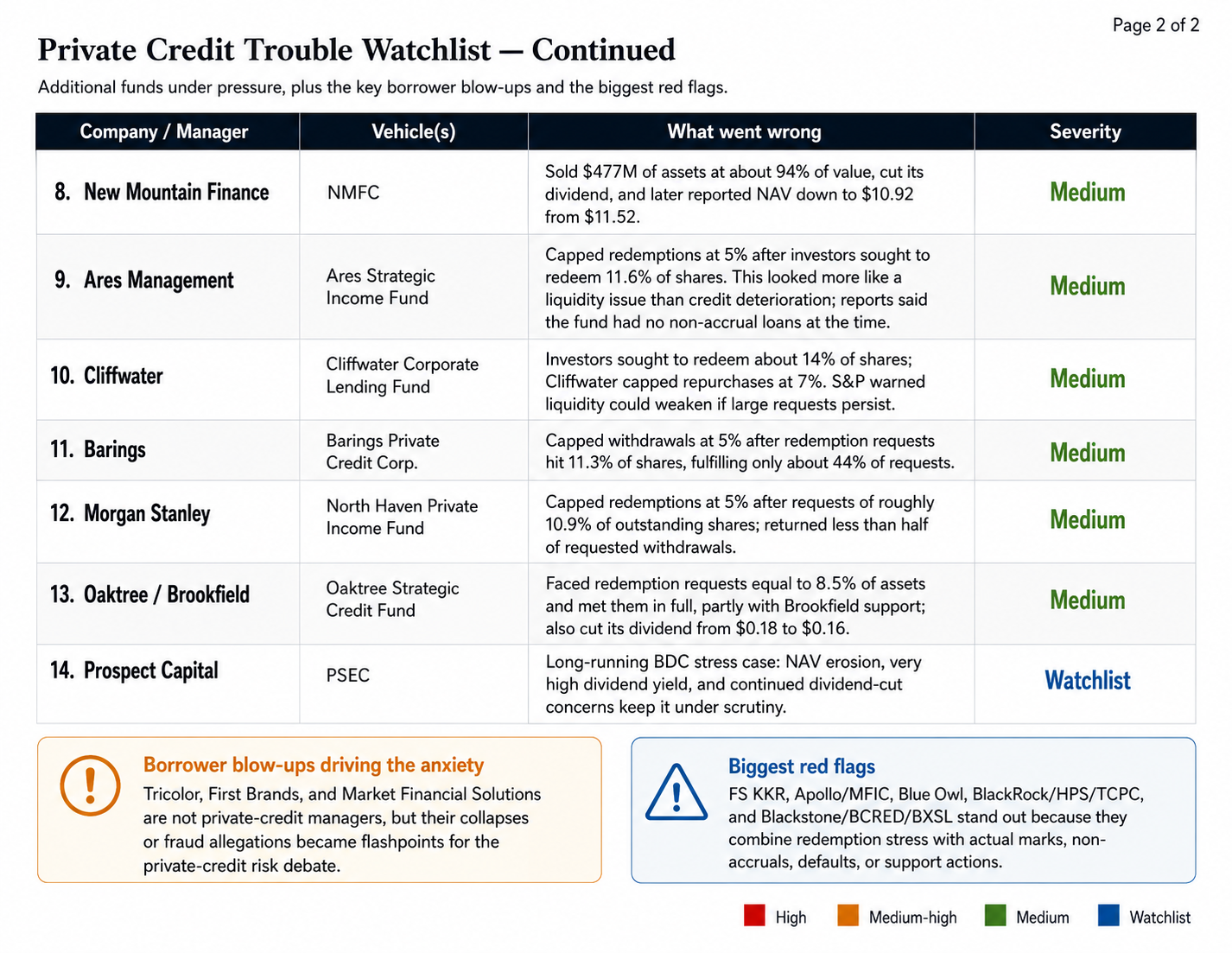

The recent blowups in private credit illustrate what happens when reporting is less frequent, transparency is lacking, and information exchange between those managing these firms and their owners or investors is highly limited. Private-credit managers, BDCs, interval/tender funds, and flagship private-credit vehicles have experienced notable redemptions, markdowns, defaults, and even portfolio blow-ups over the last couple of years. It is not a coincidence that these private companies report to their shareholders annually.

The idea of automating the process of reporting earnings in real time seemed fantastical a decade ago. Today, it is no longer unimaginable – it has become obvious.

Previously:

Report Earnings Daily (Bloomberg, August 20, 2018)

__________

1. Impact of Reporting Frequency on UK Public Companies by Robert Pozen, Suresh Nallareddy, and Shivaram Rajgopal

We studied the effects of these regulatory changes on UK public companies and found that the frequency of financial reports had no material impact on levels of corporate investment. However, mandatory quarterly reporting was associated with an increase in analyst coverage and an improvement in the accuracy of analyst earnings forecasts.”

~~~~~

AI DISCLOSURE: I wrote this myself. I used CHatGBT to generate the graphics; Claude to research various proposals, and Google Gemini to identify issues with UK changes in earnings reporting