Funny story: I was supposed to have Bobby Bonilla on for Masters in Business, but it did not come to pass.1

That was a shame, because it’s a fascinating cautionary tale about hubris, fraud, misunderstanding risk, and all sorts of other amusing and fun BeFi issues.

I went deep down the Bobby Bonilla Day rabbit hole, and it led me to some really astonishing findings. The basic story is this:

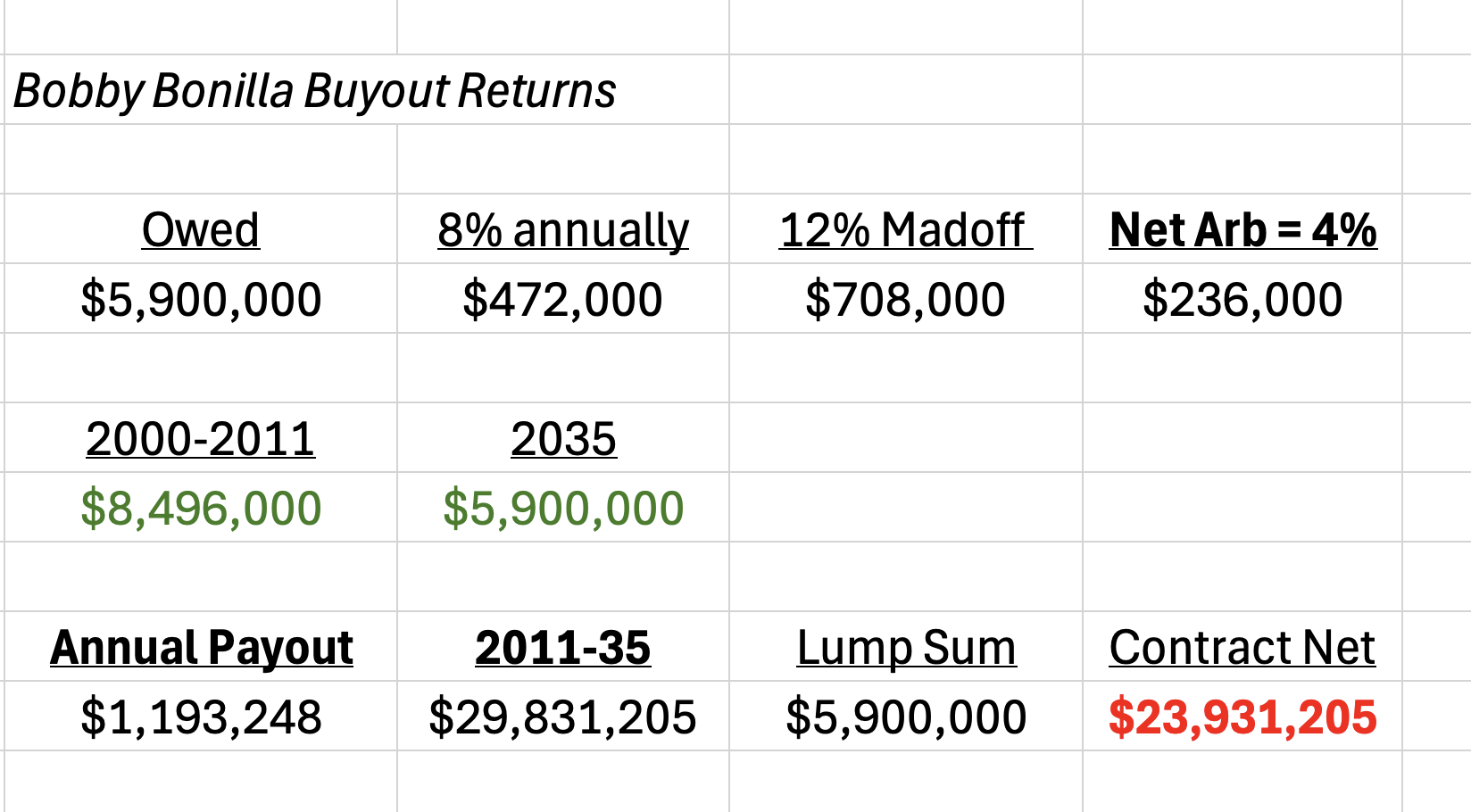

In 1999, the NY Mets decided to cut Bonilla loose after the season ended. Rather than pay him the $5.9 million contract balance in a lump sum, they offered a deferred deal of $1,193,248.20 for 25 years beginning July 1, 2011. That is an 8% interest rate, resulting in a total deal value of $29,831,205 over 36 years.

Why would the Mets do this?

Through a combination of misunderstanding risk, overconcentration in a single investment strategy, and not recognizing when an investment scenario was too good to be true. Getting scammed by the biggest Ponzi scheme in modern history didn’t help either.

These errors led the Mets’ ownership to craft the dumbest deferred deal in MLB history.

Sterling Equities was run by Fred Wilpon (Chairman) and Saul Katz (President). They acquired a partial interest in the New York Mets in 1980 and became full owners in 2002. Both men had a close relationship with Bernie Madoff, and they (along with friends and families) were associated with 483 Madoff accounts. Generating 12% per year, guaranteed. (!?)

Instead of simply paying $5.9 million dollars in lump sum, the strategy was to generate a positive return on Bonilla’s buyout of $8,496,000 by 2011, and an additional net arbitrage of $5,900,000 over what was paid to Bonilla by 2035.

Of course, all of this presumed that Madoff was not a felon scamming billions from his clients, including Wilpon and the Mets.

I reverse-engineered the deal the best I could, and I believe the math looks something like this:

For the dozen years covering 2000-2011, the $5.9 million the Mets owed Bonilla would generate about $708,000 per year at 12%. By the time the team would have to start paying the deferred contract in 2011, they would have accumulated $8,496,000 in annual returns; this is 12% only, and does not assume any additional compounding!

From 2011 on, the Mets would pocket the difference between the 8% contract payout and the 12% Madoff returns. That difference is $236,000 annually, or $5,900,000 over the 25-year deal. It is not a coincidence that this is EXACTLY the buyout amount owed to Bonilla.

Oh, to be a fly on the wall listening to that pitch:

“Not only do we earn $8.5 million before paying a single penny to BB, but the net arb over the life of the deal covers his full $5.9M! It’s free money!”

Only, not so much. The cost of NOT paying the $5.0m payout was $23,931,205.

The lessons here are obvious:

-Simplicity beats complexity

-Money has a time value

-If it looks too good to be true, it probably is.

Also, don’t do business with conmen…

__________

1. There was some confusion with Neuberger, which has Bonilla as a spokesperson of sorts for their annuities; there was some confusion (a ridiculous demand by them, actually) about a co-branding sponsorship that violated all sorts of Bloomberg rules, so they unfortunately pulled out of the recording.