I’m deep in my book writing work discussing federal debt when I see a tweet that simply epitomizes the entire genre....

I’m deep in my book writing work discussing federal debt when I see a tweet that simply epitomizes the entire genre....

Read More

@TBPInvictus here If you’re tired of California-minimum-wage-and-its-impact-on-limited-service-restaurant-employment stories, I...

@TBPInvictus here If you’re tired of California-minimum-wage-and-its-impact-on-limited-service-restaurant-employment stories, I...

Read More

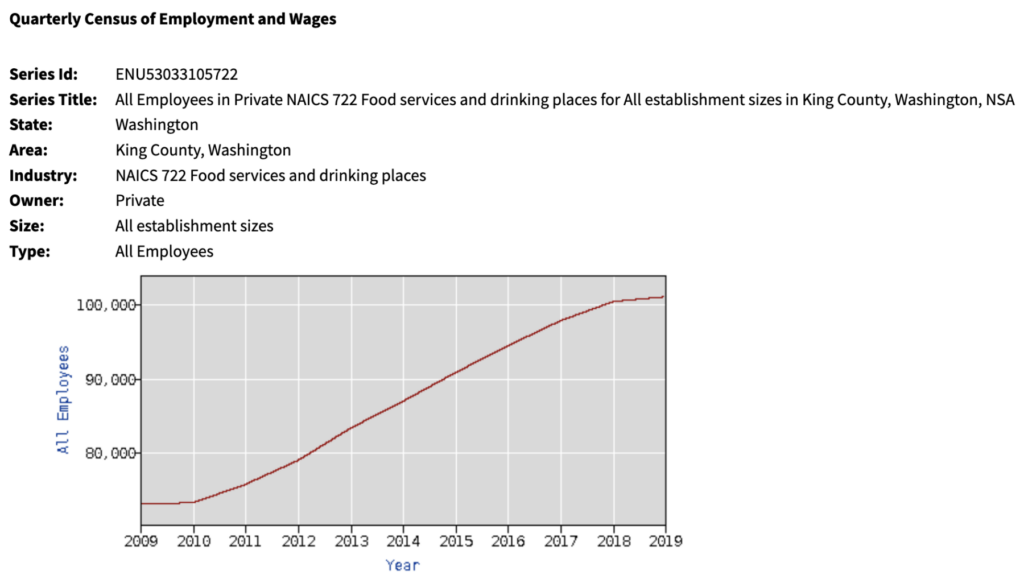

@TBPInvictus here. About a decade ago, the city of Seattle undertook to raise its minimum wage, over time, to $15/hour. Massive credit...

@TBPInvictus here. About a decade ago, the city of Seattle undertook to raise its minimum wage, over time, to $15/hour. Massive credit...

Read More

I just finished wrapping up the chapters in the new book1 on the dangers of denominator bias, along with related chapters on lack...

I just finished wrapping up the chapters in the new book1 on the dangers of denominator bias, along with related chapters on lack...

Read More

I haven’t been paying much attention to the 2023 election cycle, other than getting annoyed at all the silly polls for next...

I haven’t been paying much attention to the 2023 election cycle, other than getting annoyed at all the silly polls for next...

Read More

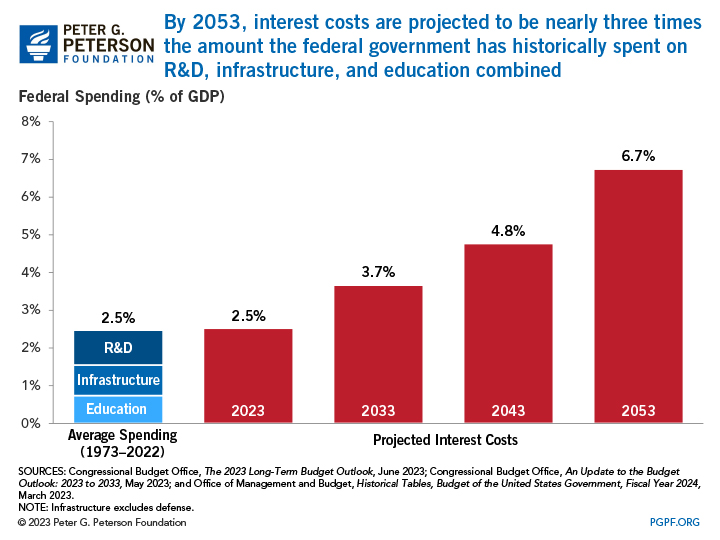

The chart in this morning’s reads shows what it is going to cost to fund the interest payments on the federal debt....

The chart in this morning’s reads shows what it is going to cost to fund the interest payments on the federal debt....

Read More

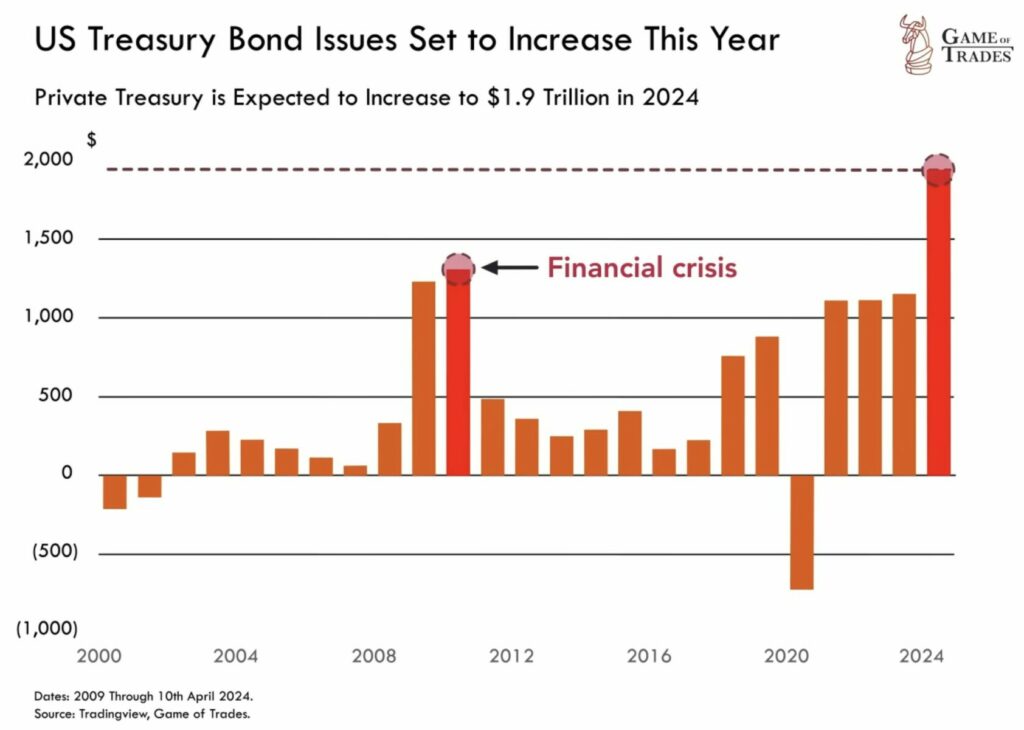

@TBPInvictus here; Let’s cut to the chase: “America’s Enormous Math Mistake” is a popular video on YouTube...

@TBPInvictus here; Let’s cut to the chase: “America’s Enormous Math Mistake” is a popular video on YouTube...

Read More

“Magazine covers, especially the Economist, are wonderful contrary indicators.” –@Trendsandtailrisks...

“Magazine covers, especially the Economist, are wonderful contrary indicators.” –@Trendsandtailrisks...

Read More

@TBPInvictus here: I want to avoid the usual “false equivalencies” and “both sides do it” approach, and ask a...

@TBPInvictus here: I want to avoid the usual “false equivalencies” and “both sides do it” approach, and ask a...

Read More

The Bull Stock Market Needs to Give Credit to the Calendar Returns this year look stellar, but only because equities collapsed the last...

Read More