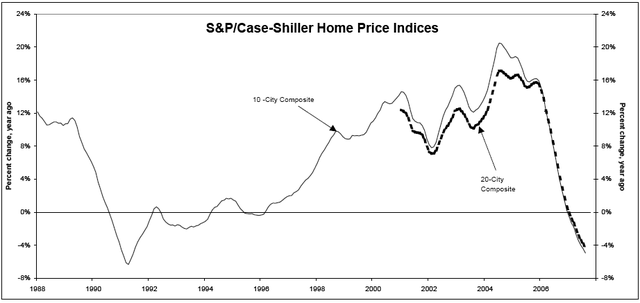

No surprise here: The Case-Shiller Home Price Index fell yet again.

Through August 2007, prices of existing single family homes across the United States. The index of 10 U.S. cities fell 5% in August from a year ago — the biggest drop since June 1991 (a decline of 6.3%

in April 1991 holds the record). It is the 21st consecutive month of decelerating returns.

Here’s Shiller on the details:

“At both the national and metro area levels, the fall in home prices is showing no real signs of a slowdown or turnaround,” says Robert J. Shiller, Chief Economist at MacroMarkets LLC. “Year-over-year and monthly price returns are continuing to either move deeper into negative territory or are experiencing persistent diminishing returns. There is really no positive news in today’s report, as most of the metro areas are showing declining or vanishing returns on both an annual and monthly basis. Only two metro areas – Denver and Detroit – showed improvement in their annual returns and even those were reports of slightly less negative numbers.”

Doesn’t look quite like a bottom just yet.

Treasury Secretary Hank “Strong Dollar” Paulson has finally come around. After making several prior, premature calls for a Housing bottom, I give credit to Paulson, who has now clearly changed his tune:

“The figures reinforce the view among Federal Reserve

officials and Treasury Secretary Henry Paulson that the housing

slump has further to go. Near-record inventory levels suggest

sellers will continue to lower prices, posing a threat to

consumer spending because homeowners will have less equity to

borrow against.

“This is really the No. 1 risk: a sustained, sharp

decrease in home prices really squeezing consumers,” said

Meny Grauman, an economist at Scotia Capital Inc. in Toronto.”

As Keynes stated, “When the facts change, I change my mind. What do you do, sir?”

Indeed . . .

>

Sources:

Further Weakening in Home Prices

S&P/Case-Shiller Home Price Indices

October 30, 2007

http://www2.standardandpoors.com/spf/pdf/index/CSHomePrice_Release_102626.pdf

S&P/Case-Shiller Home Prices Fell 4.4% in August

Courtney Schlisserman

Bloomberg, Oct. 30

http://www.bloomberg.com/apps/news?pid=20601087&sid=aRbwsKS_s_ZQ&

“Strong Dollar” Henry and “Helicopter” Ben are screwed, but they only have themselves to blame. How much lower can they cut rates, in all seriousness? Even if they did, what effect would that have? Inflation would just increase at a faster clip. They have really put themselves in a pickle. Didn’t Barry post about John Fogerty this past weekend? ;-)

“Strong Dollar” Paulson has changed the mantra because now they can use this to justify endless rate cuts. Oh! not endless. they have to stop at zero and start B-52 Ben’s aerial bombardment against the non-believers who won’t shop because they can’t meet house payments.

We’re in uncharted waters, the ship is listing, and we can’t navigate without charts (even if we had charts, our rudder is out of the water and we can’t steer the ship). ‘How deep is the bottom?’, is not the question. The question is, ‘how well can you swim?’

Keep your eye on the captian and officers – they’re going to try to steal the lifeboat and provisions.

Paulson either is stupid or knew damn well housing had not bottomed when he repeatedly said it had. For him, it is not a case of “When facts change, I change my mind”. It is a case of “When my prior politically motivated attempt to gull people into thinking things were going well becomes completely untenable, I try to salvage my credibility by acknowledging reality.” One hopes that his prior shilling for the administration did not actually convince anyone to buy or mortgage a home that is now worth less.

Giving credit to Paulson? Good Lord. The man is a politician. His words have been despicable since day one. Blowing smoke about a housing bottom when he knew better. Only now, when it is finally obvious to all, does he “change his tune.” He is either the dullest Treasury Secretary ever, or he is incredibly insincere. I believe it is the latter. The man deserves zero credit.

The only credit Paulsen deserves is being completely dishonest and talking from his lower regions at every available opp.

We are going to have a monumental problem of epic proportions if this “official” is allowed to continue to prop up the market for the sake of his handlers (chinese) and the GOP.

Without question the single biggest problem our financial system has today starts and ends with Hank Paulsen…let’s not forget Bernancke although he will have his own private place in hell starting about January 2009 when his current “strategists” suddenly look up and realize that 01/20/09 is approaching fast. By then they will have looted, plundered and lowered rates all under the guise of “forstalling” the recession so that they will be able to blame it on whoever wins the election.

I love how the media portrays MER as the only broker to loose money during the third Q……Last time I checked a write down=a loss…but not if you are a “journalist”.

Yet another bottom….gotta love it…

Ciao

MS

Excuse me? The facts didn’t change, they were ignored until it was evident that Hank/Ben were so wrong on the matter that the facts could be ignored no longer!

I am reminded of the scene in “Titanic” after they hit the iceberg. The crew is kicking around the ice on the deck and they are talking about getting in to New York late.

We live in interesting times!!!! We don’t know if we should get out our sunglasses because the future is so bright or run for the bunker. I guess I’ll just stand close to the bunker with my sunglasses on—lol

More of the deregulate, get the government off by back, free marketeer crowd suddenly want government help:

(Begin to spill into prime ???)

.

Anyone check the spreads on the CMBX indices lately? Over half are setting new highs, easily surpassing levels set in August. Same goes for the ABX indices setting new lows, yet CNBS talk is that we’re nearing the end of the credit crunch. Disdain for mass financial media grows by the hour.

http://www.markit.com/information/products/cmbx.html

Speaking of CFC… Government risk?

“U.S. Tosses Lifeline to Lenders Using Home Loan Banks

Oct. 30 (Bloomberg) — Banks shut out of the market for short-term loans are finding salvation in a government lending program set up to revive housing during the Great Depression.

Countrywide Financial Corp., Washington Mutual Inc., Hudson City Bancorp Inc. and hundreds of other lenders borrowed a record $163 billion from the 12 Federal Home Loan Banks in August and September as interest rates on asset-backed commercial paper rose as high as 5.6 percent. The government-sponsored companies were able to make loans at about 4.9 percent, saving the private banks about $1 billion in annual interest…”

http://www.bloomberg.com/apps/news?pid=20601087&sid=a_l2_kTFSFGU&refer=home

yes the timing of all of “tangelo’s” comments are usually applicable to 1). Him making yet another change in his stock sale plan. 2). The Fed just happens to be meeting as they were when he opened up his mouth about it last time.

How this guy is not in jail is beyond reproach…he just continues to go along and be a “victim” of his own failure to understand the business that has made him very rich.

But I guess it’s just a coincidence that he has sold hand over fist for over a year.

Ciao

MS

I was home sick yesterday and had Bloomberg on in the background. One of their guests was demanding 11 consecutive 25 bps cuts. I’m like, did you guys forget what got us in this mess in the first place? Suck it up.

And is anyone else but me getting a chuckle out of the fact that Mozillo and Mezger were speaking at the Milken Institute yesterday (from the article VJ linked)?

that little tidbit did’nt escape me as did the one about O’neal starting out in the junk-bond division of Merill…..in 1986 no less.

Stupid is stupid does.

Ciao

MS

VJ:

Wasn’t it CFC that said they see blue skies and profitiability in 4Q and on down the road? It seems his statements at the Milliken Institute are at odds with that.

Eh gads, Tampa prices are falling by more than Detroit!!! Now that’s news. Florida is toast.

The HGX has just gone positive… must be time to back up the truck on homebuilders.

Florida is right: rate cuts no way!

I’d go further by suggesting a 25 points rate HIKE. Just a one time trick but you don’t say so. Just to signal to the market participants that moral hazard won’t be tolerated anymore.

However, this scenario assume a Fed with cojones and spine, able to clearly tell to their political counterparts that they work for the good of the country, not for the elephant or the donkey, and if they ain’t happy with that, they have the right to go to Hell. Volker did it: why can’t Copter Ben try to emulate a real man, instead of Easy Al, the Great Invertebrate?

I’m definitely not holding my breath for that to happen, but one can always dream a bit no? :-D

Francois

i don’t get why falling housing prices effects anything. I mean, really, how often do people actually move? The only time your housing price matters is when you’re selling.

A house isn’t an investment, it’s a place to sleep.

And rates should go up. Our problem right now is billions of bad loans. I fail to see how lower interest rates is going to help stop bad loans.

don’t expect rate hike from dovish JumboJet Fed Ben. He is stock market pumper. He cuts rate to pump up market. Just look at repo, you know he will cut by 50bp again. don’t place your bet according to wish.

So now we have former Treasury Secretary Rubin back in the picture as Bloomberg headlines read… “Rubin urges policy makers to re-establish fiscal discipline… says policy favoring weak dollar isn’t ‘sound approach’… much weaker dollar could boost inflation… lower exchange rate reduces U.S. living standards… goal should be ‘strong currency based on sound policy’… ”

O-kay… is this part of the ‘Rubin Rule’

“One of their guests was demanding 11 consecutive 25 bps cuts.” and gutless Ben will cave in like last time. well I mean dovish and deflation fighter will excel his predecessor. Ben preemptively cut 50bp before the problem appear. he will do at least another 50bp cut. we should be prepared for consecutive cuts in the future, because Ben really want to make sure stock market continue to moon

And right on cue. GE “lays off” all of it’s mortgage personnel…….ONE FULL DAY BEFORE the FED decision. I’m guessing Mr. Immelt was not part and privy to the many meetings that have taken place……secretively of course…

Ciao

MS

“i don’t get why falling housing prices effects anything. I mean, really, how often do people actually move? The only time your housing price matters is when you’re selling.”

The reason falling home prices affects the economy is threefold:

1. Consumers, for the last 5-10 years, have been using the artificially created housing bubble to convert their homes into ATM’s, and much of the equity they withdrew via MEWs went directly back into the economy. Many people were also making a lot of money flipping homes, which was another large source of consumer spending that is now kaput. To put it plainly: The spending party is over, and it’s abrupt end will put a rather large dent in overall consumer spending (unless the FED floods the economy with money…).

2. The housing industry comprises 5% of the overall economy. When home prices are falling and inventory piles up, builders cannot sell homes because no one wants to buy into an obviously losing deal. If builders are not selling homes, they are also not building them, which leads to job cuts across the board in the housing industry. Current GDP growth is around 2% – So if 40% of the (massively inflated) housing industry vanishes, that’s 2% less growth… Or, in other words, economic stagnation. Any more than 40%, and the US sees negative growth. Of course, that’s overly simplistic, but it’s also essentially correct.

3. It’s not only falling home prices that are the problem – It’s the ARM loans. Every dollar that consumers must pay to keep their homes when their ARMs reset is one dollar of less disposable income they spend. Even if not one single person lost their homes, those ARM resets have the potential to put a very large dent in overall consumer spending. (Unless the FED continues inflating, of course…)

That’s why.

“i don’t get why falling housing prices effects anything. I mean, really, how often do people actually move? The only time your housing price matters is when you’re selling.”

Robert, you forgot about the most important element in your lesson — “the wealth effect.” American consumers have (and will continue) to spend as long as they continue to “feel wealthy” and they have any credit capacity whatsoever (spending is largely behavioral — and less something that can be forecast with quantitative measurement). Furthermore, the wealth effect is more powerful with homes (as compared to stocks) because the “average joe” thinks home prices never fall. Additionally, the wealth effect is not limited to only those with poor financial habits. It affects everyone to some degree.

Perception is reality. If (and when) consumers cease to “feel wealthy,” reality will hit home (pun intended) and the party will truly be over…

Joe,

“Wasn’t it CFC that said they see blue skies and profitiability in 4Q and on down the road? It seems his statements at the Milliken Institute are at odds with that.”

Yepper. Of course, back then Tangelo was trying to make nice with BOA.

I’m with schumacher. He’s once again making a lot of noise right before the Fed meeting. Also noticed that Crazy Cramer was on NBC Nightly News again tonight, predicting DOOM if the Fed doesn’t cut (no foaming at the mouth this time).

.

forgive my ignorance, but discussions about rate cuts and what they mean to mortgage rates always seem to be accompanied with a caveat, “however short term rates don’t always influence long term rates”.

at the same time, most bond market players will openly acknowledge that china’s anti-free-market currency pegging strategy is what has affected our long term rates for the last decade.

why then does the media (read: wsj oped pages) consistently blame al and ben for the housing bubble?

we are facing this uncertain situation because we have a government, not a market, influencing the prices on everything for the last decade.

to this end, i believe (likely naively optimistically idealist) that Mr. Paulson and the current weak dollar strategy are designed to shake the dog off our ankle and get the markets setting prices again.

A Deepening and Wealth-Eroding Housing Downturn Seems Likely

The case for a protracted housing downturn (until 2010 at the earliest) and a broad and associated negative wealth effect remains likely.

* Home affordability remains stretched. Home prices in real terms are only about 3.5% lower than at the peak last year. According to Dr. Lacy Hunt, “Real home prices remain nearly 58% above the previous cyclical high reached in 1989 and almost 94% above the average real price from 1890 through 2007.”

* Housing starts would have to drop by another 25% just to reach the average cyclical lows over the last 50 years.

* We are now at a record level of months of unsold home inventory. With cancellations as high as 50% to 65% at certain public homebuilders, resets accelerating into next year (causing more defaults/foreclosures and supply to come on to the markets) and with lower selling prices and concessions failing to stimulate demand recently, months of unsold inventory will likely expand in the months ahead.

* Not only has the issue of home affordability yet to be resolved but home ownership is still high relative to rentals. According to Dr. Shiller, home prices would have to fall by over 50% to be aligned with rental values.