Defeated managers, in assets globally (Statistical Ideas)

One would think that active managers would eventually outperform somewhere after the negative press that ensued a year ago. And now that 2015 performance data has been properly audited and tabulated, we can see what the new results are. We normally don’t delve into the same topic twice, but as with some matters there is ample public curiosity to see what might have changed. This is one of those times where is it is critical to revisit our numerous warnings about the skill of active managers in outperforming their benchmarks, particularly now. Over the past year, through today, a number of interesting folks (too many to list here but will do so on social media) at the tip-top of the investment community and in journalism have taken a key interest in the Indomitable benchmarks article. In it we showed that in all 17 mutually-exclusive risky segments of the U.S. markets, active managers underperformed their benchmarks. The gap was so wild that it was probabilistically a once in a multi-thousand year event due to chance alone. In other words, they were specifically bad for your money, can’t blame it on luck, and the government has listened. And the article was one of the most popular ever for this site. Today we take a unique look at the 2015 data recently released by S&P Indices. We scan not just U.S. fund managers, but also examine fund managers in all available countries globally (for stocks, bonds, and real estate). The results will only surprise those who are just now heeding attention.

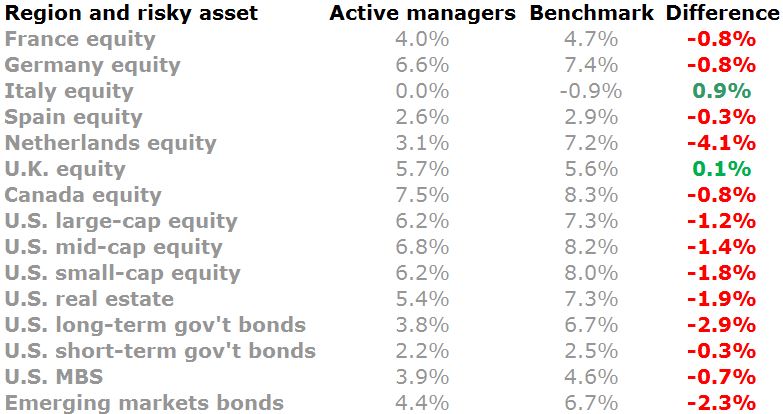

Now for housekeeping we should note that only regions with 10-years of performance data were included, to capture pre-TARP/ZIRP, a full economic cycle, and to not muddle with statistics over the short-run that more arguably are the result of luck. Canada was the only exception to the rule, with only 5-years of found data, but their performance was so similar to the U.S. that it was worth showing with this disclaimer. What we notice from this exercise above is that active managers have underperformed (for reasons noted in these most-read articles from Pensions&Investments or from CFA) over a long-run not just in U.S. equities, but also across different assets around the world. This includes once-successful investment vehicles such as Berkshire Hathaway, and Sequoia Fund.

Sure there were 2 winners in the 15 mutually-exclusive funds above (or only 2 winners out of 18 if we look at value versus growth in the U.S. as described above), while last year’s rolling 10-year returns showed 0 winners out of 17 funds. That was the point of this exercise to see what range in underperformance exists across a variety of instruments and cultures (some argue that overseas fund managers may be more quantitative, or disciplined, or dabble in more inefficient markets, etc.) There is little good of course to report, though not everything appears immensely cruel. We should note that theaverage underperformance on these 12 funds above is 1.2% (with a standard deviation of 1.2% as well), and the 1-year U.S. equity returns for just 2015 was -1.5% (versus a benchmark of +1.0%). So it is clear that the active fund manager results, in developed-market assets around the globe, have continued to underperform by a reasonable amount. And for U.S. equities, the dire contrast on how severely fund managers were underperforming showed through with yet another year where nearly all fund categories underperformed their benchmarks. Enough of an underperformance across most risk segments that it substantiates last year’s results in Indomitable benchmarks were not the result of luck.